2 Energy Stocks I'd Buy Right Now

I find it fascinating that when you type the phrase "eat your own cooking" into a basic Google search, the top results are all related to wealth management and investment advice. Apparently, investors are looking for advice from people that are doing that very thing and putting their money where their mouth is.

So in the spirit of sharing my home cooking, I thought I would discuss two stocks I would buy right now. It's much easier to do that since these two stocks are both ones I previously owned and have gone back to the well for more. The two stocks that look compelling to me today are First Solar (NASDAQ: FSLR), and Enterprise Products Partners (NYSE: EPD). Here's why these two are the stocks I'm adding to my positions now.

Image source: Getty Images.

A speed bump on a long runway

Of all the sources of energy available today, alternatives such as wind and solar have the most room available to grow. For starters, alternative energy has such a small piece of a massive pie. Today, total power generation from solar is less than 1% of the total energy mix. Much of the development over the years has been helped along by government tax credits and other incentives for non-carbon or domestic power generation, but the industry truly is at a tipping point.

According to the most recent version of Lazard'sLevelized Cost of Energy (LCOE) survey, the average cost of a utility-scale solar facility per megawatt hour is the second least expensive option today, trailing only wind turbines. What's more important is that those comparisons are an unsubsidized level, which means before any subsidies. While it isn't a perfect comparison, it does highlight the progress solar has made in recent years to be competitivewith conventional power generating assets. As power producers such as utilities look to add capacity or need to replace old power generating assets, solar is likely going to take a larger piece of the pie.

The reason First Solar and so many other solar panel producers are cheap today is because, well, solar is still a cyclical industry. Even in fast-growing sectors, too much panel manufacturing capacity coming online at one time or a slight dip in growth rates can cause panel prices -- and profitability -- to suffer. Today, the industry is feeling the hangover effects of some government policies that encouraged investors to complete projects by the end of 2016 to reap certain tax credits. Those benefits were extended, although too late for many developers to change their project timelines. A slight slump in demand today, though, is providing a splendid time to buy shares of First Solar.

First Solar stands out among the rest of solar panel producers for one simple reason: It's better at allocating capital. In a business where margins are rather thin, technology develops at a rapid pace, and demand can wax and wane; where and when you invest your money matters. First Solar is an example of a company that does this better than any other in the business. Over the past decade, it has been able to generate the best returns on equity in the industry consistently and has the balance sheet strength to ride out these short-term downturns better than almost any other.

There is a lot of short-term pessimism baked into First Solar's stock -- it trades at a price to tangible book ratio of 0.5x. What's even more incredible about First Solar's stock price is that its cash on hand is equal to 70% of the company's market capitalization. Wall Street is pricing in an immense amount of pessimism for an industry leader with a bright future ahead of it.

A sound base for an energy portfolio

One thing that can make First Solar investors skittish is the fact that its stock is so volatile. Having to stomach the wild ups and downs of the solar industry isn't easy, but it is made much easier with Enterprise Products Partners as part of my portfolio. The company's massive infrastructure network, its investment grade credit rating, and conservative management team make it a stock you can buy and hold for years without giving much thought to it.

The transportation and infrastructure business is considered the stalwart of stability in the oil and gas industry. Many of these companies structure their contracts with producers and consumers such that they pay a fixed fee to move or process a mandatory minimum amount of volume. There are, however, some minor nuances in this business that make some operators a more reliable investment than others. For example, pipelines designed to gather and consolidate production from disparate wells tend to be more susceptible to the ups and downs of the market since they rely on production from a few individual wells or a particular production region. By contrast, long-haul pipelines that transport from hub-to-hub pull production from a multitude of locations and tend to remain in service no matter the commodity price environment.

Enterprise's asset profile is unique in the sense that it is mostly an integrated system. If the company does have gathering pipelines in a particular region, then those assets are also connected to long-haul pipelines and in many cases connected to processing facilities. Enterprise's network of oil, natural gas, and natural gas liquids pipelines connects to every major U.S. shale basin, every ethylene processing facility, and 90% of the oil refining capacity East of the Rocky Mountains. This high level of connectivity makes Enterprise's network attractive for its customers and provides it with unique investment opportunities that few other companies in this industry have.

With shale drilling starting to recover in the U.S., a booming business is emerging in the U.S. Golf Coast to manufacture and export petrochemicals from cheap feedstocks such as natural gas liquids. In less than a decade, The U.S. has transformed from a net importer to the world's largest exporter of propane gas, and Enterprise exports more than half that product. This is just one example of how Enterprise's diverse portfolio has allowed its management team to invest in unique projects that few competitors can replicate.

What is also impressive about Enterprise is how they source capital to invest. Unlike so many others that rely exclusively on external capital from equity issuance or debt raises, Enterprise retains a large chunk of internally generated cash flow. When you say that out loud, it sounds like business management 101, yet it is frightening how many companies in this business elect to pay every available dollar in cash to its shareholders rather than keep some to fuel growth. In 2016, Enterprise was able to reinvest $700 million in retained cash flow to support its growth program. That is $700 million less in interest bearing debt chewing up cash or additional shares that will slow per share payout growth over time.

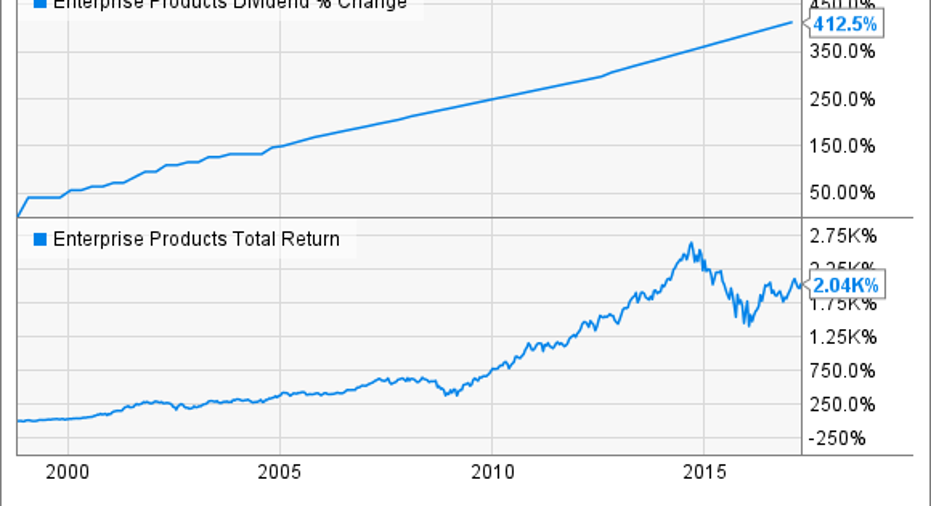

Most investors will pick other pipeline companies because their payouts are projected to grow faster, or their current payout yields are higher.Shares of Enterprise carry a distribution yield of 5.9% and management has increased that payout at a 5.1% annual rate. Neither number by itself is that eye-popping, but add to it Enterprise's streak of increasing its payout every year since its IPO in 1998 and you get some pretty impressive growth over the long haul.

EPD Dividend data by YCharts.

Enterprise's stock currently trades at an enterprise value to EBITDA ratio of 16.2 times. That valuation is more or less in line with its historical average valuation. So you could say that Enterprise's stock is neither cheap nor expensive today. For such a stable business that pays a reliable, modestly growing, and high-ish yielding dividend, that seems like a price worth paying.

10 stocks we like better than Enterprise Products PartnersWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Enterprise Products Partners wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of April 3, 2017

Tyler Crowe owns shares of Enterprise Products Partners and First Solar. The Motley Fool recommends Enterprise Products Partners. The Motley Fool has a disclosure policy.