Better Buy: Starbucks Corporation vs. Dunkin Donuts

For years, Starbucks (NASDAQ: SBUX) and Dunkin' Brands (NASDAQ: DNKN) largely went after different demographics.

Dunkin' had a blue collar reputation selling simple coffee along with doughnuts, bagels, and breakfast sandwiches. The company, for many years, played to its working class New England roots, and in some ways it still does.

Starbucks has always been a bit more for the coffee snob. The company brought European style coffee houses, complete with espresso drinks to the United States. It has changed how Americans drink coffee, but it has also led the way with flavored drinks, frozen beverages, and other choices for consumers who don't want a plain cup of java.

Both chains have been very strong despite an overall difficult market for restaurants and both continue to grow. Starbucks and Dunkin' Brands have been good to shareholders over the long term, and prospects for both look strong.

Starbucks' Roastery in Seattle has become a destination for coffee lovers. Image source: Starbucks.

Both have similar strengths

Recently, the two companies have gotten more similar. Dunkin' has moved its offering more toward its rival's space by adding espresso-based drinks. In addition, the two companies offer a variety of seasonal products designed to drive traffic, lure new customers, and get existing users to spend more.

Both chains are now digital leaders offering mobile ordering and payment through their apps. Starbucks was the pioneer in that area, but Dunkin' Brands has largely caught up.

As noted above, both companies had strong results in 2016, but Starbucks' were a little stronger. Dunkin' Brands reported comparable-store sales growth for the year of 1.6% at its coffee chain while Baskin-Robbins had 0.7% growth. The company added 723 new restaurants globally and delivered a 1.1% increase in revenue. Diluted adjusted earnings per share rose 15.5% to $2.23 on a 52-week basis.

For the full year, Starbucks saw global same-store sales rise 5%. It also grew revenue 11% while increasing its EPS 4% to $1.90 a share, though that should be adjusted down $0.06 as the company had an extra week in its fiscal year compared to 2015. The chain opened over 2,000 stores in 2016.

Both companies, it's worth noting, pay a dividend. Starbucks' has been $0.25 per share for the past two quarters, while Dunkin' Brands raised its dividend for Q1 2017 7.5% over the previous quarter to $0.3225.

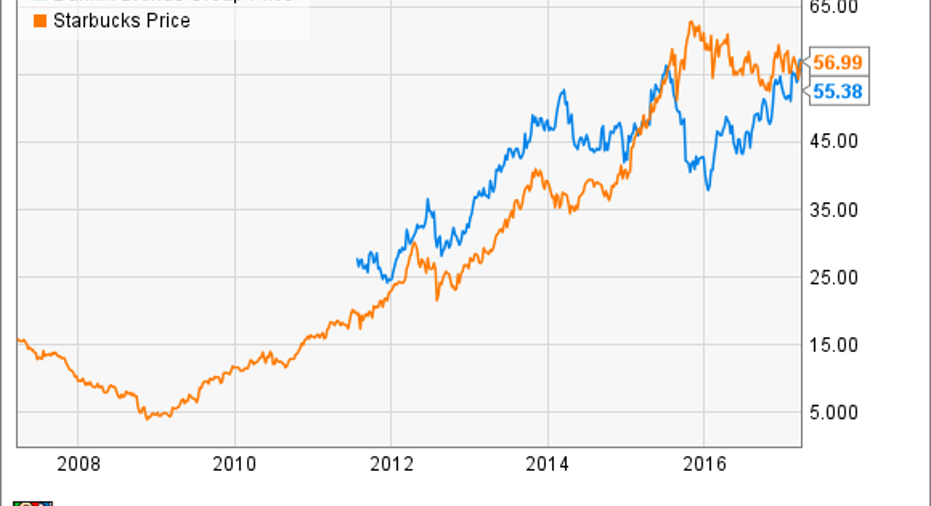

Image source: YCharts.com.

What's next for both brands?

Both Dunkin' and Starbucks have major expansion plans. Deciding which company is a better buy largely rests on which chain's long-term vision you believe in more.

Dunkin' has been slowly growing its footprint in the U.S. outside its Northeast home. That has included major growth on the West Coast, and in Texas, as well as in markets around the world. For its expansion the company has been sticking with its proven model. There are regional and international tweaks, but the core format is coffee, pastries, breakfast items, and a limited effort at selling lunch.

Starbucks has a much bolder plan for expansion that not only includes adding stores, but also launching a premium brand. The company has even put outgoing CEO Howard Schultz in charge of its efforts to build out its Roastery Business and Reserve brands.

The company plans to build new Roastery locations in New York, Shanghai, Tokyo, and Milan this year and next. On top of that the chain plans to open over 1,000 Reserve stores and add Reserve bars to up to 20% of its locations by 2021.

It's a bold plan that may hit bumps in the road, but Schultz has pointed out many times that the average check at the Seattle Roastery comes in at four times what a typical customer spends in a regular store. The question for investors is how much the company can scale the concept. A destination visit to a Roastery is a unique event where money may not be an object, but will consumers regularly spend more at a Reserve store or bar?

Which stock is a better buy?

Dunkin' Brands has taken a slow and steady approach to expansion while Starbucks is making a big expensive bet. In the short term that could mean some down quarters, but in the long run it gives the coffee retailer a higher ceiling.

By only building a few Roastery locations Starbucks should keep that brand as a destination -- a kind of theme park for coffee where consumers don't think much about cost. Growing the Reserve brand will be a bigger challenge, but the chain has shown that people will pay more for premium experiences. There may be a limit on what customers are willing to pay for that, but offering higher-end coffee, food, and experiences should deliver an increase in sales from the new stores while raising comps in existing locations that get Reserve bars. It's also possible that offering a coffee experience meant to be savored will drive afternoon and evening sales, something both companies have struggled with.

With these two companies there are no losers. Starbucks just has a higher ceiling if you believe -- as I do -- that it will make premium coffee work on a broad level. Dunkin' still has a lot of room to grow its store footprint and it should be able to do that successfully. Over the next few years, however, Starbucks is a better buy because it should be able to dramatically raise its margins by selling pricier coffee in its Roastery and Reserve locations.

10 stocks we like better than StarbucksWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Starbucks wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017

Daniel Kline has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Starbucks. The Motley Fool recommends Dunkin' Brands Group. The Motley Fool has a disclosure policy.