5 Reasons to Buy HCP, Inc. Now

Healthcare real estate investment trust HCP, Inc. (NYSE: HCP) has come a long way over the past year or so, and continues to improve with every quarterly report. Between the company's improving fundamentals and attractive valuation, the nature of the healthcare real estate business, and the future demand for healthcare in the United States, there are some good reasons to consider HCP for your portfolio.

1. Better private-pay revenue mix than most peers

When it comes to the revenue generated by healthcare properties, private-pay revenue sources are generally more stable and predictable, as opposed to revenue dependent on government reimbursements. This is especially true now, as there is tremendous uncertainty surrounding healthcare reform in the U.S., and Medicare isn't exactly on the most stable financial footing.

Image source: Getty Images.

Ninety-four percent of the revenue generated by HCP's healthcare properties comes from private-pay sources, one of the highest ratios in the industry.

2. Attractive valuation

Another reason to consider HCP is that it's an attractively valued stock. Healthcare REITs in general trade more cheaply than other types right now, and HCP is cheaper than most. Here's how HCP's valuation compares with industry leader Welltower (NYSE: HCN), as well as a couple of leading REITs with other property specializations.

|

Company |

Recent Stock Price |

2017 FFO Guidance |

P/FFO |

|---|---|---|---|

|

HCP |

$30.62 |

$1.89-$1.95 |

15.9 |

|

Welltower |

$69.78 |

$4.15-$4.25 |

16.6 |

|

Realty Income (NYSE: O) (Retail) |

$59.51 |

$3.00-$3.06 |

19.6 |

|

Equity Residential(NYSE: EQR) (Apartments) |

$63.34 |

$3.05-$3.15 |

20.4 |

FFO Guidance is normalized, when available, and P/FFO is based on the midpoint of each company's guidance range.

3. Buy before balance sheet/credit improvements

One factor that could explain HCP's lower valuation is its balance sheet. In a nutshell, HCP's balance sheet and credit ratings are not quite as good as those of many peers, such as Welltower.

However, since spinning off its riskier assets into QCP in October 2016 and agreeing to strategically sell some of its other properties, HCP's financial condition has improved a great deal. HCP sees this improvement continuing for the next few years, and hopes to regain its Baa1/BBB+ credit ratings (Baa2/BBB currently). If these goals are met as planned, HCP's valuation could rise considerably.

|

Metric |

End of 2016 |

2017 Goal |

2019 Target |

|---|---|---|---|

|

Net debt/EBITDA |

6.2x |

Low- to mid-6x |

5.5x-6.0x |

|

Leverage |

48.6% |

43%-44% |

Less than 40% |

|

Fixed charge coverage |

3.6x |

3.6x-3.8x |

Less than 3.5x |

Data source: HCP investor presentation.

4. A fragmented healthcare real estate market

The current U.S. healthcare real estate market is about $1.1 trillion in size, and is highly fragmented. In fact, no REIT has more than a 3% market share, and it's estimated that just 12%-15% of all healthcare properties are REIT-owned, as compared with 40% or more for other property types, such as malls and hotels.

Image source: HCP investor presentation.

Larger operators have advantages when consolidation occurs, such as the cost advantages that come with a larger operation, and the financial flexibility to pursue attractive opportunities as they arise. In fact, HCP estimates that it has an "investable universe" of about $650 billion in properties between its three main property types -- senior housing, medical office, and life science.

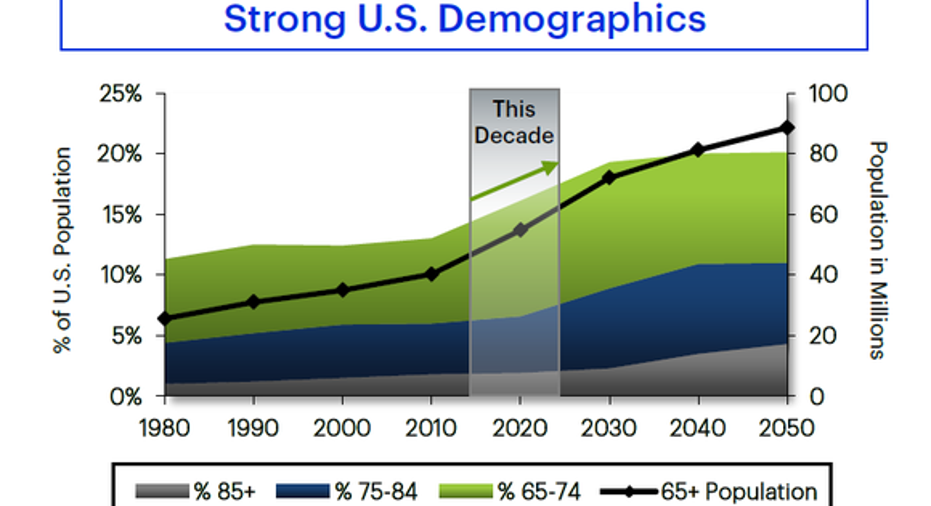

5. Ground-up developments could drive performance

In addition to the existing market, there's reason to believe that there are good times ahead for healthcare real estate, particularly senior housing and medical offices. In a nutshell, the U.S. population is aging -- fast. Older people tend to utilize healthcare services more and also spend more (either by themselves or through insurance) when they do.

Image source: HCP investor presentation.

So, another big growth opportunity is development of new properties, which can create instant value for shareholders.

To illustrate why this is so important, consider this simplified example. Let's say that apartment buildings bring in 7% of their value in rental income each year, so a $1 million property would bring in $70,000. Well, if you can build the same property at a cost of, say, $800,000, not only is the building instantly worth $200,000 more than you paid for it upon completion but the income generated now represents a greater percentage (8.8%) of the price you paid to build it.

HCP currently has $820 million in committed ground-up developments, mainly in life science properties, but sees a much larger pipeline going forward.

10 stocks we like better than HCPWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and HCP wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017

Matthew Frankel owns shares of HCP, Quality Care Properties, Inc., Realty Income, and Welltower. The Motley Fool recommends Welltower. The Motley Fool has a disclosure policy.