General Electric Company Still Has a Capital Arm; Here's Why It Matters

It's well known thatGeneral Electric Company (NYSE: GE) is shifting back to its industrial roots with CEO Jeff Immelt planning to generate 90% of the company's earnings from its digital industrial businesses by 2018. As such, GE Capital assets have been sold off to banks like Wells Fargo & Co and Capital One Financial Corp., while the highly successful Synchrony Financial (NYSE: SYF) spinoff also saw General Electric jettisoning financial businesses. With all of this going on, it's easy to forget that the company still has a capital arm, and it happens to be a key part of its future. Here's how and why.

GE Capital industrial finance solutions are being expanded to also cover renewable energy. Image source: GE Reports.

General Electric becomes an industrial again

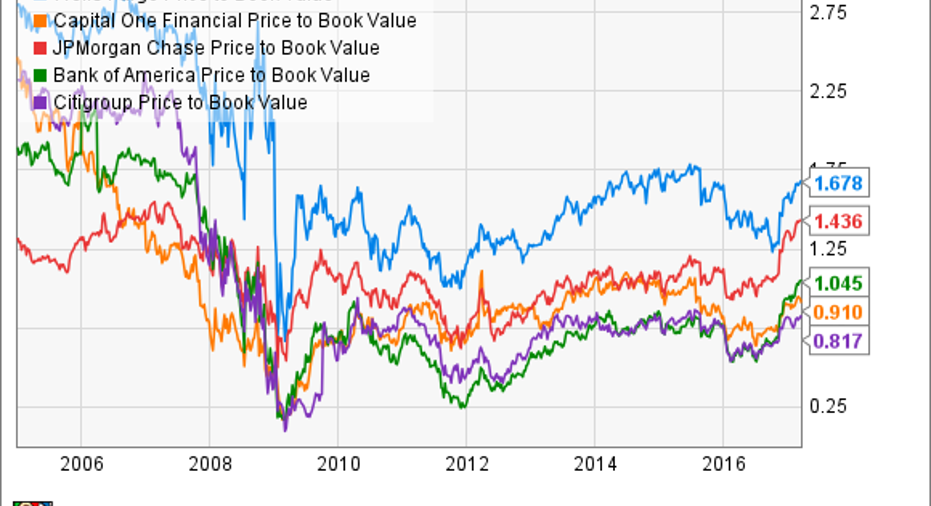

The financial crisis hit GE particularly hard, and few long-term investors will forget when Immelt cut the dividend to 10 cents a share from 31 cents a share in 2009 -- the first cut since 1938. The effects of the crisis still linger, and as shown below, bank stock valuations are nowhere near what they used to be prior to the crisis.

WFC Price to Book Value data by YCharts.

However, industrial company valuations are comparable to pre-recession levels.

HON EV to EBITDA (TTM) data by YCharts.

In other words, the market has decided to take a different view on future prospects of the two industries -- not least because banks like Wells Fargo are more subject to regulation intended to reduce risk, andthis is likely to make them less able to generate outsizedreturns.

GE Capital still has a role

With that said, many industrial companies have financial arms that support their businesses, and GE is no different. In a presentation given at a recent JPMorgan conference, GE Capital CEO Richard Laxer claimed that 90% of GE's financial services business is now aligned with GE's industrial business, whereas "a few years ago it was 50-50." Here are the benefits of such a change:

- GE Capital can help drive industrial order growth through offering financing: Laxer claimed 23% of equipment orders in 2016 were facilitated by GE Capital.

- Through its participation in the so-called GE Store (the process by which different GE businesses collaborate in order to create value), it can provide financial and intellectual capital to GE and customers.

- It allows GE to receive access to capital markets, ultimately in order to better facilitate customer order growth.

- GE Capital generates earnings on its own.

To demonstrate how this works, Laxer outlined the three areas where GE Capital is active today. In aviation finance, it's the world's leading aircraft-leasing company, with 85% of its fleet powered by GE or GE joint-venture (CFM) engines. Second, in energy finance, 90% of its investment activity is related to GE equipment. Third, industrial finance reduces friction at the point of saleand generates cash flow for GE.

Aviation and energy are core industries for GE, and they both tend to involve significant investments by customers who are unlikely to recoup their investments in terms of cash flow in the near term. In this context, GE Capital's services are key to driving order growth. Meanwhile, industrial financing is being expanded from traditional strength in healthcare toward areas like transportation, additives, oil and gas, and renewables.

Looking forward

This industrial pivot isn't just about GE's industrial businesses. It also marks a change of emphasis at GE Capital. In a nutshell, the capital arm is now overwhelmingly focused on helpingGE's industrial businesses generate growth and productivity.

Moreover, as the company expands into emerging markets, it's going to be increasingly important to create financing solutions for potential customers in areas like energy and transportation. All told, GE Capital is still an integral part of GE's future and another good example of how the company is leveraging scale to give itself an edge over the competition.

10 stocks we like better than General ElectricWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and General Electric wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017

Lee Samaha has no position in any stocks mentioned. The Motley Fool owns shares of General Electric. The Motley Fool recommends Synchrony Financial. The Motley Fool has a disclosure policy.