Your Gut Feeling is Right: 8Point3 Energy Partners is a Buy

It might seem almost too good to be true, but there really is a stock that simply owns a large number of solar panel installations and pays out the cash flow generated from said assets to shareholders. Sure, we've all been there before: we've all heard about an investment that promises a bright future and predictable returns. However, at least with 8point3 Energy Partners (NASDAQ: CAFD), the dream may very well align with reality. Here's why.

Recent History

First, the bad news: the current investment environment for solar energy is less than ideal. Wall Street, recently burned by SunEdison's bankruptcy, is less than enthusiastic about contributing more capital to the sector. Worse, SunEdison's trip to Chapter 11 court brought with it its own two yieldcos, TerraForm Power(NASDAQ: TERP) and TerraForm Global(NASDAQ: GLBL). These two yieldcos are guilty by association, and while the jury is still out on their situation, these two entities -- which were once thought to be completely safe -- have left many investors high and dry.

Source: Getty Images.

Which leads us to 8Point3 Energy, a yieldco created by not one well-run solar power firm but two: SunPower(NASDAQ: SPWR) and First Solar (NASDAQ: FSLR). The yieldco currently sports a sky-high dividend yield of 7.4%, which is great for enterprising investors but not so great for fulfilling on the company's basic mission -- to issue new equity and purchase new cash-generating solar projects from its two parent companies. The cost of capital associated with such a sky-high dividend yield is extremely prohibitive. The higher the dividend yield for CAFD, the higher the return on invested capital hurdle for assets that it might acquire.

Fortunately, these problems may very well prove transitory. True, 8Point3 ratcheted back its growth expectations (modestly) in its fourth quarter earnings release, but results have been decent and future growth plans remain more or less intact.Revenue came in at $14.5 million, netting the company just over $4 million in GAAP net income, derived from $18.3 million in EBITDA. Cash available for distribution came in at $20.4 million. Perhaps most importantly, the release included an announcement that 8point3 Energy Partners only plans to grow its dividend by 12% YoY in 2017. That's below the 15% dividend growth rate since the company was launched, and is at the low end of its own guidance.

All in all, investors probably are right to be somewhat leery of the solar sector at large. However, the company's recent results seem to be those of an enterprise that's built to last, especially when held up to the light of its history since inception.

A shining history

8Point3 was formed by First Solarand SunPowerto buy completed solar projects. The reason is that builders of large-scale solar projects have two options after a project is completed -- keep it on their balance sheet and derive decent returns on the invested capital for 10-20 years, or sell the project and use the cash to repeat the process. By creating 8Point3, both FSLR and SPWR gave themselves operational flexibility. Further, investors gained another investment option in the solar space -- one that wasn't subject to the ebbs and flows of actually building huge solar projects.

A bright future

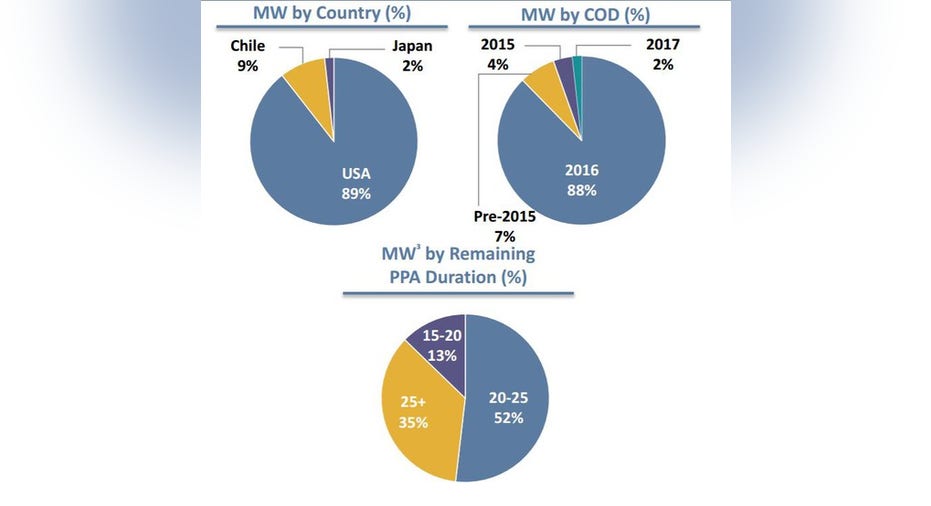

As seen in the company's fourth quarter results, current operations are going well at 8Point3. Its dividend is secure -- indeed, it was increased year over year, though not by as much as investors had hoped. Looking further out, the future does appear sunny. Not only does the company have a huge pipeline of projects with which to expand its portfolio, the equivalent of some 2.6 times its current electricity production, but it is about begin its expansion into international markets:

Source: 8Point3 Energy Partners Investor Presentation.

Source: 8Point3 Energy PartnersInvestor Presentation.

Essentially, not only does 8Point3 sport a 7.4% dividend yield supported by power generation contracts with an average life of 22 years, but it has a pipeline of projects that all but guarantees a long runway of growth in the years ahead. Obviously an attractive situation for investors to strongly consider, but there are a few kinks in 8Point3's armor for enterprising investors to be aware of.

A few sun spots

Positives aside, investors should be aware of the fact that a small portion of 8Point3 Energy Partner's planned future growth is to be located overseas. This is not, in and of itself, an inherent negative. However, there is something to be said for the political stability and contractual firmness that goes along with projects based in the United States.

Also, while the risks seem remote given the dual sponsorship of not one but two relatively strong enterprises, the risk that the company will run into funding issues at some point does exist. The experiences of investors in now defunct SunEdison's two yieldcos (enterprises that have avoided bankruptcy court but are nevertheless tarnished-by-association), Terraform Power and TerraForm Global, should not be far from investors' minds. Capital markets could dry up, through no fault of the company's. Such an eventuality would severely hamper the company's growth projections in the years ahead.

Yieldco 8Point3's future growth requires a constant stream of new projects and expansionary capital to add kindling to the fire. Case in point: for the FY ended November 30, 2016, CAFD was $73 million. This was supported, of course, from cash flows from its power generation contracts. However, equally important in keeping things moving was the issuance, over the same time period, of $430 million in stock and a net $217 million in new debt. Should there be no fuel to add to the fire -- 8point3 will likely be unable to deliver on its mission to acquire more and more projects in the years ahead.

Fortunately, the situation here isn't entirely dire. The company issued $102.6 million worth of shares at $14.65 last October in order to buy an interest in a Californian solar project. This issuance price is just 16% above its currently sagging valuation. While certainly not ideal, it shows that the company is capable of delivering on its business model once the current storm passes. Also, while there are recent claims that the company is overleveraged, its hard to take claims seriously given the company's current balance sheet (sporting $1.34 billion in assets and $455 million in liabilities, for a debt-to-assets ratio of just 34% as of November 30, 2016) and the backing of both SunPower and First Solar.

At the very worst, and if 8point3 doesn't grow one iota from here on out, investors can likely count on something similar to its current dividend for the next 23 years. That's nothing to sneeze at. At a 6% discount rate, and only including the dividends over the next 20 years, annual dividends of $1.08 per share discounted to the present at, say, 6%, are worth $13.13 . And this assumes NO terminal value of the enterprise at the end of this time frame. Here's the per share value of 20 years worth of $1.08 per share dividends at a few other discount rates:

| Discount rate | DCF value per share |

| 5% | $14.54 |

| 6% | $13.13 |

| 7% | $12.52 |

| 8% | $11.68 |

Source: Author Calculations.

Bottom line: 8point3 is currently trading at a valuation that not only assigns little to no value to the enterprise 20 years from now, but one that also assumes zero growth in the years ahead. Is this reasonable? You be the judge.

Foolish final thoughts

After taking in all of the pros and cons in, 8Point3 seems to be a great way to play the growth in solar power generation in the years ahead while simultaneously collecting a healthy dividend. There appears to be enough differences between it and SunEdison's yieldco's as well. So, if your gut has been telling you that 8Point3 is a great addition to your portfolio, the evidence seems to suggest that it just might be right.

10 stocks we like better than First SolarWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and First Solar wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017

Sean O'Reilly has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.