Here's Why the Best Is Yet to Come For HCP

Healthcare real estate investment trust HCP, Inc. (NYSE: HCP) has undergone a big transformation over the past year or so, and the result of these efforts is a much more stable, high-quality, and financially flexible company. However, the work isn't done yet -- the best could still be yet to come for HCP's shareholders.

The "new" HCP

By far, the most significant event that took place within HCP during 2016 was the spin-off of the HCR ManorCare portfolio of assets into a newly created REIT, known as Quality Care Properties (NYSE: QCP), or simply as QCP for short.

In addition, HCP decided to sell a significant amount of other properties in order to reduce its exposure to Brookdale Senior Living as a tenant. Lack of tenant diversification is a big risk factor for several major healthcare REITs, and HCP reducing its Brookdale concentration from 34% to 27% is a positive step in the right direction.

Image source: Getty Images.

Because of these transactions, HCP now has a much higher asset quality, as the portfolio is primarily composed of predictable, private-pay healthcare properties. Private-pay is generally more stable than properties dependent on government reimbursement programs, and HCP's portfolio is now 94% private-pay, and is spread out among senior housing, medical office, and life science property types.

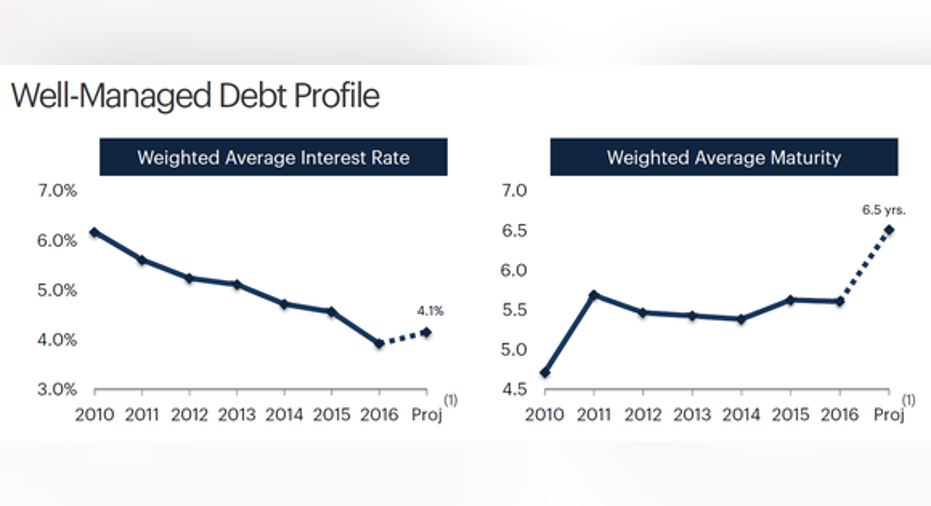

Also, the company is more financially sound than it was a year ago. Thanks to debt repayments that resulted from the spin-off proceeds, HCP has no significant debt maturities through the end of 2018. Plus, the company has done an excellent job of reducing the interest rates on its debt, while maintaining long-dated maturities and avoiding floating-rate debt.

Image source: HCP Investor Presentation.

HCP's 2019 goals

One of HCP's primary goals is to regain its Baa1/BBB+ credit ratings, which it lost some time ago.

To achieve this goal, HCP intends to dramatically improve its financial condition over the next few years, and reduce its tenant concentration even further.

|

Metric |

End of 2016 |

2017 Target |

2019 Target |

|---|---|---|---|

|

Net Debt/EBITDA |

6.2x |

Low- to mid-6x |

5.5x-6.0x |

|

Leverage |

48.6% |

43%-44% |

Less than 40% |

|

Fixed-Charge Coverage |

3.6x |

3.6x-3.8x |

More than 3.5x |

|

Top 3 Tenant Concentration |

44% |

35%-40% |

30%-35% |

Source: HCP Investor Presentation.

HCP also expects to increase its re-development pipeline in order to maximize returns. In the near term, HCP anticipates $75-$100 million of re-development projects per year, with a cash-on-cost return in the 9%-12% range -- significantly higher than the company can expect from simply buying an existing property.

HCP will be in a strong position to capitalize on the growing healthcare market

There are a few reasons to be bullish on healthcare real estate, both in the intermediate-term and over the next several decades.

For starters, the U.S. population is aging -- fast. Over the next 20 years, 10,000 people will turn 65 in the United States every day, and the 75-and-over population is expected to roughly double over the next 20 years. This translates to an expected surge in healthcare demand, especially for senior housing facilities, HCP's bread-and-butter.

Additionally, the healthcare real estate market is highly fragmented and is in the early stages of REIT consolidation. The existing inventory of healthcare properties in the U.S. is estimated to be worth about $1.1 trillion, and even the largest REITs have a market share of about 3%. In all, less than 15% of healthcare real estate is REIT-owned (compared with 40% or more for properties like hotels and malls), so there is ample opportunity for growth within the existing inventory.

Image source: HCP Investor Presentation.

Invest with the long term in mind

As a final point, healthcare real estate is an inherently defensive type of asset. It is a non-discretionary type of commercial business, which means it generally holds up just fine during recessions and other tough times. Plus, most healthcare tenants are on long-term net leases with 2%-3% annual rent increases build right in.

Having said that, this doesn't mean that HCP is immune to volatility along the way. There are several factors that could send shares on a roller-coaster ride, such as interest rate fluctuations and political uncertainty in the healthcare industry.

The point is that REITs like HCP should be approached as long-term investments. Over the long term, HCP's business model should generate excellent returns, but not without a few bumps in the road along the way, so invest accordingly.

10 stocks we like better than HCPWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and HCP wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017

Matthew Frankel owns shares of HCP and Quality Care Properties, Inc. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.