5 Things You Didn't Know About Costco Wholesale Corporation

Costco (NASDAQ: COST) opened its 100th warehouse in December 1992. A quarter-century later, the retailer generates $116 billion of annual business out of its 728 locations.

Here are a few things you might not know about the world's second-biggest retailer, by revenue.

Image source: Getty Images.

California matters

Costco is highly leveraged to the California market due to its high concentration of the retailer's biggest, most profitable warehouses. Almost one-third of its entire U.S. revenue came from that single state last year.

And since the U.S. business accounts for over 70% of its operations, California plays an unusually large role in its global footprint. "Any substantial slowing or sustained decline" in this market, the company warns in its 10-K, "could materially adversely affect our business and financial results."

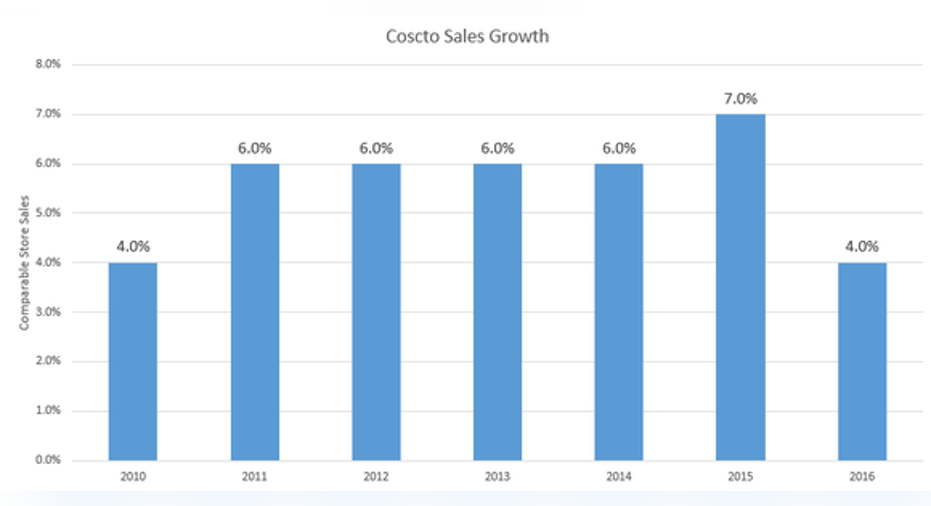

Customer traffic trends are down

Customer traffic gains have been the engine behind Costco's sales growth over the past decade. It handled a market-thumping 4% more member visits in each of the five years leading up to fiscal 2016, which helped produce comparable-store sales gains of 6% or better.

Annual sales gains. Chart by author.

That awesome streak ended last year, in part because its co-branded credit card switch produced a major disruption in membership renewals. Executives are hopeful that this will be just a temporary challenge, though, and renewal rates should climb back up above 90% over the coming quarters while bringing customer traffic levels higher as well.

Small selection

Rivals like Target (NYSE: TGT) and Wal-Mart (NYSE: WMT) aim to stock as wide a selection of products as possible, but Costco deliberately takes the opposite tack. These retailers carry over 80,000 items while a typical Costco warehouse holds less than 4,000.

By restricting selection to just the most popular, fastest-selling products, Costco can keep its expenses low through elevated sales volumes. In fact, the retailer moves through its inventory so quickly that in most cases it sells a product -- and receives payment for it -- before it has to pay its supplier. It can then use those savings to deliver prices that peers just can't match.

The membership business

Nearly all its earnings are generated by membership fees rather than the product markup that underpins most retailers' business models. That's why it's more useful to think of the company as a club engaged in subscription sales rather than a retailer interested in selling stuff.

The approach makes for significantly lower profitability. Costco's gross profit margin is roughly half Wal-Mart's 26% of sales and even further from Target's 30%. The same is true on the bottom line, where the company is lucky to turn 2% of sales into net income, compared to 4% for Target and 3% for Wal-Mart.

Yet Costco's earnings are much more stable since they're attached to recurring subscriber revenue and thus less exposed to swings in the economy.

Odd dividend approach

Especially considering its reliable profit stream, Costco delivers only a small portion of earnings to shareholders as dividends. Its payout ratio is about one-third of profits, compared to 50% for its retailing peers. One good reason for this skimpy capital return promise is that Costco is still aggressively expanding its store base and so there's less cash available to send right back to owners.

On the other hand, its paltry 1% dividend yield understates its actual payout. Twice in the last five years it has issued a massive special dividend to investors, amounting to $7 per share in 2012 and $5 per share in 2015.

By the end of this year, Costco will have opened 29 new locations to nearly match its most aggressive expansion pace on record. Executives see a wide retailing opportunity ahead, both in the U.S. and international markets.

10 stocks we like better than Costco WholesaleWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Costco Wholesale wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017

Demitrios Kalogeropoulos owns shares of Costco Wholesale. The Motley Fool owns shares of and recommends Costco Wholesale. The Motley Fool has a disclosure policy.