3 Energy Stocks We Can't Help but Love

Yeah, we know. Investing is supposed to be a profession that's devoid of emotion, but we're all human. Sometimes, there are those fantastic companies that you can't help but want to keep buying. When a company has proven to be an excellent operator and capital allocator, it's OK to get a little attached to its stock.

So we asked three of our contributors to highlight energy stocks they personally love, and why. Here's a quick rundown of the three stocks they chose: pipeline companies Enterprise Products Partners (NYSE: EPD) and Magellan Midstream Partners (NYSE: MMP)and refining and chemicals manufacturer Phillips 66 (NYSE: PSX).

Image source: Getty Images.

This long-term relationship continues to pay big dividends

Matt DiLallo (Enterprise Products Partners): I have owned units of midstream master limited partnership Enterprise Products Partners for nearly a decade now. My affection for the company certainly has grown over the years, helped by the fact that my initial investment has more than doubled. On top of that, the company has paid me a higher distribution in every single quarter since I first invested. My only regret is that I haven't invested more into the company over the past decade.

The reason Enterprise Products Partners has been such a strong performer is that it is one of the most conservatively managed MLPs in the sector. While most of its rivals were paying out nearly all their cash flow to satisfy yield-starved investors, Enterprise maintained its disciplined approach by retaining a significant portion of its distributable cash flow to reinvest in growth projects. Because of that, it has kept its unit count and debt from growing out of control. In fact, the company maintains one of the highest credit ratings among MLPs.

Enterprise has also maintained a disciplined approach to growth, only buying or building assets that deliver steady cash flow that will move the needle for distribution growth. Currently, the company has $5.3 billion of projects under construction and a growing pipeline of opportunities under development. As it completes these projects, they'll fuel incremental cash flow that it can use to keep the distribution growth streak alive. While it might not be growing as fast as some rivals, its slow-and-steady approach has proven to be a winning strategy in the past and should continue to be for the foreseeable future.

A pipeline with so many competitive advantages, it's regulated

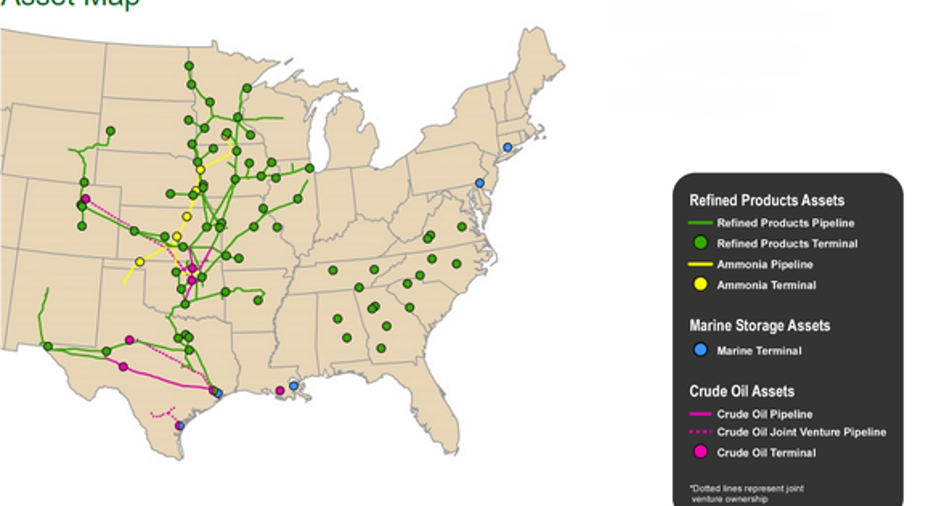

Tyler Crowe (Magellan Midstream Partners):I have been a shareholder of Magellan Midstream Partners for a few years now, and several of the reasons I like this company are the same ones Matt laid out for Enterprise: it has a conservative management team, retains cash flow for growth, keeps debt and equity issuance to a minimum, and has consistently increased its payout at a double-digit rate for more than a decade.

The one thing that makes Magellan a little different that many others in the midstream industry is that a decent portion of its refined petroleum product pipeline serves regions that are deemed non-competitive by the Federal Energy Regulatory Commission. Basically, this network is treated like a regulated utility because it delivers an essential product to underserved parts of the country.

Image source: Magellan Midstream Partners.

As part of its being a regulated pipeline, there are fixed-price guarantees that ensure a certain rate of return on these assets. For any investor looking for income, those are the sorts of traits that will ensure the company's payout to shareholders will continue for years into the future.

Magellan has recently completed a large round of capital spending, and so the pipeline for new projects is a little lighter than normal. However, the company has some new projects that are awaiting final investment decision that could significantly add to its capabilities as a major marine hub for crude oil and refined products in the U.S. Gulf Coast. Based on management's history of investing in projects with high rates of return and making timely acquisitions at the right price, this is the kind of company I want to own for a long time.

My favorite big oil stock for your retirement account

Jason Hall(Phillips 66): While my colleagues highlight two excellent energy investments, they come with the limitations of being MLPs, which could make them bad choices for retirement savers. This is because MLPs can be subject to taxes, even in your IRA, Roth, or 401(k).Phillips 66 is a wonderful company to consider if you're looking for a great energy stock to buy in your retirement account.

Like both Magellan Midstream and Enterprise Products, Phillips 66 is involved in what happens with oil and gasafterit is produced, thereby avoiding much of the commodity price risk that oil producers take on. But where the aforementioned partnerships focus on processing, transportation, and storage of oil, gas, and refined products, Phillips 66 is also one of the world's biggest refiners and petrochemical manufacturers.

This structure gives Phillips 66 a nice balance of steady cash flows from its refining business, but also strong growth prospects in its midstream and chemicals segments. Last year alone, the company invested nearly $3 billion in capital growth projects, and has billions more lined up, as demand for transportation, export, and processing infrastructure in the U.S. grows in coming years.

Furthermore, the company's management has proven to be very shareholder-focused. Since going public in 2012, the company has repurchased 17% of shares outstanding, and increased its dividend 215%. At 3%, there are bigger-yielding energy stocks out there, but if you're looking long term, Phillips 66's dividend growthcould deliver much bigger returns over time.

10 stocks we like better than Enterprise Products PartnersWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Enterprise Products Partners wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017

Jason Hall owns shares of Phillips 66. Matt DiLallo owns shares of Enterprise Products Partners and Phillips 66. Tyler Crowe owns shares of Enterprise Products Partners and Magellan Midstream Partners. The Motley Fool recommends Enterprise Products Partners and Magellan Midstream Partners. The Motley Fool has a disclosure policy.