Earnings Reports From 2 Companies Dragged Down All Frack Sand Stocks in February

What happened

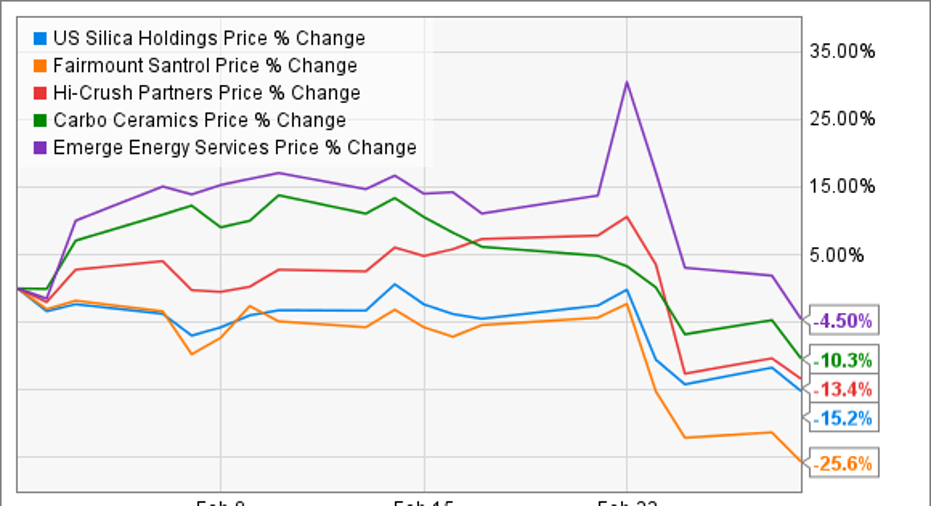

Despite signs that the market is improving for frack sand companies, the five large publicly traded players in this industry -- U.S. Silica Holdings (NYSE: SLCA), Fairmount Santrol Holdings (NYSE: FMSA), Hi-Crush Partners (NYSE: HCLP), Emerge Energy Services (NYSE: EMES), and CARBO Ceramics (NYSE: CRR) -- all saw their stocks drop big time after U.S. Silica and Hi-Crush Partners released earnings on Feb. 22.

Image source: Getty Images.

So what

It would seem that the market was expecting big things this quarter, especially after CARBO Ceramic's earnings report in January really impressed Wall Street, as it saw big bumps in sales volumes.

But apparently investors were looking for more than just increased sales from the rest of the frack sand group. When U.S. Silica and Hi-Crush Partners released earnings, they showed sand volume increases of 34% and 45%, respectively. Those figures were pretty much in line with the gains CARBO reported, but the opposite effect occurred: The whole group plummeted following those announcements.

What was even more peculiar about this was that shares of Fairmount declined more than the rest despite the fact that it has yet to report earnings (it will do so on March 9).

The biggest negative to come from U.S. Silica's and Hi-Crush's earnings reports is that those large increase in volumes sold didn't translate into better bottom-line results. Both companies still reported net income losses. This isn't that extraordinary, though, because both had higher-than-expected costs associated with ramping up production at some of its idle and underutilized facilities. These are larger one-time costs that we probably won't see in the coming quarters, but they were enough to paint the quarterly results in a bad light.

Emerge Energy Services also reported earnings later in the month, and its sales volume increase was even more impressive -- up 67% from the prior quarter! At the same time, though, weak sand prices and higher costs with ramping up production made profits elusive for Emerge in this past quarter as well.

Now what

It really seems as though Wall Street was a little too fixated on those short-term cost increases over the past quarter. After two years of declining sand volumes, this rapid uptick is going to require some higher expenses. Once those facilities get back up to higher utilization rates, though, they will be able to spread the fixed costs associated with those mines over a larger production rate and improve margins. It just may take a quarter or two for it to happen.

Shale oil and gas drilling is back on the rise and in a big way. All of these companies are touting volume sale increases above 30% (pending Fairmount's earnings report, of course), and there are signs that things are only going to get better from here. ExxonMobiljust announced that it was increasing its capital spending budget, and 25% of it -- about $5.5 billion -- is going to go specifically into shale drilling in the Permian and Bakken shale formations. That's a lot of wells, and that will require a lot of sand. If investors can overlook the short-term hurdles, there is clearly an opportunity in this industry.

10 stocks we like better than U.S. Silica HoldingsWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and U.S. Silica Holdings wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017

Tyler Crowe owns shares of XOM. The Motley Fool owns shares of XOM. The Motley Fool has a disclosure policy.