Bank of America's Shares Just Crossed an Important Threshold

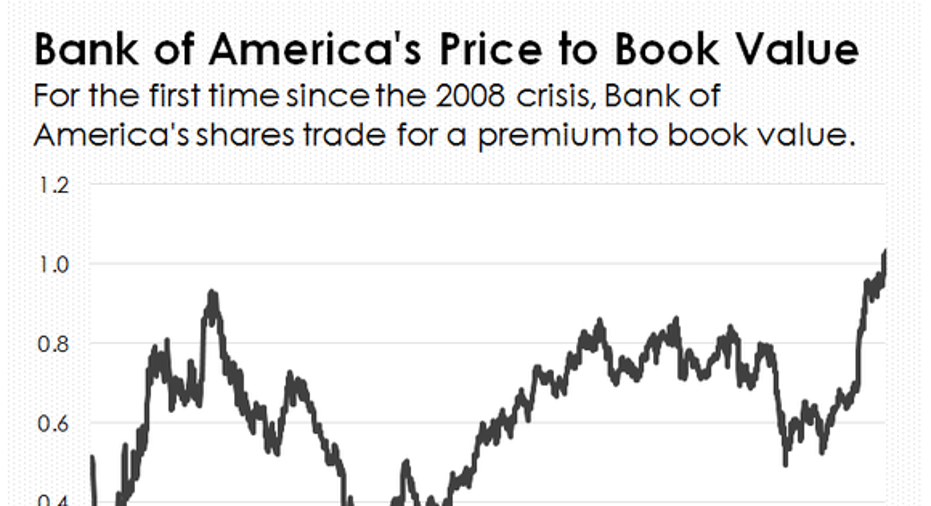

For the past eight years, Bank of America's (NYSE: BAC) stock has traded for a discount to the bank's book value per share, qualifying it as a bargain in many investors' minds. But that's no longer the case.

After climbing more than 45% since the presidential election, shares of Bank of America finally eclipsed the $24 mark earlier this month, which means its stock now trades for a 3% premium to book value.

Not to belabor the point, but this is the first time since the financial crisis that the nation's second biggest bank by assets hasn't traded for below its book value. That's an important threshold that current and prospective investors in the $2.2 trillion bank should take note of.

Data source: YCharts.com. Chart by author.

There's no question that Bank of America's stock could still go higher, as more profitable banks tend to trade for 30% or more over book value. However, it's equally important to recognize that there's a limit to how much higher shares of the North Carolina-based bank can go given the fundamentals.

This all boils down to the relationship between a bank's profitability, which is measured by return on equity, and the valuation of its stock. The higher a bank's return on equity, the higher its valuation.

As a general rule, a bank's shares will trade for a premium to book value only if the bank is creating value for shareholders in excess of similar investment alternatives. The demarcation point for banks is their cost of capital. So long as a bank's return on equity exceeds its cost of capital, in other words, its shares should trade for a premium to book value.

The issue with Bank of America is that it isn't earning its cost of capital -- which, according to my math, equates to an 11.7% return on equity. Bank of America had a very good 2016, but its return on tangible common equity was only 9.54%.

Bank of America's performance last year was better than 2015, when its return on tangible common equity came out to 9.08%. And it's much better than 2014, when the figure was a mere 2.52%.

Bank of America's stock just crossed a major hurdle, trading for the first time since the financial crisis at a premium to the bank's book value. Image source: Getty Images.

The bank still has a lot of ground to make up before its profitability exceeds its cost of capital. Higher interest rates and the current presidential administration's vow to deregulate the financial services industry will certainly help. But those things will take time to filter through to Bank of America's bottom line.

In sum, there's a reason bank investors responded the way they did in the wake of the presidential election, but that response has ensured that Bank of America's shares are no longer cheap.

I am by no means arguing you should sell its shares. However, I am saying that you shouldn't buy its stock today with the expectation that it'll go a lot higher in the foreseeable future.

10 stocks we like better than Bank of AmericaWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now...and Bank of America wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017.

John Maxfield owns shares of Bank of America. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.