The Simple Concept Underlying U.S. Bancorp's Dominance

Even if you compare U.S. Bancorp (NYSE: USB) to the best in the banking business, it still dominates the competition. For seven consecutive years, it has ranked first among big banks in terms of return on equity, the preeminent profitability metric in the industry.

I've studied U.S. Bancorp over the years in an effort to figure out how it does this -- especially how it does so year in and year out. The short answer is that the Minneapolis-based bank is highly efficient, spending a smaller share of its revenue on operating expenses each year than even the notoriously efficient Wells Fargo.

Data source: Quarterly earnings reports. Chart by author.

But there's more to U.S. Bancorp's perennial outperformance than just this. Efficiency is a necessary but not sufficient condition of dominance in the bank industry. A bank must be efficient to outperform its peers, in other words, but efficiency alone doesn't capture the whole picture. It instead merely ignites and accelerates what may best be described of as a force of nature, akin to the law of compounding returns.

Jim Collins in his book Good to Great analogizes this force of nature to a flywheel. It takes effort to get the wheel spinning, and more effort to make it go faster, but at a certain point, Collins notes, there's a breakthrough when the laws of physics take over:

No company illustrates the power of this concept better than Amazon.com, which, as Brad Stone writes in The Everything Store, incorporated Collins' flywheel into its operating philosophy more than a decade and a half ago.

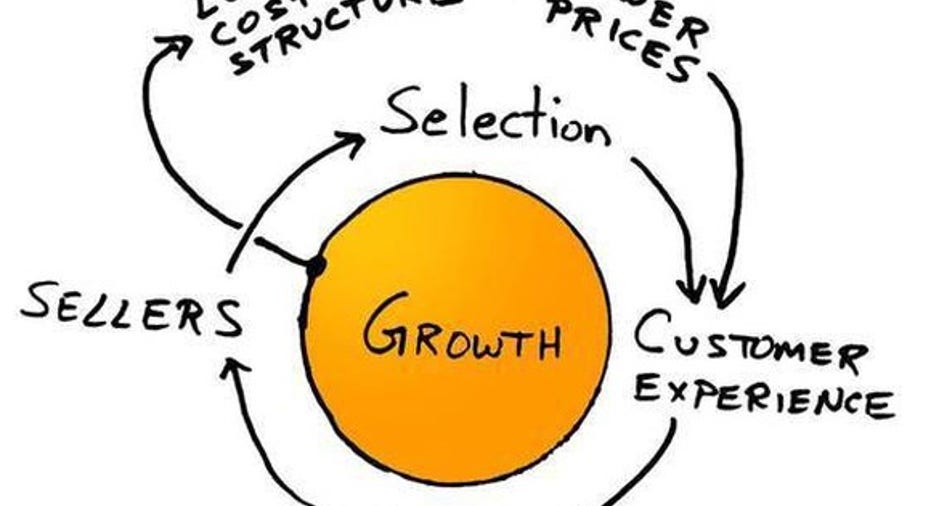

In Amazon's version, a low-cost structure enables the e-commerce giant to offer lower prices than its competitors. Lower prices lead to happier customers, which leads to higher traffic on its website. Higher traffic encourages new sellers to join Amazon's marketplace, which increases selection. And a better selection improves the customer experience, which powers a new revolution of the flywheel.

The Virtuous Cycle, as drawn by Amazon. Image source: Amazon.

Although Amazon and U.S. Bancorp are very different companies, the flywheel concept works in a similar way for the $446 billion bank. In fact, given the unique dynamics of banking, it may be an even more powerful force in the financial services arena.

By operating more efficiently than its peers, U.S. Bancorp can underprice them in the credit space. This attracts high-quality borrowers, boosting loan volumes and reducing loan losses. The latter keeps a lid on credit costs and thereby enables U.S. Bancorp to be even more competitive with respect to loan terms on the next revolution of the flywheel. It also buttresses the bank's debt rating, which keeps its interest expenses low and thus acts as added accelerant. Holding all else equal, then, with each turn of the flywheel, U.S. Bancorp should widen its competitive advantage over its peers.

This chain of events isn't just theoretical. Here's U.S. Bancorp Chairman and CEO Richard Davis connecting the dots between its low-cost debt and heightened pricing power on a conference call with analysts in 2015:

As I've demonstrated in the past, moreover, there's a clear correlation between efficiency ratios and loan losses among the nation's biggest banks. This follows from the fact that less efficient banks must stretch for yield in their loan portfolios in order to generate the double-digit returns on equity earned by more efficient banks. And because higher yields reflect higher risk, less efficient banks tend to write off a larger share of their loan portfolios during recessions such as the one following the financial crisis eight years ago.

Data source: S&P Global Market Intelligence. Chart by author.

The irregular but not infrequent undulations of the credit cycle further accelerate this, as banks that play fast and loose with credit risk are more likely to fail when the economy takes a turn for the worse. And even short of insolvency, a bank that takes large loan losses in a downturn is in no position to pick up its less prudent peers for pennies on the dollar when they run into trouble, which is one of the most effective ways to grow a bank and maximize returns over the long run.

What all of this means is that U.S. Bancorp should continue to outperform its peers in the years ahead. Its stock isn't cheap, and Davis is retiring later this year, but I don't believe that either of these alter the investment thesis underlying its stock.

10 stocks we like better than US BancorpWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and US Bancorp wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017

John Maxfield owns shares of U.S. Bancorp and Wells Fargo. The Motley Fool owns shares of and recommends Amazon. The Motley Fool has a disclosure policy.