Time to Think Differently About Investing in UPS and FedEx Stock?

Now that the dust has settled on a disappointing set of earnings from United Parcel Service, Inc.(NYSE: UPS), it's time to look at whether the investment case for the stock has changed. In common with key rival FedEx Corporation (NYSE: FDX), UPS is seeing strong e-commerce growth pressuring its margin, while it's increasing its capital spending plans to expand network capacity. Do all of these developments change how to think about investing in the stocks?

Margin pressure and capital expenditures

Back in December, FedEx reported on its second quarter and outlined how strong e-commerce growth (average daily volume growth of 5% in its ground segment) led to a 9.1% increase in revenue at FedEx ground. However, the increase was more than offset by a 12.2% increase in operating costs at ground, and ultimately FedEx ground operating income declined 11.6% in the second quarter.

The reason?Staffing and transportation costs increased to deal with surging e-commerce volumes, and FedEx ground costs increased as the companyprepared to expand its network capacity to deal with future growth.

Image source: Getty Images.

Fast-forward to UPS' results, and it's a similar story -- only it's worse. UPS' U.S. domestic package segment revenue (more than 70% of the segment's revenue is from ground) increased 6.3% in the fourth quarter, but margin pressure meant that adjusted operating profit for the segment fell 0.6%.

Ultimately, UPS got hit by two issues in the quarter:

- A significant mix-shift toward lower-revenue product deliveries, partly affected by strong residential e-commerce delivery growth.

- Increased costs from facility investments that haven't come on line yet. FedEx said almost exactly the same thing.

UPS' fourth-quarter earnings encompass the whole holiday season, and traditionally it's the strongest quarter of the year. However, when looking at profit growth between the third and fourth quarters in recent years, we see a significant deterioration in the relationship:

Data source: United Parcel Service, Inc presentations. Chart by author.

In addition, UPS announced that it will increase its capital expenditures to $4 billion in 2017, compared with $3 billion in 2016, a figure that represents more than 6% of forecast revenue in 2017 -- a ratio far higher than the 10-year average of 4.3%.

Data by YCharts.

Increased investments

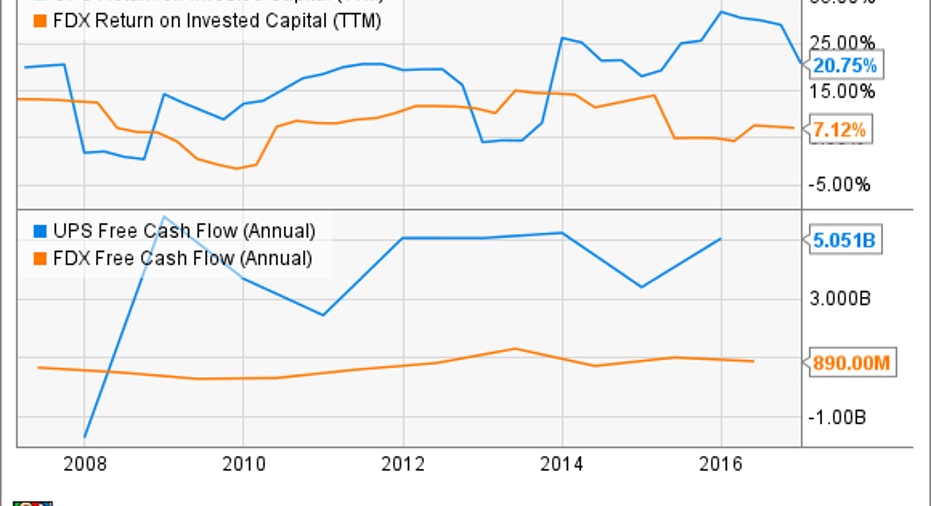

The earnings call made it clear that UPS' management believes the investments are necessary to service strong future growth and raise margin and profitability in the years to come. However, the question is whether the combination of margin pressure from a less favorable product mix -- business-to-consumer growth shows no signs of slowing -- and the increased capital expenditures necessary to service e-commerce growth will ultimately both eat into free cash flow generation and return on invested capital.If they do, then UPS' potential to grow its dividend, and with it the potential for shareholder returns,will be reduced.

Data by YCharts.

Scott Group, analyst with Wolfe Research, asked a related question on the earnings call, to which UPS CFO Richard Peretz replied, "I think one thing to keep in mind here is our priorities have always been the same, which is, first, is to reinvest in the business because of the high ROIC being ... mid-20s or higher." He added, "I think how you should think about the capex is for the next several years, we'll be a little higher than we have been, say, the last six or seven years."

More details will come at the UPS investor conference on Feb. 21, but it's safe to say we know capital expenditures are going up. However, revenue and profit will need to increase to push operating cash flow higher, so as to counteract the planned increase in capital expenditures. This matters, because companies usually seek to grow free cash flow (operating cash flow minus capital expenditures) in order to increase dividends, make stock buybacks or acquisitions, or pay back debt.

It matters even more because neither stock is priced cheaply on a free cash flow basis:

Data by YCharts.

Has the investment thesis changed?

FedEx and UPS are proactively taking measures to improve profitability (dimensional-weight pricing, adjusted oversize package surcharges, and so on), but it's proving harder than anticipated to grow margin with e-commerce deliveries. In a nutshell, we know capital expenditures are likely to go up, but we can't be clear on whether FedEx and UPS have a handle on increasing profitability with e-commerce deliveries.

All told, investors should feel a little less comfortable holding UPS and FedEx, particularly at these valuation levels. E-commerce growth is creating challenges, and it's not clear yet that both companies are overcoming them in terms of margin and cash flow generation.

10 stocks we like better than United Parcel Service When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and United Parcel Service wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of January 4, 2017

Lee Samaha has no position in any stocks mentioned. The Motley Fool recommends FedEx and United Parcel Service. The Motley Fool has a disclosure policy.