There Are Only 2 Acceptable Reasons to Go Into Credit Card Debt, New Survey Shows

Image source: Getty Images.

Credit card debt: for most Americans, it's a necessary means to paying bills. But it's also a major source of embarrassment for credit card holders, at least according to a newly published study from NerdWallet.

It's probably no secret that America runs on credit. According to a separate NerdWallet study, as of 2016 the average household had $132,529 in debt, leading to average annual interest costs of approximately $1,300. Separate data from ValuePenguin found that 38.1% of all American households had some sort of debt, with revolving credit card debt totaling a whopping $929 billion as of May 2016. That's up from $841 billion in outstanding revolving debt since 2010.

While not all debt is equal, credit card debt is often stigmatized as being "bad" since it only serves to weigh on incomes and causes the accountholder emotional stress. However, this bad form of debt is deemed acceptable in a select few scenarios, as you'll see below.

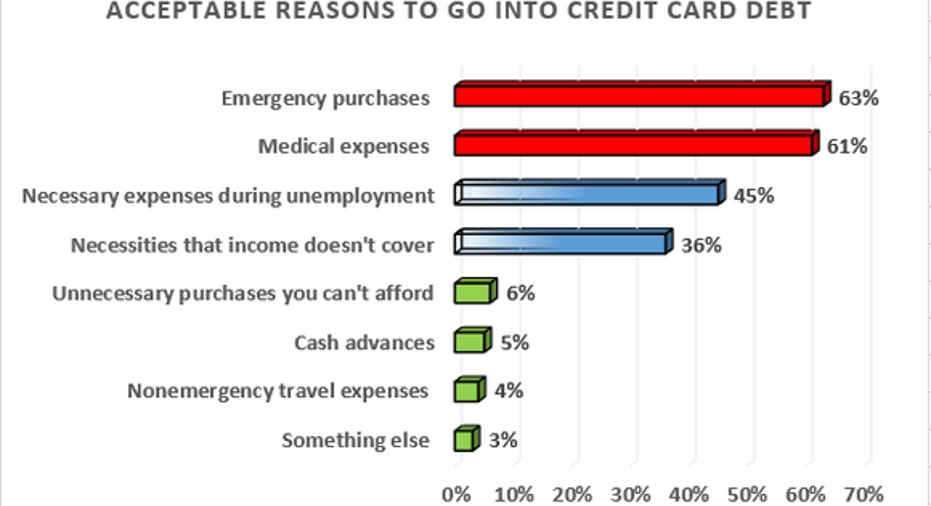

Acceptable reasons to go into credit card debt

NerdWallet's latest survey questioned more than 2,000 adults across the U.S. on various debt topics. Among the most intriguing responses was that 86% of Americans say there are acceptable reasons to go into credit card debt, while a nearly equal number of Americans (87%) believe that going into credit card debt is embarrassing.

What's acceptable, you wonder? Let's have a look.

Here's what 2,062 adults suggested were acceptable reasons for going into credit card debt:

Data source: NerdWallet. Chart by author.

As you can see from the answers above, just two of the eight choices were "acceptable" reasons to go into credit card debt according to the respondents. Nearly two-thirds of the respondents suggested that emergency purchases are an acceptable reason to use a credit card, while medical expenses came in a very close second at 61%. Considering that large medical bills and emergencies are a common source of unexpected costs and bankruptcies, it's not one bit surprising to see a majority of Americans support the idea of using their credit cards in such a scenario.

On the other hand, covering necessary expenses while unemployed, as well as necessities that your current income doesn't cover, didn't get a majority of responses, though both were somewhat close at 45% and 36%, respectively. Unnecessary purchases, cash advances, and nonemergency travel expenses didn't even crack the double-digits.

Problem, meet solution

The real problem here is that many credit cardholders simply aren't doing a good job of saving money, and they clearly don't have the wherewithal to live their lives on a budget (at least based on the figures from this survey).

Data from the St. Louis Federal Reserve from December shows that the personal saving rate in the U.S. was just 5.4%, which is a far cry from the 12.1% Americans were socking away in Dec. 1966, and it's also well below what citizens in most developed countries save as a percentage of their income.

Image source: Getty Images.

Likewise, national pollster Gallup found in 2013 that only 32% of American households kept detailed monthly budgets. This essentially meant that 68% of households were crossing their fingers and hoping for the best, because without a detailed monthly budget it's practically impossible to understand your cash flow and optimize your saving and spending habits.

The fix to these issues appear to be one and the same: a budget. If more Americans with credit cards were regularly using and sticking to budgets, the requisite "embarrassment" described by NerdWallet that comes along with racking up a large amount of credit card debt would probably be substantially reduced.

Formulating the perfect budget and kissing those debt worries goodbye

There are really two challenges when formulating a budget.

First, you have to formulate an airtight budget that's going to allow you to successfully save money and keep your credit card spending below your income level. The good news in this respect is that budgeting software can do most of the grunt work for you nowadays. Budgeting software handles all of the adding and subtracting, and it can even help you formulate a pathway to save if you provide it with your weekly, monthly, or yearly savings goal.

One of the best things you can personally do to ensure that your budget makes sense is to employ the "S.M.A.R.T." system. The "SMART" acronym stands for:

- Specific

- Measurable

- Achievable

- Realistic

- Time-based

Image source: Getty Images.

In other words, being a SMART budgeter means developing a saving and spending plan that has specific, achievable, and realistic goals that allow you to easily measure your progress over the course of weeks, months, or the year. This way you'll be able to really understand your cash flow and what can be adjusted to optimize your ability to save. More importantly, these added savings could keep you from reaching for your credit card if an emergency arises.

Once you've handled the structural components of your budget, it's time to tackle the mental ones. In other words, it's time to ensure that you stick to your budget. The best way to do that is to get people who share like-minded values involved. This means getting everyone else under your roof involved in a household budget (kids and grandparents included), as well as potentially meeting up with a group of people who share your saving values once every couple of weeks. The more you surround yourself with other people who are budgeting, the more likely you are to remain on your own budget.

Another idea that could help avoid the temptation to buy unnecessary things is to consider using separate accounts for each spending category. In effect, if you've set aside $200 in entertainment expenses for the month, keep that $200 separate from your checking and savings account so you aren't tempted to overspend. Even using something as crude as jars in a cabinet could wind up being effective for those who have trouble resisting the urge to overspend.

America may run on credit, but that doesn't have to be a bad thing if you have an airtight budget in your back pocket.

The $15,834 Social Security bonus most retirees completely overlook If you're like most Americans, you're a few years (or more) behind on your retirement savings. But a handful of little-known "Social Security secrets" could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $15,834 more... each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we're all after.Simply click here to discover how to learn more about these strategies.

The Motley Fool has a disclosure policy.