Only 1 In 4 Americans Are Making This Smart Move With Their Money

Scared that your retirement savings will fall short in retirement? You're not alone. Millions of Americans have yet to recover from the financial damage inflicted upon them during the Great Recession.

Getting back on the right financial track isn't simple, but it can be done, and according to Fidelity Investments' number crunchers, some American workers are making one very important decision that can allow them to achieve financial security. Over 25% of 401(k) participants increased how much of their income they're contributing to their retirement plan last year. If you were among those savvy savers, great. If not, then here's why it might be time to follow their lead.

IMAGE SOURCE: GETTY IMAGES.

A big dilemma

Common wisdom is that retirees should withdraw no more than 4% of their savings annually, if they don't want to outlive their money.

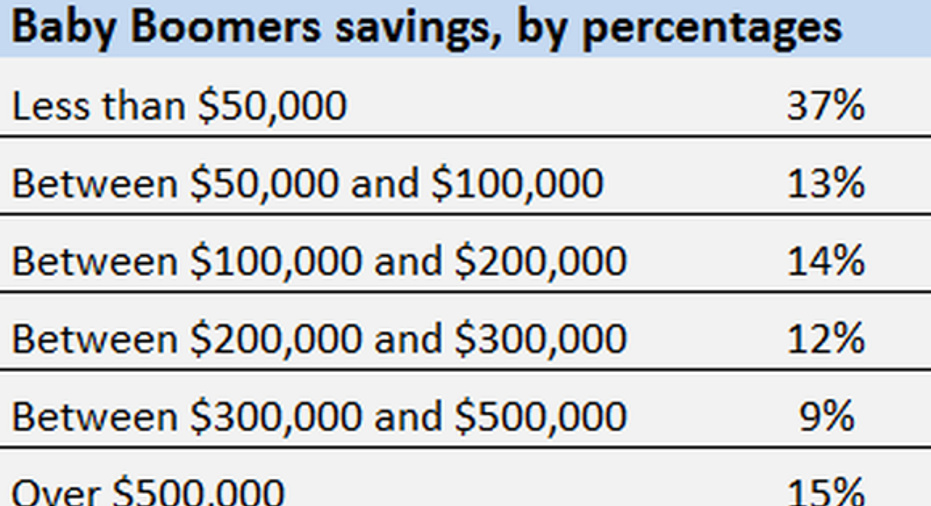

That's prudent advice, but the reality is that few Americans will be able to maintain financial independence in retirement with a withdrawal rate so low. Why? Because most Americans' savings are limited. For example, a PWC survey last year found that about half of baby boomers have less than $100,000 in retirement savings, a worrisome figure when you consider how close they are to retirement and that 4% rule:

DATA SOURCE: PWC EMPLOYEE FINANCIAL WELLNESS SURVEY. TABLE BY AUTHOR.

Spending does fall in retirement, mostly because homes have been paid off and transportation costs decline, but the average retiree still spends nearly $45,000 per year, according to the Bureau of Labor Statistics, and that means that retirees are relying heavily on Social Security.

If that's your retirement plan, you might want to reconsider. In 2017, the average person will only receive $1,360 per month in Social Security income, or $16,320 per year. That's hardly a windfall.

Steps in the right direction

Fidelity's research shows that the average 401(k) account increased last year, and undeniably, the 236% move upward in the S&P 500 since March 2009 has helped repair a lot of the average American's balance sheet. However, it's not just rising stock prices that contribute to thickening balances. Rising worker-contribution rates have a lot to do with it too.

Fidelity reports that American workers are contributing 8.4% of their income to their 401(k) plans. That's the highest contribution rate observed by Fidelity since the second quarter of 2008, and those contributions, plus matching contributions from employers, helped the average 401(k) account balance grow to $92,500 in 2016 from $88,200 in 2015.

Getting on the right track

Contributing 8.4% of your income to a workplace retirement plan is a good start, but that's still unlikely enough to allow you to reach the maximum contribution allowed every year. In 2017, $18,000 in earnings can be contributed to 401(k) and 403(b) plans, plus an additional $6,000 can be contributed if you're age 50 or older.

You probably won't be able to increase your contribution enough to reach that limit all at once, but bumping up your contribution rate by even 1% to 2% per year can make a big difference to your future account balance, without busting your budget.

For example: Jane is 35 and she makes $50,000 per year. If she contributed 8% of her income to her retirement plan annually, and earned an average annual return of 6%, she could have a nest egg worth $316,229 at age 65. If she upped that contribution rate to 10%, her account could be worth $395,294 at 65, and if she boosted it to 12%, it could be worth $474,349. If we use the 4% rule to calculate how much of her savings she can safely withdraw in retirement, she would be able to take out $18,973 at age 65 in the 12% scenario -- roughly 50% more than she would be able to withdraw if she contributed only 8%.

The $15,834 Social Security bonus most retirees completely overlook If you're like most Americans, you're a few years (or more) behind on your retirement savings. But a handful of little-known "Social Security secrets" could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $15,834 more... each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we're all after.Simply click here to discover how to learn more about these strategies.

The Motley Fool has a disclosure policy.