1 Simple Social Security Fix Could Boost Lifetime Payouts by Nearly $30,000, Study Shows

Image source: Getty Images.

Social Security is a program that more than 41 million retired workers rely upon each and every month. According to the Social Security Administration (SSA), 71% of unmarried elderly individuals, and 61% of elderly individuals as a whole, receive at least half of their monthly income from Social Security.

However, Social Security was never meant to be leaned on so heavily by retirees. The SSA suggests that Social Security benefits are only designed to replace about 40% of your working wages. Yet based on the data above, we know that 3 out of 5 seniors would likely be in serious trouble without Social Security income. According to the November SSA snapshot, the average retired worker brings home $1,354.78 a month, or about $16,260 a year. That's (depressingly) not too far from the federal poverty level of $11,880.

Hey Social Security, you're doing it wrong!

Yet, according to a new study from The Senior Citizens League (TSCL), a nonpartisan organization designed to keep senior citizens and retirees abreast of the policy decisions that can affect them, a simple change to Social Security could give retirees a considerably brighter outlook and, according to the report, net the average retiree in 2015 nearly $30,000 extra in lifetime benefits over 25 years.

A notable problem TSCL has identified with Social Security is the method by which cost-of-living adjustments, or COLAs, are calculated. Social Security COLAs are the "raises" beneficiaries receive most years.

Image source: Getty Images.

Social Security's COLA is calculated based on changes in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). The CPI-W is designed to measure the change in the price of a predetermined basket of goods and services. To calculate Social Security's COLA, the average CPI-W reading from the third quarter of the previous year acts as the baseline figure, while the average CPI-W reading from the third quarter of the current year serves as the comparison. If there's a year-over-year decline in the average CPI-W readings, no COLA is given. If, however, there is an increase, Social Security beneficiaries receive the difference, rounded to the nearest 0.1%.

But, as TSCL points out, the CPI-W has a fatal flaw: it represents the spending habits of working Americans, not senior citizens, despite the fact that two-thirds of all Social Security recipients are retired workers.

This "fix" could put nearly $30,000 in retirees' pockets over their lifetime

According to TSCL, the solution would be to switch the COLA measure to the Consumer Price Index for the Elderly (CPI-E). As the name implies, the CPI-E only factors in the spending habits of households with individuals who are 62 and older.

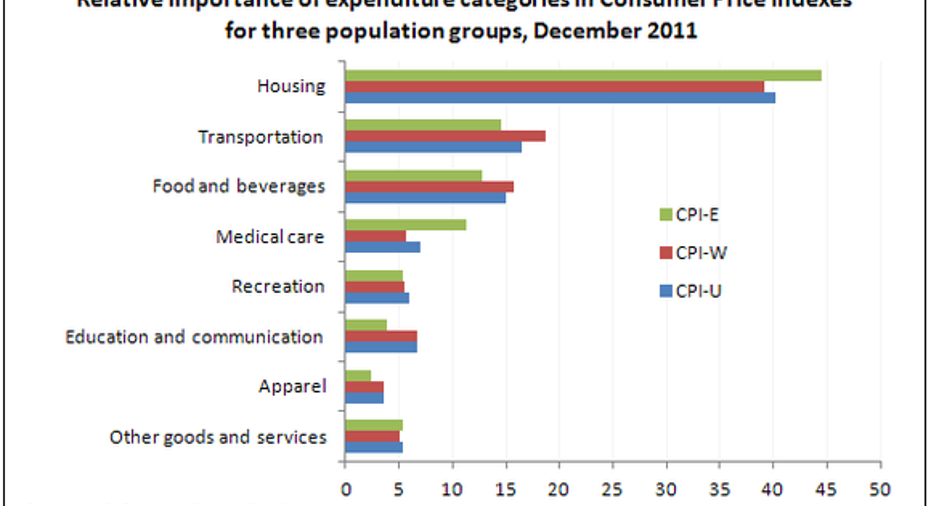

As you can see by the Dec. 2011 comparison of the CPI-W and the CPI-E below, the weighting of expenditures is quite different for certain categories. For example, seniors spend twice as much on medical care as do working Americans. They also tend to spend more on housing. By comparison, the CPI-W places a higher emphasis on education, apparel, entertainment, and transportation expenses.

Image source: U.S. Bureau of Labor Statistics.

These percentages may not look large on this Bureau of Labor Statistics comparison, but over the course of 25 years using the CPI-E instead of the CPI-W could be expected to increase annual payouts by an average of 8.9%, or $29,568 in aggregate, based on the current average monthly payout of $1,355 a month for retired workers.

What's more telling is that over the past 33 years, the CPI-W would have resulted in a greater annual COLA than the CPI-E on just three occasions (2006, 2009, and 2012). In the remaining 30 years, the CPI-E would have provided a substantially higher COLA, which would presumably allow seniors to more comfortably afford the rising cost of medical care. Not surprisingly, medical care inflation has outpaced Social Security's COLA in 33 of the past 35 years.

The CPI-E has its flaws, too

On one hand, TSCL makes a strong case for the CPI-E considering that seniors make up a majority of Social Security recipients, and given that they're falling far behind the medical care inflation curve. But the CPI-E brings its own set of problems to the table.

To begin with, there are far more working Americans than there are seniors. In other words, even though the CPI-W doesn't perfectly match the spending habits of seniors as outlined in the BLS chart above, it arguably creates a more accurate picture of the spending habits of Americans than the CPI-E because it has so many additional data points for analysis.

Image source: Getty Images.

Another concern is that the CPI-E doesn't factor in the rising cost of Medicare Part A expenses. Part A is the hospital insurance component of Medicare, and it covers in-patient costs, surgeries, and long-term skilled nursing care. Part A costs can be extensive, and if they aren't factored into the CPI-E seniors could still wind up falling way behind the medical care inflation curve, even if the CPI-E were being used to calculate COLAs instead of the CPI-W.

Lastly, and this could arguably be the biggest issue of all, switching to the CPI-E, could also expedite how quickly the Social Security Trust burns through its spare cash. TSCL's calculations demonstrate that seniors would receive a higher COLA in most years than with the CPI-W, which means even more pressure on Social Security.

Will the CPI-E debate gather steam on Capitol Hill? It's really anyone's guess at this point, but considering that Republicans are in charge of Congress for at least the next couple of years, and many of them favor moving to a Chained CPI (a measure that produces even slower growing COLAs than the CPI-W), I wouldn't hold my breath.

The $15,834 Social Security bonus most retirees completely overlook If you're like most Americans, you're a few years (or more) behind on your retirement savings. But a handful of little-known "Social Security secrets" could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $15,834 more... each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we're all after.Simply click here to discover how to learn more about these strategies.

Sean Williamshas no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen nameTMFUltraLong, and check him out on Twitter, where he goes by the handle@TMFUltraLong.The Motley Fool has no position in any of the stocks mentioned.The Motley Fool has adisclosure policy.