Better Buy: Silver Wheaton Corp. vs. Vale SA

On the surface, giant iron-ore-focused miner Vale SA (NYSE: VALE) and gold- and silver-streaming company Silver Wheaton (NYSE: SLW) don't appear to have too much in common. Investors willing to do a little more analysis, however, will quickly see that both are facing external issues that could have a material impact on their business outlooks for years to come, which is why most investors should err on the side of caution with this pair.

Samarco reconstruction efforts. Image source: Vale SA.

Disasters and taxes

The end of 2015 was really bad for Vale. A containment system for mine waste at the Samarco mining operation, which is owned 50/50 by Vale and BHP Billiton (NYSE: BHP), ruptured on the afternoon of Nov. 5. Two towns were destroyed and multiple lives were lost. Needless to say, 2016 started on a weak note.

Last year, however, a roughly $6 billion legal settlement with Brazil was reached, with costs stretched out over more than a decade. However, there are additional claims (around $42 billion worth) that could materially increase Vale's costs for moving past Samarco. Although there's some clarity for Vale and its partner since they've come to an agreement on how that bill will be resolved, the duo's financial exposure is still open-ended. And the financial impact will linger for years even after all the legal issues are ironed out.

Silver Wheaton, meanwhile, has been fighting with the Canadian government over its tax bill. It started out with a look at the 2005 to 2010 tax years, but in 2016 was expanded to include 2011 to 2013. And since Silver Wheaton believes it is preparing its taxes correctly, investors should expect the inquiry to end up including every year up to the final resolution of the issue.

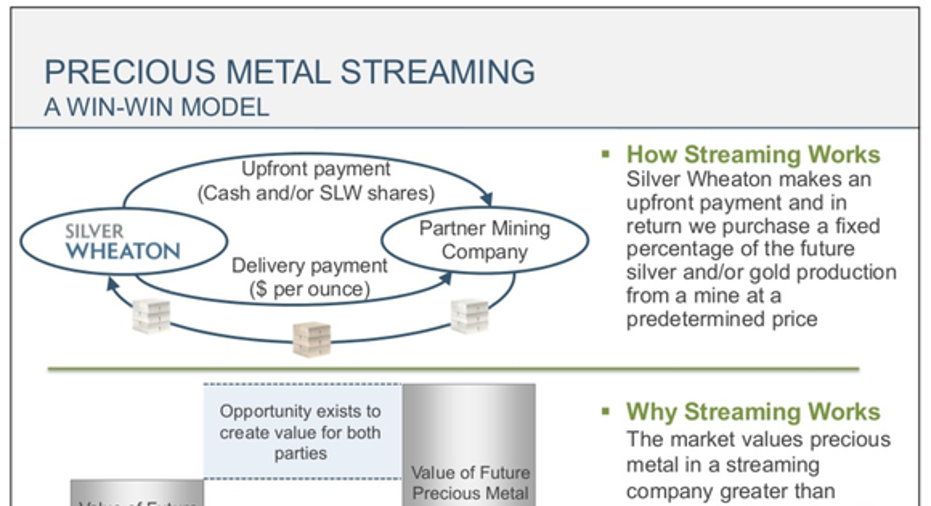

Silver Wheaton's streaming business model explained. Image source: Silver Wheaton.

The bill, which back-of-the-envelope math puts in the $500 million range at last count, isn't nearly as large as the one facing Vale. However, Silver Wheaton isn't nearly as large a company. To put some perspective on that, Silver Wheaton's net earnings through the first nine months of 2016 were around $185 million. That makes my estimate of half a billion dollars look pretty material. More important, however, is the potential impact on future profits, which would likely be lower if the company has to pay higher taxes on an ongoing basis.

So both companies are facing notable external issues that could have a lingering impact on their businesses. Still, of the two, Silver Wheaton's tax problem looks a lot less worrisome than Vale's disaster-related legal issues.

The businesses behind the names

But you also have to examine these troubles in relation to the broader businesses. Silver Wheaton is a streaming company, which means it gives upfront payments to miners for the right to buy gold and silver at reduced rates in the future. Those costs, which are around $4 an ounce for silver and $400 an ounce for gold, are extremely low and locked in. And since it avoids the expense and complication of running mines, its business tends to be relatively predictable even though volatile commodity prices have a material impact on the top and bottom lines.

Vale's costs were pretty high not too long ago. Image source: Vale SA.

Vale, on the other hand, has to deal with volatile commodity prices and the risks inherent to mining. Samarco is proof of the largest risks, but a lesser risk is the cyclical nature of mining costs. Right now Vale's costs look like they are heading lower as it completes its massive S11D iron ore project. But the fact that Vale was able to reduce its costs by 31% between 2012 and 2016 shows that costs can get out of hand if they aren't strictly controlled. That's hard to do when times are flush, like they were in the years leading up to the commodity peak in 2011.

So Vale's core business looks good today, with low costs ahead. But investors can't count on that to last if the recent upturn in commodity prices proves unsustainable. Excess is simply a part of the mining cycle. Silver Wheaton, which isn't a miner, pretty much avoids that.

When you add it up, less is more

Vale is facing an uncertain legal future because of the Samarco mine disaster. Silver Wheaton is in the midst of a tax spat with the Canadian government. Of the two, Silver Wheaton's troubles are less onerous. That alone could make it a better option for investors. Now layer on the fact that Silver Wheaton's business model locks in low prices for the commodities it sells and Vale is exposed to both volatile commodity prices and often unpredictable mining costs, and Silver Wheaton looks even better. Most investors would be better off erring on the side of caution here.

10 stocks we like better than Silver Wheaton When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Silver Wheaton wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of January 4, 2017

Reuben Brewer has no position in any stocks mentioned. The Motley Fool owns shares of Companhia Vale and Silver Wheaton. The Motley Fool has a disclosure policy.