The Average American Got a $4,886 Tax Deduction by Doing This. Will You?

Tax season is almost here, and if you're like most taxpayers, you'll soon be looking high and low for ways to pay less to Uncle Sam -- or to get a bigger refund. One way that most Americans can cut their tax bill and take a step forward in saving for retirement is to contribute to a traditional IRA. Indeed, the average taxpayer who took advantage of this tax break got a deduction of nearly $5,000. Yet only a tiny fraction of those who are eligible actually make those deductible contributions. Let's look more closely at deducting contributions to traditional IRAs to see whether you could benefit from doing so.

Image source: Getty Images.

Why a traditional IRA contribution is a smart move

The most common reason why people contribute to traditional IRAs to save for retirement is that they can usually deduct the amount they contribute from their current-year tax return. For 2016 and 2017, as long as you have earned income from a job or business, the maximum contribution to an IRA is $5,500. Those who are 50 or older can make an additional catch-up contribution of $1,000.

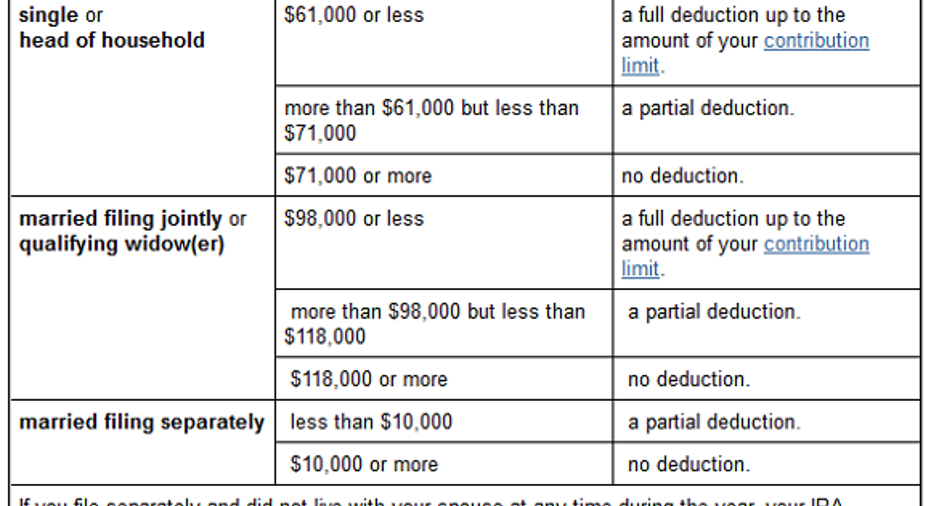

Traditional IRA contributions are eligible for a full deduction if neither you nor your spouse (if you're married) has a retirement plan through an employer. Even those who do have access to a 401(k) or similar plan from their employer can deduct their contributions to a traditional IRA, so long as they qualify under income limits. Those limits are summarized below.

Image source: IRS.

Moreover, higher limits apply to those whose spouses are covered by a plan. Joint filers contributing to an IRA for the 2016 tax year can get a full deduction with income up to $184,000, and that deduction phases out between $184,000 and $194,000.

Yet hardly anyone actually takes advantage of the IRA deduction for contributions. Only about 2.7 million taxpayers claimed the deduction in the most recent year for which data is available, according to the IRS. The data shows that the total deductions taxpayers claimed on IRA contributions totaled up to roughly $13.2 billion. Using the precise figures from the IRS data, that amounts to $4,886 per return. That figure suggests that those who do use IRAs are contributing close to the full permitted amount, although the figure includes joint returns that may include both spouses' contributions.

A $4,886 deduction could lower your tax liability by between $489 and $1,935, depending on your tax bracket. However, based on the fact that more than 148 million returns got filed that year, less than one in every 50 American households claimed the IRA deduction to boost their savings for retirement.

A second tax break you might be able to take

In addition, some taxpayers can get even more money back from the IRS if they contribute to an IRA. The Retirement Savings Contributions Credit is a credit of between 10% and 50% of the first $2,000 that qualifying savers contribute to a qualifying retirement account. In addition to IRA savers, anyone who participates in a 401(k) plan is eligible.

That said, only those who meet the credit's stringent income restrictions can claim the credit. As you can see below, you must have adjusted gross income of less than $30,750 (if you're a single filer) or $61,500 (if you're a joint filer), and the limits are even lower for the larger credit amounts. For those who do qualify, the credit can add up to $1,000 in further tax savings. About 7.9 million American taxpayers took advantage of the credit in the most recent year, and their credits amounted to more than $1.38 billion -- roughly $175 per return.

Image source: IRS.

So why don't more people make traditional IRA contributions? For one, if you have a 401(k) plan or a similar retirement plan at work, then it's often easier to use that instead of an IRA. In addition, if you're fortunate enough to get matching contributions from your employer, then you definitely won't want to pass up that opportunity. Many people don't have enough savings to take advantage of both their 401(k) and an IRA.

In addition, note that the IRS data looks only at deductions for traditional IRAs. Some taxpayers use Roth IRAs instead, which offer tax-free withdrawals in retirement of all the assets -- including income -- that your retirement assets generate throughout your career, instead of an up-front deduction. Roth IRA contributions also count for the Saver's Credit.

Still, what a traditional IRA offers that a 401(k) doesn't is the ability to turn back time and make contributions that you can deduct on your 2016 tax return. This year, you have until April 18 to do so. With all the advantages that traditional IRAs offer, that last-minute capability to cut your tax bill could make a traditional IRA contribution the best choice you have.

The $15,834 Social Security bonus most retirees completely overlook If you're like most Americans, you're a few years (or more) behind on your retirement savings. But a handful of little-known "Social Security secrets" could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $15,834 more... each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we're all after.Simply click here to discover how to learn more about these strategies.

The Motley Fool has a disclosure policy.