5 Growth Stocks That Could Double

Image source: Getty Images.

Finding stocks that could double is every investor's dream, and we're always on the lookout for potential multibaggers here at The Motley Fool. We asked five contributors to name possible candidates, from restaurants to online retailers to a social-media service in need of a turnaround, among others.

Here's why Dave & Buster's Entertainment (NASDAQ: PLAY), ANI Pharmaceuticals (NASDAQ: ANIP), Wayfair (NYSE: W), Shopify (NYSE: SHOP), and Twitter (NYSE: TWTR) should be on your watch list.

A unique restaurant play

Daniel Miller (Dave & Buster's Entertainment Inc.): Eat. Drink. Play. Watch. That's the cornerstone strategy behind Dave & Buster's Entertainment's initial success as a public company. The "eat, drink, play, and watch" concept has proven its effectiveness, Dave & Buster's store financials are strong, and its growth story has room to run.

While the company is young, its brand is already widely recognized, with 93% awareness among casual-dining consumers in existing markets, according to the company's 2016 investor presentation. Further, its customers' average household income of $75,000-plus could help stave off drastic sales declines in the event of a slight economic downturn. The company's unique focus on games also helps fuel its strong financials, as you can see below:

Image source: Dave & Buster's 2016 fall investor presentation. EBITDA = earnings before interest, taxes, depreciation, and amortization.

The company's momentum is undeniable, with 24 consecutive quarters of trailing-12-month adjusted-EBITDA growth and record comparable-store sales growth of nearly 9% for fiscal year 2015. Heck, even with 2015's excellent results, the first half of fiscal 2016 increased 2.3% over the prior year's 10.4% comp-store sales growth. Its trailing-12-month revenues through the second quarter of fiscal 2016 checked in at $933.3 million, with an impressive adjusted-EBITDA margin of 26.2% -- as juicy as its cheeseburgers.

Dave & Buster's has two enticing points. The first is right here in the States: With only about 87 stores, management believes it can post annual store growth of 10% and reach a store count in excess of 200. Second, the international opportunity remains untapped, which won't be the case forever. Ultimately, this is a unique and proven concept with strong margins and a large growth story over the next decade, giving it the potential to double in the coming years.

There's something generic about this growth stock

Sean Williams (ANI Pharmaceuticals): Sometimes the most attractive growth stocks can be found in small-cap territory. My suggestion for investors would be to get drug developer ANI Pharmaceuticals on their radar.

ANI Pharmaceuticals is part of a growing class of what I like to call "hybrid drugmakers," which develop branded therapies as well as generic drugs. The trade-off is that branded drugs have much higher margins, but also a significantly higher likelihood of development failure and a relatively short period of patent protection. On the flip side, generic drugs have much lower margins, but there's a nearly endless sea of generic-drug opportunities, as well as a much higher success rate in getting generics to pharmacy shelves.

ANI Pharmaceuticals' most recent quarterly report featured a 93% year-over-year increase in sales, driven by a 100% increase in generic pharmaceutical products, which make up the bulk of its revenue, and a 203% spike in branded pharmaceutical sales. The company attributed the doubling in generic sales to the launch of 10 generic products from the fourth quarter of 2015 through the first three quarters of 2016.

At the moment, ANI has 78 products in development, with a combined market value of $3.7 billion. Of these 78, 53 were somewhat recently acquired, and 46 of those 53 should be relatively easy to commercialize, according to ANI. QuintilesIMS Institute for Healthcare Informatics predicts that generic-drug use is only going to grow in the years to come, so ANI could be a smart bet for growing sales and profits.

Furthermore, while ANI Pharmaceuticals didn't even generate $10 million in sales in 2010, Wall Street is projecting sales of $287 million and annual earnings per share of $7.61 by 2019. When it comes to growth stocks with a good chance to eventually double in value, this mighty mouse in the pharmaceutical industry could be just what the doctor ordered.

Revenue growth isn't enough

Tim Green (Wayfair): Online furniture retailer Wayfair is growing revenue by nearly 50% annually, but the market is valuing the company at less than sales. In other words, investors are intensely pessimistic about Wayfair's ability to become profitable. I'm pessimistic as well, but any indication that Wayfair is moving in the right direction could send the stock soaring.

Wayfair's business model, which relies on its suppliers shipping products directly to its customers, frees capital from being tied up in inventory. The downside is that Wayfair manages fairly dismal gross margins for a furniture seller -- around 24%. That doesn't leave much to spend onoperating expenses, and the need to advertise heavily is pushing Wayfair into the red. During the latest quarter, the company spent 11.8% of revenue on advertising; bringing that number down without hurting sales growth will be a challenge.

Wayfair is never going to be a high-margin company, but the market is clearly betting against the company ever turning much of a profit. If Wayfair can show progress next year in bringing down expenses and getting closer to profitability, investors might rethink the stock's pessimistic valuation.

Shares of Wayfair could easily double if the best-case scenario plays out. But there's also the risk that the stock tumbles, especially if growth begins to slow down without a shift toward profitability. I'm not a fan of Wayfair, and I won't be investing in the stock. But those who believe in the company's strategy could be rewarded handsomely if things work out.

An only retailer that isn't Amazon but could be just as rewarding

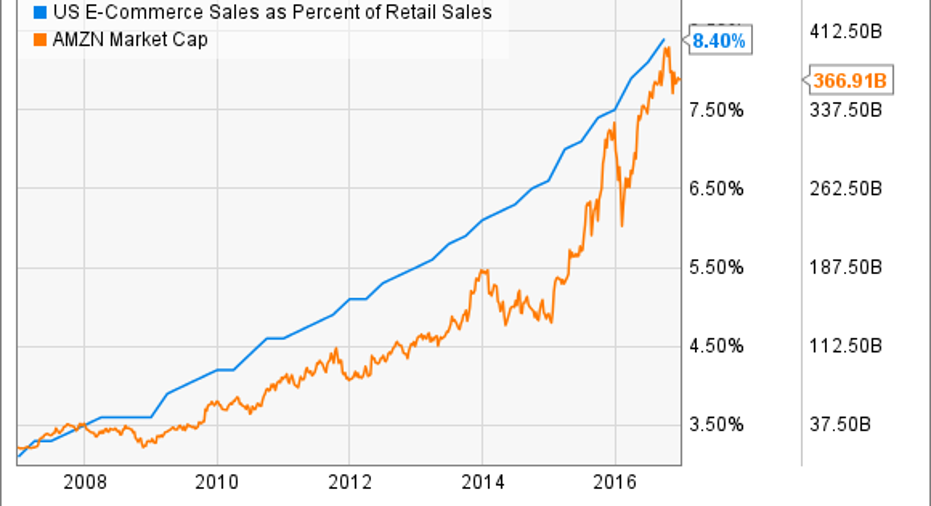

Jamal Carnette, CFA (Shopify): Over the last decade, the biggest shift in the U.S. retail landscape has been the tremendous shift to e-commerce. During this time frame, e-commerce has doubled from less than 4% of total retail sales to approximately 8.4%. E-commerce leader Amazon.com (NASDAQ: AMZN) increased its market capitalization approximately tenfold in this decade, as it has consolidated market share:

US E-Commerce Sales as Percent of Retail Sales data by YCharts.

However, with a market capitalization approaching nearly $400 billion, it will be difficult (though certainly not impossible) for Amazon to become a double-bagger from these levels even with near-flawless execution. Instead, I feel Shopify is the e-commerce company best positioned to double from current levels.

It's folly to directly compare the two companies; the comparison with Amazon is apt only in that both are poised to profit from the growth of the e-commerce industry. However, there are many features that separate the two. The most obvious differentiator is that Shopify provides an online marketplace hosted on merchants' websites, while Amazon's goods compete on its eponymous website.

Shopify is a plug-in software solution for merchants seeking to offer an online marketplace on their own sites. Shopify profits from monthly subscription and payment transaction fees while the merchant bears the traditional retail risks of inventory, pricing, and brand loyalty; Amazon sells its own inventory. In many cases Amazon is directly competing with third-party sellers using its platform, while Shopify and its merchants are not.

Shopify's value proposition has had strong demand. In the recently reported third quarter, Shopify grew revenue 89% over last year's corresponding quarter. However, gross merchandise volume -- the total value of orders processed through Shopify's software -- increased 100%, which points to increased growth. Although Shopify is currently unprofitable, it's only a $4 billion company. If it continues its torrid growth streak, profitability and stock gains should quickly follow.

A social media turnaround play

Evan Niu, CFA (Twitter): Considering my general skepticism regarding Twitter, it might strike some as odd that I think shares could potentially double from current levels. While I think Twitter has its fair share of problems, including an ongoing exodus of executives and the obligatory investor concerns around nonexistent user growth, the company has carved out a niche for itself within social media. The service has undoubtedly become a valuable platform to disseminate information and syndicate publications, as well as a part of mainstream culture.

If Twitter is able to address its plethora of underlying problems, including employee retention and weaknesses in its core service, it could potentially bounce back in a big way. CEO Jack Dorsey recently called out to the Twitter community for product-improvement suggestions, showing he's still aware that Twitter has plenty of work to do on the product front. If Twitter becomes easier to use, the improvements could attract more users.

Revenue growth decelerated significantly in 2016 (third-quarter revenue growth was just 8%), but the company used to put up growth rates of 30%, 50%, and higher; the company will need to reinvigorate growth if it wants more confidence from investors. Meanwhile, it could reduce how much stock-based compensation it grants, which would help the bottom line. Last quarter's stock-based compensation was greater than the total GAAP (generally accepted accounting principles) net loss, for instance. I don't necessarily think that Twitter will double, but it's a definite possibility if it can pull off a turnaround and begin executing.

10 stocks we like better thanWal-MartWhen investing geniuses David and TomGardner have a stock tip, it can pay to listen. After all, the newsletter theyhave run for over a decade, the Motley Fool Stock Advisor, has tripled the market.*

David and Tomjust revealed what they believe are theten best stocksfor investors to buy right now... and Wal-Mart wasn't one of them! That's right -- theythink these 10 stocks are even better buys.

Click hereto learn about these picks!

*StockAdvisor returns as of December 12, 2016The author(s) may have a position in any stocks mentioned.

Daniel Miller has no position in any stocks mentioned. Evan Niu, CFA has no position in any stocks mentioned. Jamal Carnette owns shares of Shopify. Sean Williams has no position in any stocks mentioned. Timothy Green has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Amazon.com, Shopify, Twitter, and Wayfair. The Motley Fool recommends Dave and Buster's Entertainment and Quintiles IMS Holdings. The Motley Fool has a disclosure policy.