Clean Energy Fuels Corp. May Be Destroying Value by Paying Down Debt

In 2016,Clean Energy Fuels Corp. (NASDAQ: CLNE) made substantial progress on improving its business. In a very challenging oil-price environment, the company still managed to grow the number of gallons it delivered to natural gas vehicle operators, while also continuing to lower its operating expenses and improve its gross margin.The company also paid down a pretty substantial chunk of debt in 2016, largely by selling stock so that it could preserve cash, something that I still think was a prudent move to make.

Image source: Getty Images.

However, the company announced on Dec. 21 that it was nearly doubling the number of shares available to sell under its ongoing "at the market" agreement from $110 million to $200 million, and then announced on Dec. 22 that it was purchasing $50 million of convertible debt for $42.75 million.

And while it's nice to see the company paying off debt at a discount, I'm not sure that selling stock at current levels is prudent, or creates value.Let's take a closer look at why that is.

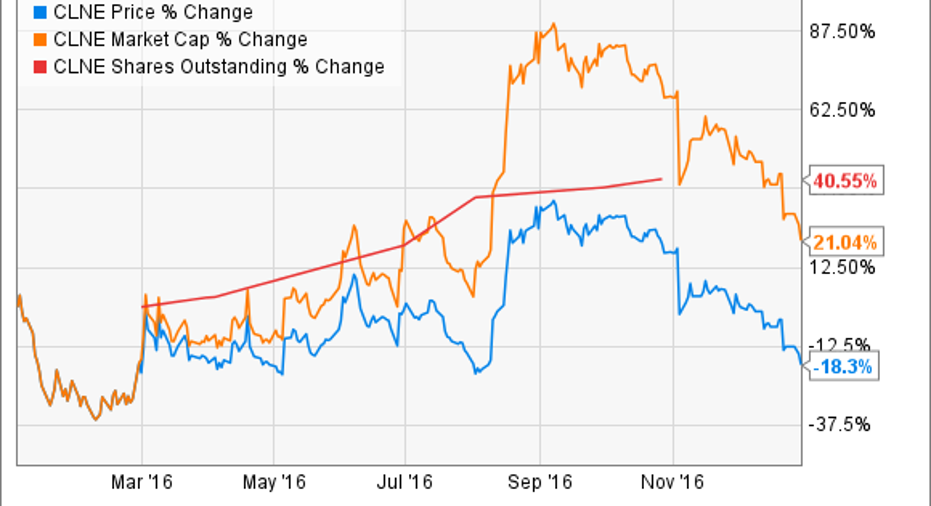

Clean Energy got bigger in 2016, but shareholders didn't benefit (yet)

Clean Energy Fuels' market cap grew significantly last year, but the enormous dilution from the new shares issued more than offset those gains on a per-share basis:

The reality is, the company had little choice beyond issuing new shares, with $150 million in debt due last August. But on balance, the dilution which clearly cost investors gains in 2016, is far more likely to benefit shareholders over the long term, because it positioned the company with a stronger balance sheet and lower expenses.

Why I supported last year's use of stock (but maybe not this year's)

Beyond the $150 million in debt due in 2016, management took advantage of multiple opportunities to buy back debt due in 2018 at substantial discounts, significantly reducing its total debt burden even before this recent repurchase. Not only does this deleveraging give the company more flexibility moving forward, but it also further cuts expenses. At the peak, Clean Energy was spending over $40 million per year on interest -- an amount that should be 40% lower in 2017. As I wrote, on balance, last year's moves were necessary and prudent.

But I'm not so sure that this will remain the case if management continues selling stock at current levels, particularly with no major debt obligations due before mid-2018.

It boils down to value creation for shareholders

On one hand, the positive is that Clean Energy just retired $50 million in debt at a 14.5% discount, and will also save around $4 million in interest payments on that debt over the next 18 months. But if the cost is another 10% dilution for shareholders -- which is what it would work out to based on selling enough shares at the current $3.25 per-share price to raise the cash -- I'm far from convinced that the discount in the debt makes up for the cost in shareholder equity.

Image source: Getty Images.

Clean Energy "saved" a total of $11.5 million in reduced interest expense and the discount it paid for the debt. Considering the importance of preserving cash, I understand the move from that perspective. But what I cannot wrap my head around is this: The company has more than a year before it really must deal with this debt, and if the business continues to grow and management continues to keep costs down, the cost to shareholdersin terms of dilution could be much lower.

Pretty much the only way the company comes out ahead is if the share price doesn't increase over the next 18 months, or doesn't actually start selling stock until the price moves higher.

So here's my concern in a nutshell: This latest expansion of the "at the market" program has me concerned that management isn't paying enough attention to per-share value creation.

I'm not giving up, but I'm watching closely

Clean Energy's management is in an unenviable position. The market has continually valued the company with oil price movements for several years now, and largely ignored the very real improvements in the company's operations, and its position in what is likely to be a very big industry in years ahead. At the same time, they have had little choice but to sell stock to improve the balance sheet and lower costs.

But at the same time, I don't want to see the company's leadership fall in love with the "easy" answer to raising cash in selling stock. Over the past two years the company has materially improved while shareholders have seen per-share value shrink. I'm not convinced that this latest debt retirement, when tied to the increase in dilution to come, is going to reverse that trend in the short-term.

I remain hopeful in the company's long-term prospects to generate strong per-share returns, but if management becomes addicted to fast-cash methods like selling more and more stock at very low prices, I'll be forced to reconsider.

10 stocks we like better than Clean Energy Fuels When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Clean Energy Fuels wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of January 4, 2017

Jason Hall owns shares of Clean Energy Fuels. Jason Hall has the following options: long January 2017 $5 calls on Clean Energy Fuels and long January 2017 $3 calls on Clean Energy Fuels. The Motley Fool owns shares of and recommends Clean Energy Fuels. The Motley Fool has a disclosure policy.