2 Top Stocks That Are Cash Cows

Image source: Getty Images.

Tech titans Oracle Corporation (NYSE: ORCL) and Cisco Systems, Inc. (NASDAQ: CSCO) are cheap on a price-to-earnings basis and they generate buckets of free cash flow (FCF). Their FCF generation combined is about as much asthe GDP of Uganda's38 million people. Even if all they did was grow earnings and FCF in line with inflation, they would be raging buys. But, of course, investing is rarely this simple, so let's take a look at what you need to know before deciding whether to buy these large-cap cash cows.

The value proposition

As you can see in the table below, both haveattractive FCF-to-enterprise value (market cap plus net debt) multiples. In plain English, this means that Cisco Systems is currently generating more than 10% of its market cap in FCF, while Oracle clocks in around 8%.However, as is often the case with cash cow stocks, revenue growth is low.

However, both have good return on invested capital (net income after tax divided by invested capital), a useful measure because an increasing ROIC suggests a company can increase FCF in the future even if revenue and earnings are flat. Declining ROIC is a warning sign.

| Company |

FCF/EV |

5-Year Average Revenue Growth |

Return on Invested Capital* |

FCF/Sales* |

|

Oracle |

8.1% |

0.8% |

10% | 33.6% |

|

Cisco |

10.7% | 2.7% | 11.3% | 25.3% |

Data source: Company accounts. Table by author. *Last 12 months.

In short, they are classic low-growth but cheap cash cow stocks. Is it time to buy? Not so fast -- these types of stocks can be value traps out to catch an unsuspecting investor. Let's look closer at them.

Oracle analysis

Both companies have threats/opportunities from the cloud, but Oracle is arguably better placed to address them. Oracle's challenge/opportunity in the next few years is to:

- Replace its declining hardware and on-premise software license sales with its fast-growing cloud revenues.

- Grow revenue while navigating the shift to cloud-based subscription sales, which forgo a large part of upfront revenue typically generated by on-license software sales.

Here is a breakout of Oracle's revenue growth for the first six months of its fiscal 2017, which ends in May. As you can see below, growth in cloud-based revenue (software, platform and infrastructure as a service) is currently offsetting declines elsewhere -- most notably in on-premise new software licenses.

| Sector |

Revenue Change |

Constant-Currency Growth |

Share of Revenue |

|

Cloud SaaS and PaaS |

$741 |

81% |

9% |

|

Cloud IaaS |

$21 | 9% | 2% |

|

On-premise new software licenses |

($452) | (15%) | 13% |

|

On-premise software license updates and product support |

$191 | 3% | 55% |

|

Hardware products |

($183) | (15%) | 6% |

|

Hardware support |

(57%) | (4%) | 6% |

|

Service revenue |

($72) | (3%) | 9% |

|

Total |

$189 | 2% | 100% |

Data source: Oracle Corporation presentations. Table by author. Data in millions of U.S. dollars.

There are two reasons to be optimistic. First, analysts are forecasting Oracle's revenue to grow 1.3% in 2017, with 3.3% expected for 2018.

Second, cloud-based subscription sales don't show the full picture, because they produce an annual recurring revenue of roughly a third of an up-font license sale. This is because subscription revenue is recognized over time, while sitting on the balance sheet as deferred revenue.

This means that reported revenue is not entirely reflective of underlying growth. Moreover, a look at short-term deferred revenue -- up8% in constant-currency terms in the second quarter -- confirms Oracle's underlying business growth is good.

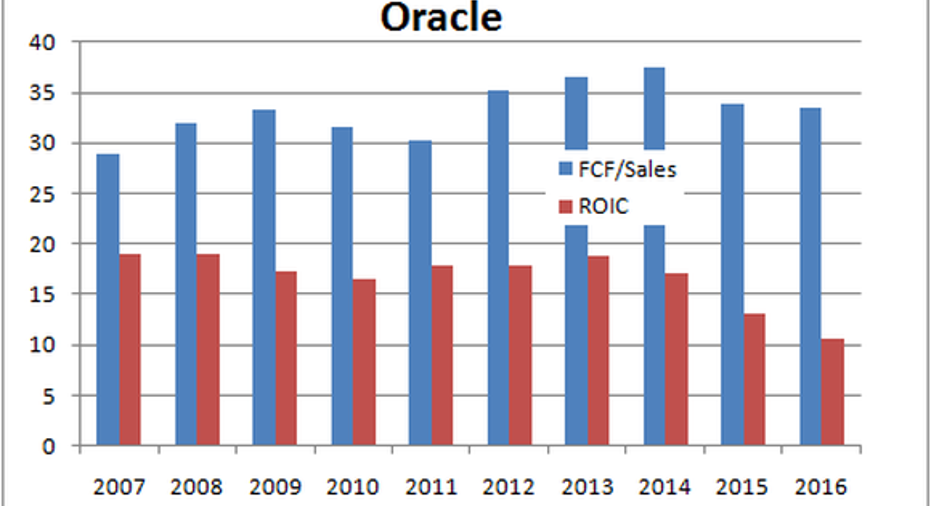

Finally, a quick look at FCF/sales suggests Oracle is holding up well during the transition, but declines in operating income in the last two years have hit ROIC. No matter, if EPS bounces back to 9% growth as expected in the year ending May 2018, the stock will start to look very cheap.

Data source: Oracle Corporation presentations. Chart by author.

Cisco analysis

While Oracle seems to be on track, the cloud appears to be creating more problems than opportunities for Cisco Systems. Increasing usage of network virtualization could mean companies run their network architecture in the cloud rather than in Cisco's sophisticated switches. Unfortunately, these switches tend to be expensive and good revenue generators for Cisco.

Similarly, if Cisco's routers and switches (which generate around 45% of its revenue) become commoditized, then less expensive options from competitors like Huawei or ZTE could threaten Cisco's market position. Indeed, a look at its quarterly switching and routing revenues shows that combined switching and routing revenue growth has been negative for the last four quarters.

NGN = next-generation network. Data source: Cisco Systems presentations. Chart by author.

Put simply, Cisco needs to stabilize its core switching and routing revenue while using its FCF to invest and grow its non-core operations. It's a different, and more difficult, problem than that faced by Oracle, and for that reason Cisco should trade at a discount to its tech peer.

Will Oracle Corporation stock fly high in 2017? Image source: Oracle Corporation website.

Which is the better buy?

Cisco is definitely a cash cow, but the risk to its core products remains, and if its products become commoditized then pricing, earnings, and cash flow could go into protracted decline. Oracle, on the other hand, looks to be on track with its transition toward the cloud, and for that reason looks like a more attractive investment.

10 stocks we like better than Oracle When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Oracle wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of Nov. 7, 2016

Lee Samaha has no position in any stocks mentioned. The Motley Fool owns shares of Oracle. The Motley Fool recommends Cisco Systems. The Motley Fool has a disclosure policy.