Mastercard's Recipe for Extra Juice

Most investors probably already know that Mastercard Inc.(NYSE: MA), the megacap credit card and payments network company, makes money every time a consumer swipes or otherwise uses one of their plastic rectangles to make a purchase. For every transaction Mastercard facilitates, the company earns a transaction processing fee and, depending on whether the purchase was made in the home country of the issuing bank, either a domestic assessment or cross border volume fee. Collectively, these revenue channels accounted for 85% of Mastercard's 2016 third-quarter revenue (before rebates and incentives are subtracted).

Image source: Mastercard.

What might surprise investors, however, is that it was not any of those revenue streams that were given credit as the "extra juice" Mastercard investors were seeing from the company's recent deals. Instead, that recognition was bestowed upon the lowly listed "other revenue" in the company's most recent quarterly investor presentation.

In the company's 2016 third-quarter conference call, Mastercard CFO Martina Hund-Mejean said:

What services make up Mastercard's "other revenue"?

Time and again during the conference call, Hund-Mejean and Mastercard CEO Ajay Banga called out Mastercard's services anonymously gathered under their "other revenue" umbrella, as one of Mastercard's growing competitive advantages. What mysterious services make up this seemingly anonymous business segment? And if it's such a small stream of revenue that it warrants barely more than a footnote on the quarterly presentation, why should Mastercard investors care so much about it?

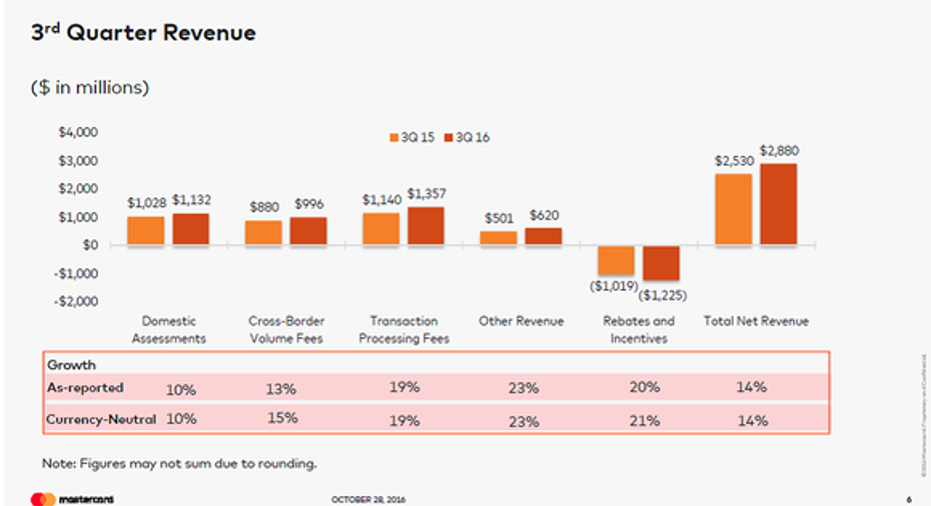

Image source: Mastercard Inc. 3Q16 Earnings Presentation.

Represented in Mastercard's "other revenue" accounting are a slew of services the company offers to its primary customers: their card-issuing banks and financial institutions. These services include fraud protection, consulting and research, loyalty and reward program management, and data analytics. These services can be extremely valuable to merchants and card issuers alike, as many of them fall far outside these institutions' core competencies.

These areas also require constant investment in technology and innovation, something that can quickly become expensive for card issuers like smaller credit unions and local banks. It is for this reason Banga said in the same conference call that these "types of competitive barriers are only as good as the investment you keep putting into them." Banga made it clear he believed Mastercard's "competitive edge" came from its constant allocation of capital and deliberate attention to these services for the past seven years.

The big takeaway for Mastercard investors

While the "other revenue" segment is the smallest of Mastercard's revenue streams, it should be noted it is also the segment showing the greatest growth. While domestic assessments, cross border volume fees, and transaction processing fees all grew by double digit percentage points year over year this past quarter, the "other revenue" line was the only segment that grew by more than 20%. This past quarter it accounted for $620 million in revenue. With those growth rates, it might not be long before it is on equal footing with Mastercard's other revenue streams.

Possibly even more important than this segment's incredible growth to Mastercard investors is the incredible value these services provide to the company's customers. When card issuing banks and merchants begin to rely on Mastercard to provide these essential services, it cultivates an incredibly sticky relationship. The stickier the relationship, of course, the harder it will be for a competitor to supplant Mastercard with that customer.

Ultimately, Mastercard investors have a lot to be pleased with this fast-growing, under-the-radar revenue stream that strengthens the company's bond with its clientele. This is exactly the type of new growth that can fuel an investment in Mastercard for years to come. Or, as Banga referred to these services in the conference call, "We're actually building yet another leg of a stool for our company for... decades to come."

Find out why Mastercard is one of the 10 best stocks to buy now

Motley Fool co-founders Tom and David Gardner have spent more than a decade beating the market. (In fact, the newsletter they run, Motley Fool Stock Advisor, has tripled the market!*)

Tom and David just revealed their ten top stock picks for investors to buy right now. Mastercard is on the list -- but there are nine others you may be overlooking.

Click here to get access to the full list!

*Stock Advisor returns as of November 7, 2016

Matthew Cochrane owns shares of Mastercard. The Motley Fool owns shares of and recommends Mastercard. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.