2 Risks Qualcomm Will Face After Acquiring NXP Semiconductors

Qualcomm (NASDAQ: QCOM) seems to have opened the door to automotive riches with its pending acquisition of NXP Semiconductors (NASDAQ: NXPI). NXP currently holds 14.5% share in the automotive semiconductor market, which is expected to be worth $36 billion by 2019, and Qualcomm is buying the lead in this fast-growing market with its pending $47 billion purchase of NXP.

However, Qualcomm's NXP acquisition does not ensure that the former will become the dominant player in the automotive semiconductor business, as it will face a stiff challenge from Infineon Technologies (NASDAQOTH: IFNNY). Additionally, Qualcomm might face integration and margin challenges once the merger is complete.

Why Infineon could pose a strong challenge

Infineon Technologies is the second-largest supplier of chips to the automotive industry with an estimated market share of 10.4% to NXP's 14.5%. This means that Infineon does not lag NXP by a huge margin. What's more, in 2015, Infineon led NXP in two of the three subsegments in the automotive semiconductor market.

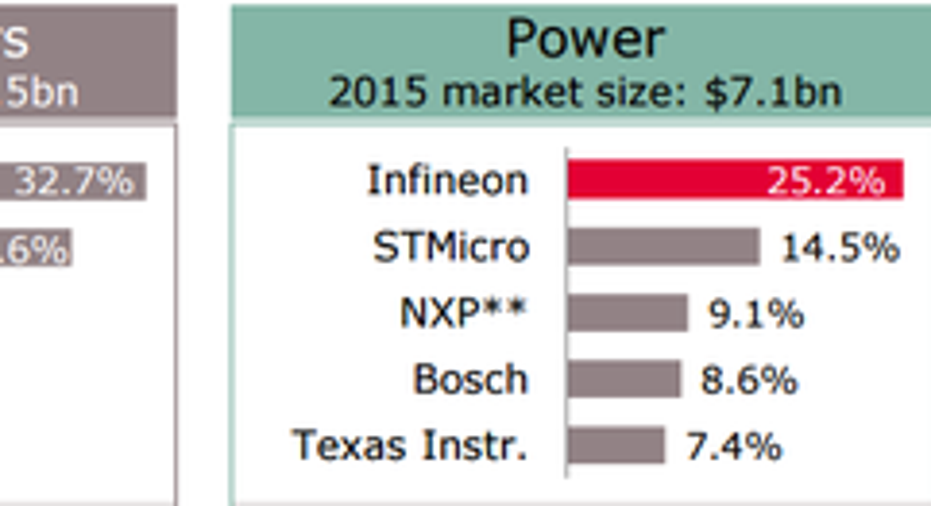

Image source: Infineon Technologies.

Infineon led NXP in the market for power and sensor chips in the automotive industry last year. These two markets were worth $11.3 billion. In comparison, NXP led Infineon by a huge margin in the microcontroller segment, which was alone worth $6.5 billion.

In the long run, Infineon can close the gap on NXP as it is the leading supplier of drivetrain solutions to electric vehicles. Infineon supplied its drivetrain solutions to seven of the top 10 electric vehicles in terms of sales last year. It counts the likes of Tesla Motors, BMW, Chevrolet, Volkswagen, and BYD Tang as its customers. This puts Infineon in a strong position in this market as it projects that sales of electric vehicles will grow from just 400,000 units in 2015 to 10 million units in 2025.

Along with pending growth in the number of electric vehicles -- which accounted for less than 1% of market share in 2015 -- the amount of semiconductor content is also expected to grow. Infineon forecasts that the semiconductor bill of materials in an EV will be as much as $705 per vehicle by 2025. In comparison, the chip content in each vehicle last year was $332, according to NXP.

EVs will carry higher chip content as compared to internal-combustion-engine-based vehicles because the electric drivetrain used in EVs contains a lot of electronics for power switching. The electronic systems in a hybrid drivetrain route power from the battery to the motor through an inverter, while no such electronic systems are needed in an internal-combustion engine.

According to McKinsey, the average hybrid drivetrain contains 10 times the semiconductor content as compared to an internal-combustion drivetrain. As a result, the demand for insulated-gate bipolar transistors, or IGBTs, will continue increasing as they play an important role in EV power systems.

Infineon enjoys a strong position in the IGBT market with a market share of 27.6%. In 2015, the IGBT market was worth $3.94 billion, according to Infineon, and some estimates put it at $6 billion in revenue by 2018.

So, Infineon could bridge the market share gap over NXP in the long run on the back of EV growth.

Integration challenges

Qualcomm's acquisition of NXP will have a negative margin impact on the former. This is because Qualcomm's gross margin profile is higher than that of NXP. For example, in the recently reported third quarter, NXP posted a non-GAAP gross margin of 50.5%. In comparison, Qualcomm's gross profit margin in the third quarter stood at 58%.

Thus, as Qualcomm begins to integrate NXP after the merger is complete in 2017, the gross margin might start deteriorating. The higher gross margin profile of Qualcomm is a result of its fabless manufacturing model as it outsources its chip manufacturing to foundries such as Samsung.

On the other hand, NXP has a foundry-based business model. It has 14 chip manufacturing facilities, along with seven packaging and testing facilities. However, these facilities can't manufacture chips for Qualcomm as they are "outdated," according to Market Realist. This reduces one potential synergy from the acquisition.

Despite this hiccup, the NXP acquisition is expected to deliver $500 million in annual cost synergies for Qualcomm within two years after the closure of the transaction. However, 65% of the savings will be on the operating expense side as Qualcomm will be able to use NXP's existing relationships to sell its automotive and Internet of Things products.

Qualcomm will also reduce its cost of goods sold as the combined companies can negotiate for lower raw material prices from suppliers. The reduction in the cost of goods sold will account for 35% of the cost-saving synergy from the acquisition. The reason the cost of goods sold synergies will be significantly lower than the operating expense reduction is because Qualcomm will not make much gains on the manufacturing side of the business due to the difference in the foundry business.

Also, given the legacy nature of the foundries, it is likely that NXP won't be getting Qualcomm's money to upgrade them. This is because Qualcomm has a different business model of outsourcing its manufacturing, and investing in NXP's foundries would lead to an increase in costs.

Although NXP will definitely add another dimension to Qualcomm's business, we've seen that it will also have a negative gross margin impact and pose integration issues. Additionally, the threat from Infineon cannot be ignored.

So even though Qualcomm is making a smart move by acquiring NXP Semiconductors, it is not guaranteed a smooth journey toward automotive riches.

10 stocks we like better than Qualcomm When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Qualcomm wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of Nov. 7, 2016

Harsh Chauhan has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Qualcomm and Tesla Motors. The Motley Fool recommends BMW and NXP Semiconductors. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.