3 Top Gold Stocks to Buy Now

With geopolitical tensions rising, now is the time when many investors are looking to spend some green to pick up some gold. From junior exploration companies to senior producers, the number of choices can be overwhelming for investors looking to gain exposure to the industry. So let's dig in and look at three top companies, Alamos Gold (NYSE: AGI), Barrick Gold (NYSE: ABX), and Goldcorp (NYSE: GG), where investors may be able to strike gold.

Ready player #1

At $2.2 billion, Alamos Gold -- a Canadian-based intermediate gold producer -- is the smallest company among the three discussed here by market cap, but that shouldn't preclude it from serious consideration. Coming off a great 2016, in which the stock doubled, Alamos seems poised to succeed even further in 2017.

In early April, the company announced that it had retired $315 million in senior debt, leaving the company debt free -- an especially advantageous position for a gold miner. According to management, this will save the company $24.4 million in annual interest payments.

Image source: Getty Images.

In fiscal 2017, management forecasts all-in sustaining costs (AISC) to equal $940 per gold ounce -- about 7% lower than the $975 it reported in fiscal 2016. Management also foresees a year-over-year rise -- about 6% -- in gold production, thanks to a ramp-up in production at its Young-Davidson mine in Ontario and higher mill production at the Mulatos mine in Mexico.

Alamos trades at 4.5 times trailing sales, which seems attractive compared to its five-year average price-to-sales ratio of 5.3, according to Morningstar. Its price tag seems even more enticing when you consider the stock trades at 16.1 times cash from operations on a trailing-12-month basis -- considerably lower than the 37 times cash from operations it was trading at less than a year ago in July.

Ready player #2

Turning to the other end of the market-cap spectrum, we find Barrick Gold, valued at $23.1 billion. Like Alamos, Barrick had a great 2016 -- rising more than 106% -- and is continuing its climb, rising more than 24% year to date. But what Alamos lacks in notoriety, Barrick makes up for in spades. And that name recognition has certainly grown recently as the company has announced a couple of major transactions.

For one, Barrick announced the $960 million sale of a 50% interest in Veladero -- one of its core mines -- to the China-based company, Shandong Gold Co., Ltd. And in another major deal -- this one closer to home -- Barrick announced a joint venture with Goldcorp to develop assets in Chile.

Reporting low all-in sustaining costs (AISC) of $730 per gold ounce in fiscal 2016, management expects modest gains, if any, in the current year -- it forecasts AISC between $720 and $770 per gold ounce. This shouldn't disappoint investors, however, as cash flow should still be strong.

In fiscal 2016, management achieved its goal of being able to generate free cash flow, even if the price of gold fell to $1,000 per ounce, and it forecasts the same achievement this year. Additionally, the company is on track to further execute its debt-reduction strategy.

The company aspires to reduce its debt by $5 billion through 2017 and 2018. On the company's fourth-quarter conference call, Kelvin Dushnisky, the company's president, reported that "Barrick wouldachieve this through a combination of cash flow fromoperations, potentially selling non-core assets and creating new joint ventures and partnerships." And the deals with Shandong and Goldcorp prove the company is executing its strategy effectively.

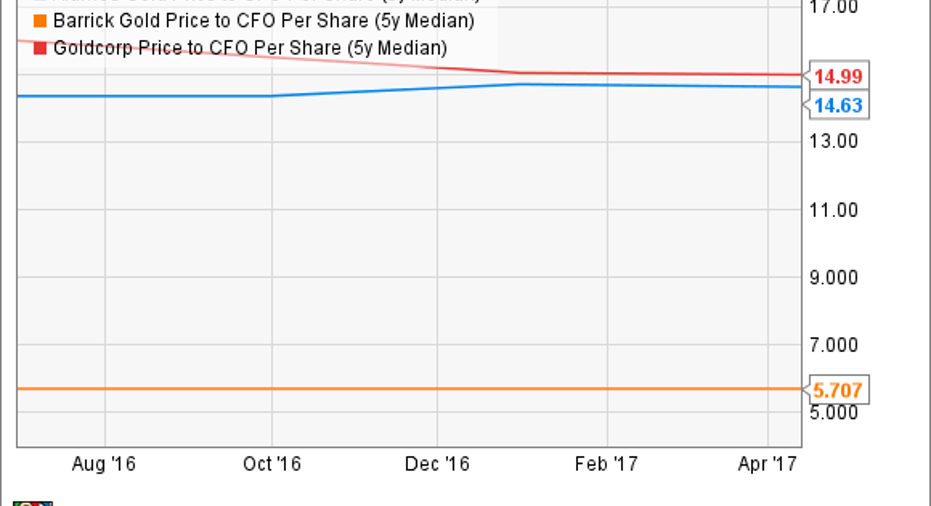

Trading at 2.7 times sales, which is higher than its five-year average of 1.8 according to Morningstar, Barrick may seem expensive, but we're looking to buy top gold stocks and hold them for the long term. The stock may seem richly priced now, but the company's long-term potential certainly supersedes this. And it's not as if the company is unreasonably valued.

NEM EV to EBITDA (TTM) data by YCharts.

In fact, it's arguably a bargain. The company has an EV (enterprise value)/EBITDA (earnings before interest, taxes, depreciation, and amortization) ratio well below its closest competitor, Newmont Mining Corp.

Ready player #3

Lastly, in-between Alamos and Barrick by market cap, we have Goldcorp. Climbing more than 13% year to date, Goldcorp has fared well this year, but it certainly has the potential to rise even higher. In executing its five-year strategy to grow net asset value per share, Goldcorp has demonstrated a long-term perspective that will benefit shareholders -- something we love to see.

For one, the company aspires to grow its gold production about 20% from the 2.5 million ounces it forecasts in fiscal 2017 to more than 3 million in 2021. In addition to ramp-ups in production at the Eleonore and Cerro Negro mines, Goldcorp is counting on increased grade and the completion of the Pyrite Leach Project at Penasquito to affect the five-year increase in production.

In terms of a farther peek into the future, we find that the aforementioned joint venture in Chile with Barrick represents a significant opportunity for the company to continuously increase its production. Additionally, Goldcorp seeks to increase its gold reserves by 20% and reduce AISC by 20% over the next five years, ensuring the company has a lustrous future.

Goldcorp, with a sales multiple of 3.7, seems reasonably valued compared to its five-year average of 4.6. On the other hand, the stock may seem pricey compared to the other companies in this group.

AGI Price to CFO Per Share (five-year Median) data by YCharts.

Valuing a stock, however, is far from black and white. And Goldcorp's long-term prospects suggest that paying a higher price today may well pay off tomorrow.

Investor takeaway

Alamos, Barrick, and Goldcorp all offer compelling arguments for investment, but those looking for lower-risk opportunities would be better served by focusing on Barrick and Goldcorp. Regardless of which company investors choose, all three provide clear benchmarks that can be monitored to ensure that their long-term successes remain on track.

10 stocks we like better than GoldcorpWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Goldcorp wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of April 3, 2017

Scott Levine has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.