The Hidden Cost of Bank of Americas Deposits

Bank of America's headquarters in Charlotte, North Carolina. Image source: iStock/Thinkstock.

When it comes to competitive advantages, Bank of America (NYSE: BAC) has a huge one. As of the third quarter of this year, it had $439 billion worth of seemingly free money that it can (and does) invest in interest-earning assets -- principally, loans and government bonds.

What is this free money, you ask? It's what Bank of America's customers have stashed away in checking and other types of non-interest-bearing accounts. However, even though these deposits don't carry a direct cost, there is an indirect cost associated with gathering them up.

Other peoples' money

Bank of America isn't the only bank that has access to these types of funds. Every one of its competitors does too. But what distinguishes Bank of America in this regard is that it has more noninterest-bearing deposits than any other bank in the United States.

Data source: Quarterly financial filings. Chart by author.

This advantage traces back to Bank of America's origin. It was founded at the beginning of the twentieth century to serve individual consumers, who had largely been ignored up until that point by the nation's other leading banks, which focused on commercial customers.

Fast forward to today and this is the reason Bank of America is primed to earn so much more money than other banks when interest rates rise. When this happens, which could be any day now, the North Carolina-based bank will be able to charge higher rates for its loans, while the cost of its massive hoard of interest-bearing deposits will stay the same, at zero.

Bank of America CEO Brian Moynihan addressed this very point at the 2016 Goldman Sachs U.S. Financial Services Conference last week:

This is great for Bank of America's shareholders, as there's every reason to believe at this point that interest rates will soon rise.

Free money isn't necessarily free

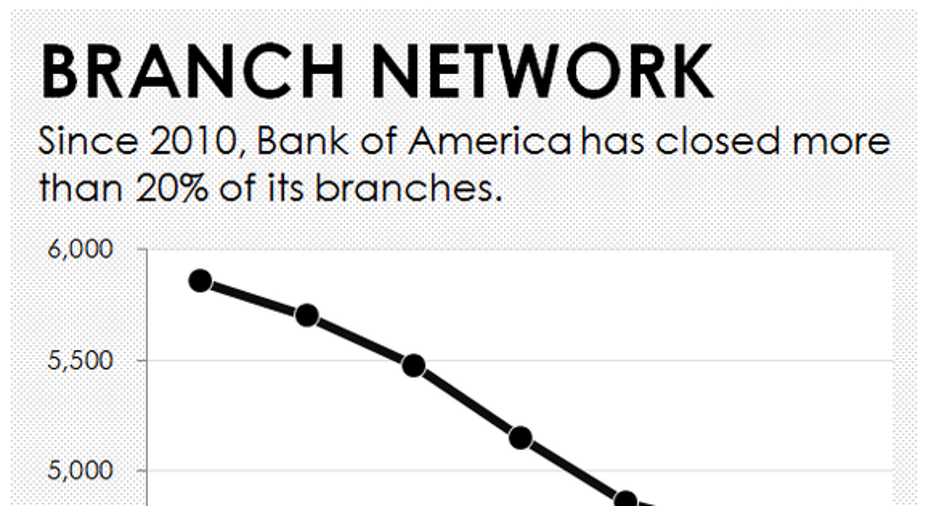

Yet, as Moynihan addressed earlier in his presentation, it's a little misleading to assume that even non-interest-bearing deposits are in fact entirely free. This is because Bank of America has to operate an enormous branch network to attract the funds.

Bank of America has just over 4,600 branches. That's down from the roughly 6,000 that it had when Moynihan took over in 2010, but it's still a lot of real estate that has to be manned by employees. When you factor this into the equation, there's a clear cost associated with what otherwise seems to be free money.

Data source: Bank of America. Chart by author.

If you spread the cost of Bank of America's consumer bank over its deposit base, it comes out on an annualized basis to about 1.6% of its total deposits. Consequently, even its free deposits aren't exactly free.

The fact nevertheless remains that Bank of America will still benefit more from higher rates than its peers, who bear similar operating costs to attract deposits. This is because, as rates rise, Bank of America's operating costs should stay the same. Thus it'll earn more money without having to spend more to do so.

It's for this reason that most of the added revenue from higher interest rates will, according to Moynihan, "fall to the bottom line."

10 stocks we like better than Bank of America When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Bank of America wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of Nov. 7, 2016

John Maxfield owns shares of Bank of America and Goldman Sachs. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.