How Much Will I Get From Social Security If I Make $50,000?

Most people rely heavily on Social Security for their retirement income, including those who earn roughly the median income for American households. If you earn $50,000 a year, you're doing better on an individual basis than many of your fellow Americans. You probably don't have a lot of money after paying your costs of living to save toward retirement, but you can save at least some money to help supplement your Social Security -- and then make it work as hard as it can by investing well. In pursuing that goal, it's helpful to know how much you can count on Social Security to provide the income you'll need. Below, we'll take a look at how much someone earning $50,000 per year can expect from Social Security.

Image source: Getty Images.

What you'll pay in payroll taxes toward Social Security

Workers who earn $50,000 per year have payroll taxes withheld from their entire paychecks, because the wage base limit on Social Security is more than double their earnings. You'll therefore pay 6.2% of your salary, or $3,100, toward Social Security. Your employer will pay an equal amount directly on your behalf to Social Security.

You'll also get credit for the full $50,000 amount in determining your benefits because all of that income was subject to payroll taxes. The key exception is if you have a job with a local or state government agency that doesn't participate in Social Security, choosing instead to offer its own independent pension.

Looking at your whole career

The calculation for determining Social Security benefits doesn't just look at a single year. Rather, the formula that the Social Security Administration uses takes your entire career into account, determining your average monthly earnings from the 35 highest-earning years in your career after applying an inflation adjustment to early years to make them comparable.

What that means is that how you got to $50,000 matters in determining your benefits. If you've had relatively flat earnings throughout your career, your benefits will be higher than if you had very low earnings early in your career and then got major raises to climb up to the $50,000 level. That's in stark contrast to some pension programs, where even a single year of high earnings can boost your pension benefits substantially.

What you'll get from Social Security

To come up with a number, let's take a hypothetical case. Specifically, we'll consider a situation in which a worker earned the inflation-adjusted equivalent of $50,000 for their 35 highest earning years, turning 62 in 2017. That makes the work a lot simpler and provides a baseline against which you can consider your own particular situation.

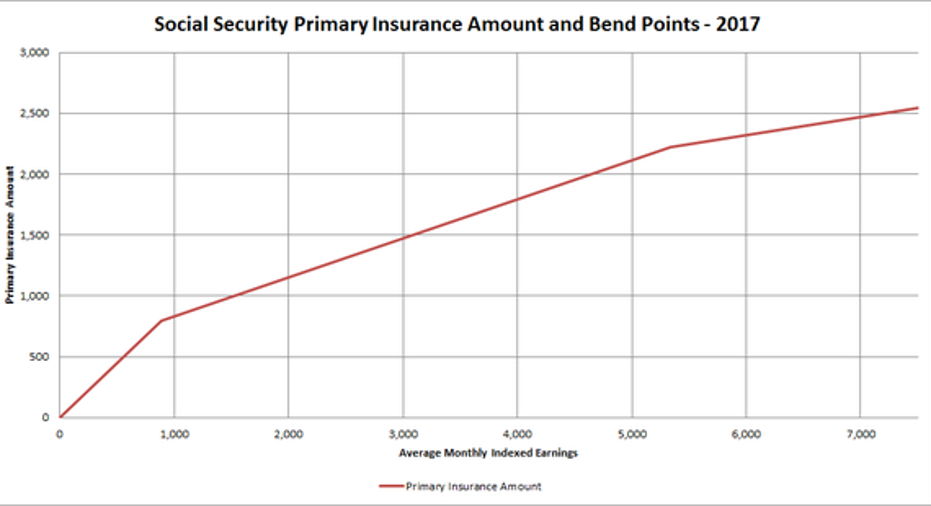

Your average indexed monthly earnings under these assumptions will be $4,167 per month. To use the SSA's benefit formula for someone becoming eligible for Social Security in 2017, you take 90% of the first $885 in monthly earnings, and then 32% of earnings between $885 and $5,336. Earnings above that level produce a 15% bump in the resulting number, which the SSA refers to as the primary insurance amount. However, for an average of $4,167, we don't need to use that second bend point. Instead, 90% of $885 is $796.50, and 32% of the remaining $4,144 is $1,050.24. That adds up to $1,846.74 as a monthly benefit if you wait until full retirement age to retire, which for you will be 66 years and two months.

Graph by author. Data source: SSA.

Another way of thinking about it is in terms of how much of your previous income Social Security will replace. In this case, your benefits will pay you about 44% of your previous salary. That's a higher percentage than for those who earn more, but a lower one than for those who earn less.

If you don't retire at your full retirement age, then your benefits will differ. For example, if you claim benefits right away at age 62, you'll receive 25.8% less, or about $1,370 per month. By contrast, if you wait until you turn 70, you'll receive 30.7% more, adding up to about $2,414 in monthly benefits.

Finally, let's consider a situation in which you work for only half of a 35-year career. You might think your benefits would simply be half of what someone who worked throughout that period got, but Social Security has a progressive benefits system that leads to a higher replacement income for lower-income workers. For instance, if you worked just half of the 35-year history of the example above, your average earnings would be $2,083 rather than $4,167. Put that number in the formula, and it spits out $1,179.86. That's almost two-thirds of the full-career Social Security benefit, even though your total payroll taxes withheld was just half of what a full-time worker over 35 years made.

Know your Social Security benefits

Social Security will play a key role for those earning $50,000 a year. However, with monthly payments that replace less than half of your pre-retirement earnings, you'll still need to save in order to be financially secure when you retire.

The $15,834 Social Security bonus most retirees completely overlook If you're like most Americans, you're a few years (or more) behind on your retirement savings. But a handful of little-known "Social Security secrets" could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $15,834 more... each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we're all after.Simply click here to discover how to learn more about these strategies..

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.