The Most Depressing Social Security Statistic You'll Ever See

Image source: Getty Images.

It's pretty fair to say that Social Security is America's most important social program. It's possible that Medicare could eventually surpass Social Security in average lifetime benefits if medical care inflation keeps outpacing wage and benefit growth rates, but for the time being, the monthly income provided to retired workers by Social Security is far more important.

According to the most recent poll on Social Security from national pollster Gallup, 59% of currently retired seniors count on Social Security as a "major" source of their income, unchanged from the April 2015 poll. Those who count on Social Security as a "minor" source of income dropped slightly to 28% from 31% in the prior year. Still, that's nearly nine in 10 seniors who likely need Social Security income to make ends meet during retirement. Among pre-retirees, nearly eight in 10 believe Social Security income will account for a major or minor source of their retirement income.

These statistics make it plainly evident that the longevity of the Social Security program should be among lawmakers' top priority. Unfortunately, that's not been the case.

Social Security is coming to a crossroads

Based on the latest report from the Social Security Board of Trustees, the program is expected to flip from a cash inflow to a cash outflow -- largely caused by the ongoing retirement of baby boomers and people living longer than ever -- by the year 2020. Once 2034 rolls around, the Trustees predict all $2.8 trillion-plus in spare cash will have been exhausted. If the program's excess cash is depleted, the report predicts that benefits would need to be cut across the board by 21% in order to sustain benefits through the year 2090. Not exactly a promising scenario for current or future retirees.

Image source: Pixabay.

But there's an even bigger and more immediate problem for Social Security: a lack of adequate inflationary increases in benefits for current retirees.

Social Security's benefits are examined annually by the Social Security Administration using the Consumer Price Index for Urban Wage Earners and Clerical Workers, or CPI-W. The average reading from the third quarter in the previous year serves as the baseline, while the average reading in the third quarter of the current year serves as the comparison. If the CPI-W increases year over year, then seniors get a raise that's commensurate with the percentage increase, rounded to the nearest tenth, from one year to the next. If the price of goods and services measured by the CPI-W declines, then benefits remain flat. Over the past eight years, there have been three such instances where the cost-of-living adjustment (COLA) has been 0% as a result of a year-over-year decline in the CPI-W.

The latest COLA, which was released four weeks ago by the SSA, called for the smallest increase on record: just 0.3%. Weaker energy prices and stagnant food costs weighed on the CPI-W, leading the SSA to announce an increase that'll put only $4.05 extra in the average retired worker's monthly benefit check.

The most depressing Social Security statistic you'll ever see

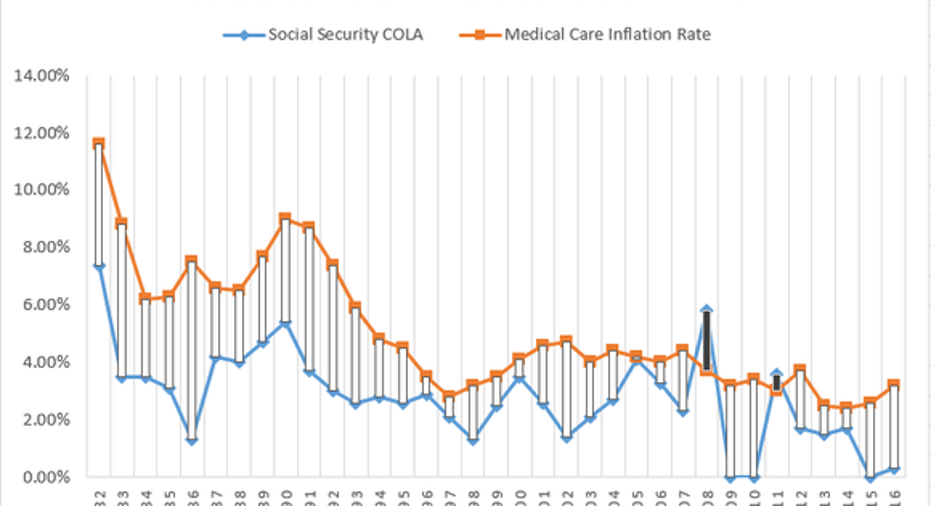

The bigger problem is that the inflation seniors are facing from housing, and especially medical care, is growing at a much faster clip than 0.3%. In fact, medical care inflation has been outpacing Social Security's COLAs for an exceptionally long period of time. In what could easily be described as the most depressing Social Security statistic you'll ever see, medical care inflation has been higher than Social Security's COLA in 33 of the past 35 years.

Here's what that difference looks like on a comparative basis:

Chart by author. Data source: Social Security Administration, Bureau of Labor Statistics. 2016 medical care inflation rate based on first-half BLS estimate.

But, even more telling, here's the difference on a monetary basis (assuming both began at $100) since 1982:

Chart by author. Data source: Social Security Administration, Bureau of Labor Statistics. 2016 medical care inflation rate based on first-half BLS estimate.Based on beginning value of $100.

No, your eyes aren't deceiving you. Based on Social Security's COLA, a $100 benefit in 1981 is now worth nearly $260. However, what $100 bought you in medical care in 1981 has increased to almost $556, or a 456% increase. That's more than double Social Security's COLA over the past 35 years. That's pretty depressing, and it's a clear reason why seniors could be struggling to make ends meet.

The move to make right now

One idea that's been floated around to resolve this vast difference in inflation between Social Security benefits and medical care is to abandon the CPI-W in favor of the CPI-E, or Consumer Price Index for the Elderly. The CPI-E only factors in the spending habits of households with persons aged 62 and up, meaning it would presumably offer a better read on the expenditures that matter most to seniors. In particular, the CPI-E puts much more emphasis on housing and medical care costs relative to the CPI-W, whereas the CPI-W emphasizes education, apparel, entertainment, and food expenses more than the CPI-E.

However, this proposal is unlikely to gain much traction, at least in the near term, because the CPI-W takes millions of additional households into account in its calculations, and is thus still viewed as the better measure of inflation.

Instead of hoping that Congress will adjust how Social Security's COLA is factored annually, current retirees and pre-retirees need to ensure they're working with a detailed monthly budget. Cutting your spending isn't ideal by any means, but having a good understanding of your cash flow can go a long way toward extending your monthly benefit.

Image source: Getty Images.

Here's the good news: Budgeting tools can be found almost entirely online these days, and many are free. In fact, some software can help you set up a monthly savings plan to ensure you stay on track.

Probably the hardest part of budgeting is ensuring you stick to your plan. The easiest way to do that is to surround yourself with people who share your ideals to stick to a budget. This means everyone in your households sticks to the budget. If you live alone, then meeting up with like-minded people once or twice a month to discuss your financial progress could be a smart move. Separating your money into different accounts for entertainment, food, and so on can also help if you have a hard time resisting the urge to spend.

Long story short, it doesn't look as if the gap between Social Security's COLAs and medical care inflation is going to abate anytime soon, which means seniors and pre-retirees need to be prepared to function on an increasingly tighter budget where their dollar may not stretch nearly as far as in years past.

The $15,834 Social Security bonus most retirees completely overlook If you're like most Americans, you're a few years (or more) behind on your retirement savings. But a handful of little-known "Social Security secrets" could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $15,834 more... each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we're all after.Simply click here to discover how to learn more about these strategies.

Sean Williamshas no material interest in any companies mentioned in this article. You can follow him on CAPS under the screen nameTMFUltraLong, and check him out on Twitter, where he goes by the handle@TMFUltraLong.

The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter servicesfree for 30 days. We Fools may not all hold the same opinions, but we all believe thatconsidering a diverse range of insightsmakes us better investors. The Motley Fool has adisclosure policy.