Check Point Software Technologies Ltd. Earnings Top Company Guidance

Following Fortinet's (NASDAQ: FTNT) pre-announcement on Oct. 11 that it would miss management's revenue forecast, investors in Check Point Software Technologies Ltd. (NASDAQ: CHKP) had a right to fear the worst from their company's third-quarter earnings, which were reported Oct. 31. In the end, Check Point's revenue came in at the top end of guidance and earnings per share were ahead of the estimate, with CEO Gil Shwed claiming he hadn't seen any of the kind of lengthening in the sales cycle that Fortinet's management spoke of.

Let's take a look at the earnings report.

Check Point Software Technologies results: The raw numbers

Starting with the headline numbers from the third quarter:

- Total revenue increased 6% to $428 million, compared to the forecast range of $405 million to $435 million.

- Non-GAAP operating income increased 1.1% to $230.6 million.

- Non-GAAP earnings per share increased 9% to $1.13, compared to the forecast range of $1.03 to $1.10.

Details behind the numbers

The headline numbers were good, but on an underlying basis revenue was even better. I have three points regarding the numbers, but first, here is a chart of revenue share so you can see the relative importance of each revenue stream:

Data source: Check Point Software Technologies investor presentation.

Underlying revenue

As with many companies growing software subscriptions (in this case Check Point's "software blades"), there is a short-term hit to revenue growth. In Check Point's case this is because the price of the software blade is separated from the appliance product and then recognized on the balance sheet as deferred revenue over time. CFO Tal Payne disclosed that the net effect on revenue was $6 million to $8 million; in other words, revenue growth was arguably closer to 7.6% in the quarter.

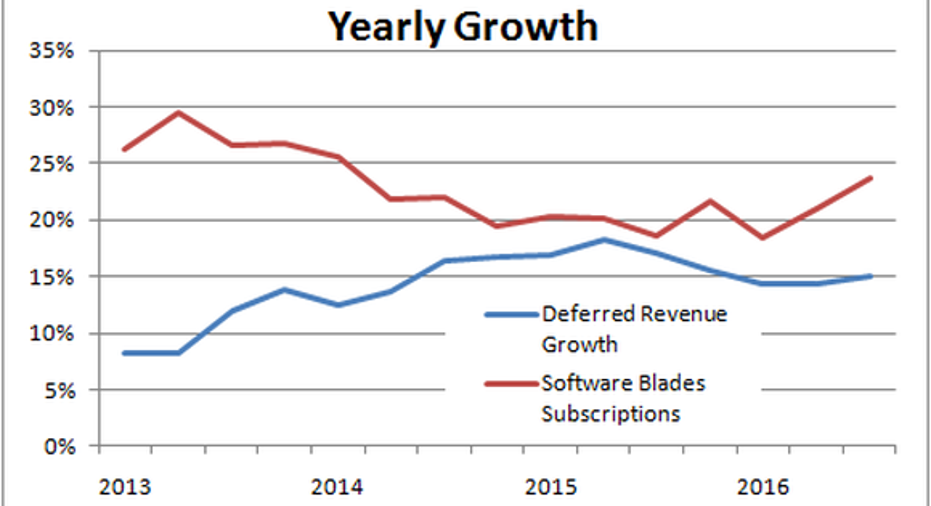

As you can see below, deferred revenue growth continues at a very strong clip, as does software-blade revenue. For reference, software-blade subscriptions made up 23.1% of revenue compared to 19.7% in the same period last year.

Data source: Check Point Software Technologies investor presentation.

Products and licenses growth

It's important to recognize the importance of the shift to deferred revenue, because on a superficial basis revenue growth is slowing. In addition, as you can see below, revenue growth in products and licenses -- the key to future software updates and maintenance growth -- appears to be slowing. However, recall that as Check Point increases the software blades bundled with product appliances, it becomes less important to purely look at products and licenses sales growth.

That said, overall revenue growth has clearly been slowing in recent quarters:

Data source: Check Point Software Technologies investor presentation.

Earnings growth?

Third, revenue growth came in at 6%, but non-GAAP operating income increased just 1.1%. Why?

The answer lies in the margin compression caused largely by management increasing sales and marketing expenses in order to drive revenue growth. Check Point needs to do this in order to maintain its leadership position in the marketplace, and continue to grow its installed base.

Data source: Check Point Software Technologies investor presentation. LHS = left-hand scale. RHS = right-hand scale.

Wondering how 1.1% operating-income growth led down into 9% non-GAAP EPS growth? The answer is a reduced share count created by share buybacks.

Looking ahead

Check Point's management affirmed it hadn't seen any of the "moderated spending environment, extended sales cycles and sales execution challenges" spoken about by Fortinet's CEO Ken Xie during that company's earnings call. That suggests that Fortinet's troubles may well be company-specific. On the other hand, Check Point is aggressively increasing sales and marketing efforts -- at the cost of margin -- and revenue growth is expected. However, Check Point's underlying revenue growth is good, and the growth in deferred revenue should lead to plenty of revenue and cash flow in future.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Lee Samaha has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Check Point Software Technologies. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.