3 Questions Williams Companies Inc Investors Want Answered Next Week

Images source: Getty Images.

Given how volatile commodity prices and Williams Companies' (NYSE: WMB) stock have been over the past year, one would think that Williams' financial results have been just as volatile. However, that simply isn't the case. As the chart below shows, its underlying results, measured by the performance of its MLP Williams Partners (NYSE: WPZ), have been quite good:

Data source: Williams Partners. Chart by author. Figures in millions.

Instead, one of the driving forces behind the volatility is the uncertainty surrounding Williams' future. Because of that, the company needs to resolve some questions investors have, which it can do when reporting third-quarter results on Monday. Here are three questions investors would like it to answer in that report.

1. Did Williams Partners' growth projects deliver as expected?

Expansion projects have been the primary driver of Williams Partners' growth over the past year. For example, earnings in its Atlantic-Gulf segment are up 6% year over year due in part to increased fee-based revenue from expansion projects on the Transco system. Likewise, its central segment benefited from fee-based growth projects going into service.

Three more projects were expected to come online during the third quarter to drive results. These included the Transco-Rock Springs facilities that it placed into service at the beginning of August, the Gunflint tieback that started delivering oil in mid-July, and the Kodiak tieback that was expected to be in full production during the quarter. Investors want to see that these three projects delivered as promised during the quarter by driving atangible improvement in segment earnings.

2. Does it have any update on the Geismar monetization?

During the quarter Williams Partners announced that it had initiated a process to monetize its interest in the Geismar olefins plant. The MLP said that it was considering either a sale of its interest in the asset or a fee-for-service tolling agreement. Either option would help bring more security to Williams' financial situation. A sale would bring in cash that it can use to repay debt and fund capex, while a fee-based agreement would stabilize that asset's cash flow.

What investors want to see this quarter is where the company is in that process. If nothing else, they want to know if the company is leaning one way or the other regarding how it plans to monetize the facility.

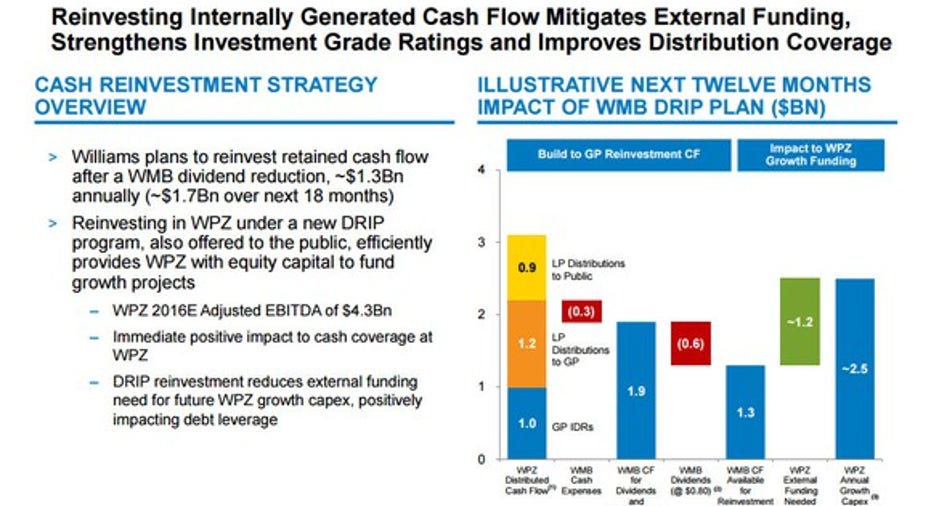

3. How is it planning to fund its capex gap?

The reason an update on Geismar is important is that Williams Partners has a gap between its current financial resources and anticipated growth spending over the next two years:

Image source: Williams Partners investor presentation.

As that chart notes, Williams Companies is helping it bridge the gap by reducing its dividend and reinvesting that cash flow to support its MLP's growth capital needs. That said, there's still a wide gap that it needs to cover. What investors would like to know is how it intends to plug that hole. While the company said that its options include asset sales (such as Geismar), equity issuances, and public debt issuances, investors want more details, especially considering Williams' increased cost of capital due to its slumping unit price and credit metrics.

One other thing investors want to see is how many of their fellow unitholders are participating in the company's new distribution reinvestment plan (DRIP). If a significant portion of unitholders joined Williams Companies in the DRIP program, it would considerably reduce the company's need for outside funding.

Investor takeaway

The expectation is that Williams Companies will deliver another relatively solid quarter because nearly all of its income comes from the growing supply of fee-based revenue from its MLP. That said, the company still has a couple of issues to work out, including the plans for its Geismar plant and how it intends to fund the major expansion projects currently in the pipeline. If Williams can address these questions by showing tangible progress on sourcing solutions, then it would give investors more confidence that the franchise is on solid ground.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Matt DiLallo has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.