Sunoco LP in 4 Charts

Image source: Getty Images.

Sunoco LP (NYSE: SUN) is unique in the gasoline distribution segment. Because it chose to organize as a master limited partnership, it pays its unitholders pretty generous distributions, with a current yield at more than 10%. But before jumping on board with that eye-catching yield, there are a few things investors need to know about the company.

Sunoco's complex ownership structure makes one owner a big winner

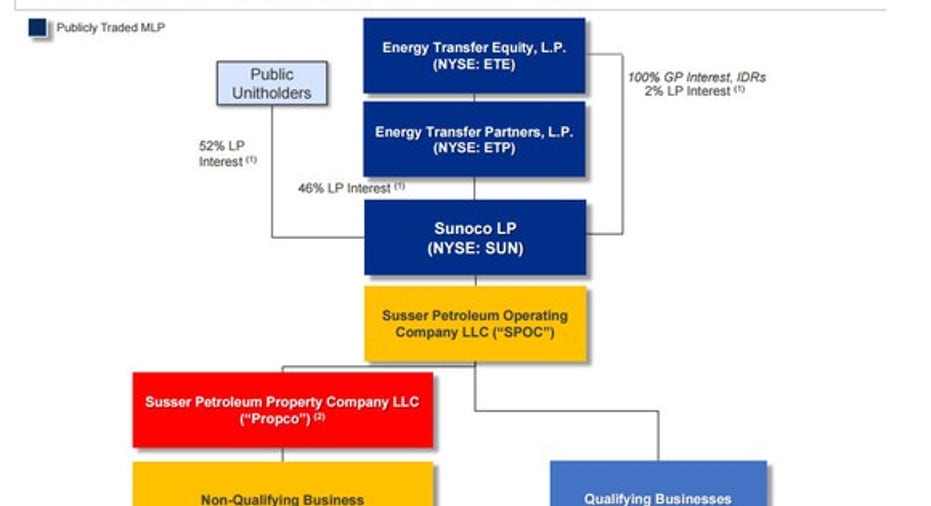

One of the first things investors need to understand about Sunoco is that it has what appears to be a complex organizational structure at first glance. As the chart below shows, it has three owners:

Data source: Sunoco LP.

On this chart, you see that Energy Transfer Equity (NYSE: ETE) is the company's primary parent because it owns both Sunoco's general partner and incentive distribution rights (IDRs). This gives Energy Transfer Equity a significant portion of the company's quarterly cash flow compared to public unitholders and Energy Transfer Partners (NYSE: ETP), which own similarly sized portionsof Sunoco's outstanding units:

Data source: Sunoco LP and Energy Transfer Equity. Chart by author.

As this chart shows, despite the fact that Energy Transfer Equity only owns 2% of Sunoco LP's outstanding units, it received 22% of last quarter's cash distributions because the IDRs give it an increasing share of the company's distributable cash flow.

Its earnings are resilient but not stable

While most MLPs own fee-based assets like pipelines and processing plants, Sunoco LP owns gas stations and fuel distribution businesses. These assets provide relatively steady income. However, commodity prices and economic drivers can impact cash flow. Because of that, its margins can fluctuate:

Data source: Sunoco LP investor presentation.

Those fluctuations in margin can be problematic for a company that pays out most of its income to unitholders each quarter. For example, last quarter distributable cash flow was $92.2 million, which was down from $111.5 million in the prior quarter. As a result of that decline, Sunoco LP's distribution coverage ratio was 0.92 times, meaning it paid out more than it brought in. That is a concern because if the coverage ratio continues to remain below 1.0 times in the future, it could cause the company to cut its lucrative distribution. The market seems to think that is what will happen, which is why the distribution yield has risen to more than 10% this year.

Sunoco LP has plenty of room to grow

One way Sunoco LP can avoid reducing its payout is by delivering meaningful growth in distributable cash flow via organic growth and acquisitions. That is exactly what it intends to do, investing roughly $400 million this year in building up to 35 new gas stations.

Meanwhile, it continues to make acquisitions in both the retail and wholesale distribution segment. Last quarter, for example, the company agreed to purchase the fuels business of Emerge Energy Services (NYSE: EMES) for $178.5 million. The Emerge Energy Services' deal diversified the company by addingtransmix operations and other midstream assets to the mix, providing additional platforms for future growth. In addition to that, Sunoco agreed to buy the convenience store, wholesale motor fuel distribution, and commercial fuels distribution businesses from Denny Oil Company. That deal continued the company's roll-up strategy, whereby it has acquired more than $500 million of third-party retail and wholesale fuel distribution assets since Dec. 2014. It has plenty of additional roll-up opportunities given the fragmentation in the industry as the chart on the slide below shows:

Data source: Sunoco LP Investor presentation.

Investor takeaway

Sunoco LP is not like the typical MLP. It does not own fee-based pipeline and processing assets that deliver relatively stable cash flow to support distributions. Instead, it owns convenience stores and fuel distribution assets, which are more sensitive to economic conditions and commodity prices. Because of that, the company's payout is not as secure as other MLPs. Furthermore, the company's complex ownership structure means that a large percentage of its cash flow goes to Energy Transfer Equity instead of regular unitholders. For many income investors, these critical differences mean that Sunoco LP might notbe the best MLP to own if steady income is the goal.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Matt DiLallo has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.