Is Ingersoll-Rand Plc Still a Good Value?

It's been a pretty good year so far for companies with significant exposure to heating, ventilation, and air conditioning (HVAC) markets. Ingersoll-Rand Plc(NYSE: IR)has risen 20%, pure play Lennox International, Inc (NYSE: LII) is up nearly 26%, andJohnson Controls (NYSE: JCI) (which also has substantive automotive operations, and is busy integrating Tyco International this year) is up 35%.

With the smallest stock price increase of the three, is Ingersoll-Rand still a good value for investors?

Ingersoll-Rand's unusual year

At the start of fiscal year 2016, management predicted continuing adjusted EPS of $3.80 to $4. Fast-forward to the second-quarter results in July, and guidance increased to $4-$4.10, while the stock is up more than 20% year to date. In addition, adjusted free cash flow guidance increased to a range of $1 billion-$1.1 billion from $950 million-$1 billion previously.

It's good news, but it's really a tale of two segments moving in opposite directions. To explain, let's first look at how the company makes money. As you can see below, Ingersoll-Rand generates 77% of its revenue from its climate segment, with the rest bundled together in its industrial segment. Two-thirds of total revenue came from North America in 2015, and 68% of revenue was from new equipment. That's important, as it means the company's revenue tends to fluctuate significantly with end demand.

Data source: Ingersoll-Rand presentations.

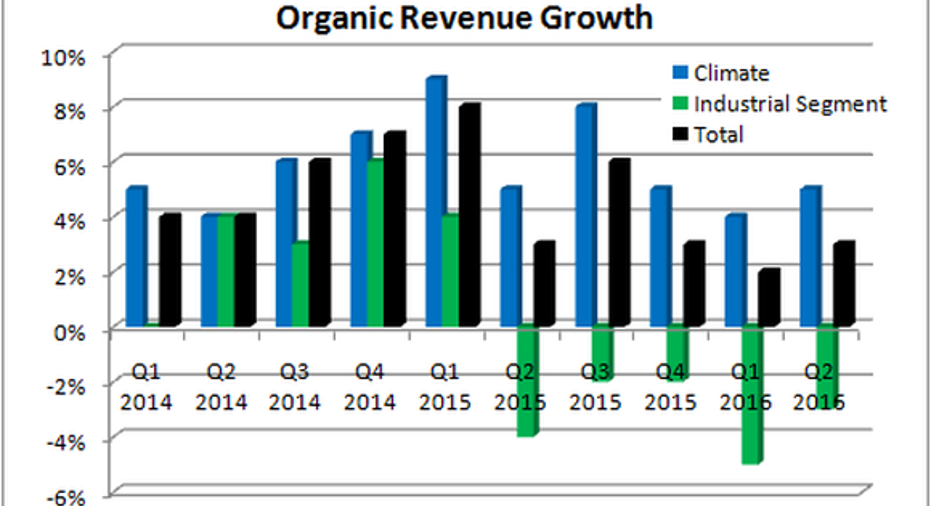

Climate good, Industrial bad

Simply put, Ingersoll-Rand's climate segment has outperformed the expectations set at the start of the fiscal year, while the industrial segment has fallen short. Here's a quick look at how organic revenue growth has diverged in the two segments.

Data source: Ingersoll-Rand presentations.

Ingersoll-Rand has an opportunity to expand operating margin with its Trane brand (air conditioning systems), and management has delivered so far this year. Having started the year expecting 3% to 5% organic revenue growth and operating margin of 13.25% to 13.75%, the climate segment is now forecast to hit 4% to 5% organic revenue growth with a 14% to 14.5% operating margin.

It's a similar story with Johnson Controls' building efficiency (primarily HVAC) segment. Organic sales increased 4% in its most recent third quarter, with North America up 3%. Meanwhile, Lennox International expects North American residential HVAC shipments to increase by the mid single digits in 2016, with commercial shipments forecast to increase in the low single digits.

However, it's a different story with Ingersoll-Rand's industrial segment. Organic revenue is now expected to decline 5% to 4%, compared to original expectations for a decline of 1% to growth of 1%. It's even worse with operating margin, which is now expected to be 10% to 11%, compared to initial guidance of 13% to 13.75%.

Data source: Ingersoll-Rand presentations. Figures in basis points, where 100 basis points equals 1%.

According to CFO Susan Carter on the most recent earnings call, utility vehicles make up around 20% of industrial sales, with aftermarket sales overall in the segment contributing 30%. This means around 50% of industrial sales go to new equipment in the industrial process industry, including compression technologies used in the energy industry. No prizes for guessing that sales have been hard-hit this year as energy companies continue to cut capital spending.

Looking ahead

There are three key reasons Ingersoll-Rand stock might increase in value in the future:

- Ongoing margin could expand in the climate segment, expanding profits in future years.

- Energy capital spending could increase with higher energy prices, with which Ingersoll-Rand's compression equipment is highly linked.

- A recovery in compression technologies sales or a sale of the unit could lead to a re-rating.

The third point is best expressed by comparing the company, which getsaround 80% of its revenue from climate technologies, withLennox International, apure-play HVAC stock. As you can see below, Ingersoll-Rand trades at a substantial discount.

LII EV to EBITDA (Forward) data by YCharts.

On an absolute basis, Ingersoll-Rand looks a little cheap, but it's hardly a screaming buy. A forward P/E ratio of 16.5 times earnings isn't anything to write home about, even if the stock trades on a forward free cash flow-to-enterprise value (market cap plus net debt) yield of 5.2%.

All told, Ingersoll-Rand still looks like a good value, but not by much. The stock needs to deliveron itsmargin expansion plans in the climate segment and see some better industrial conditions in order to move significantly higher from here.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Lee Samaha has no position in any stocks mentioned. The Motley Fool owns shares of Johnson Controls. The Motley Fool is short Johnson Controls. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.