Better Buy: Chipotle Mexican Grill, Inc. vs. Panera

Chipotle (NYSE: CMG) and Panera Bread (NASDAQ: PNRA) compete for the same customers using a similar strategy.

Both companies have pushed the idea that they offer better food than their cheaper fast-food rivals. That has allowed them to price higher, discount less, and attract an audience seeking a better, but still relatively quick and inexpensive, meal.

Chipotle has branded its initiative "Food With Integrity." The company defines that on its website as a commitment to "sourcing the very best ingredients we can find and preparing them by hand."

Panera has gone even further in that direction by offering what it calls a "100% clean" menu. That, according to a press release, means its menu is now "free from all artificial flavors, preservatives, sweeteners, and colors from artificial sources as defined by the company's No No List, inclusive of 96 separate ingredients and additive classes."

Of course, offering food that is actually fresh and not swimming in preservatives has its risks. Chipotle has been struggling since it was hit with multiple E. coli outbreaks beginning in July 2015. And even though the company has taken extensive steps to prevent future problems, its business has yet to bounce back. Panera faces the same risks, but ultimately both companies' futures are not directly linked to food safety (though it may be a while before former Chipotle customers agree with this statement).

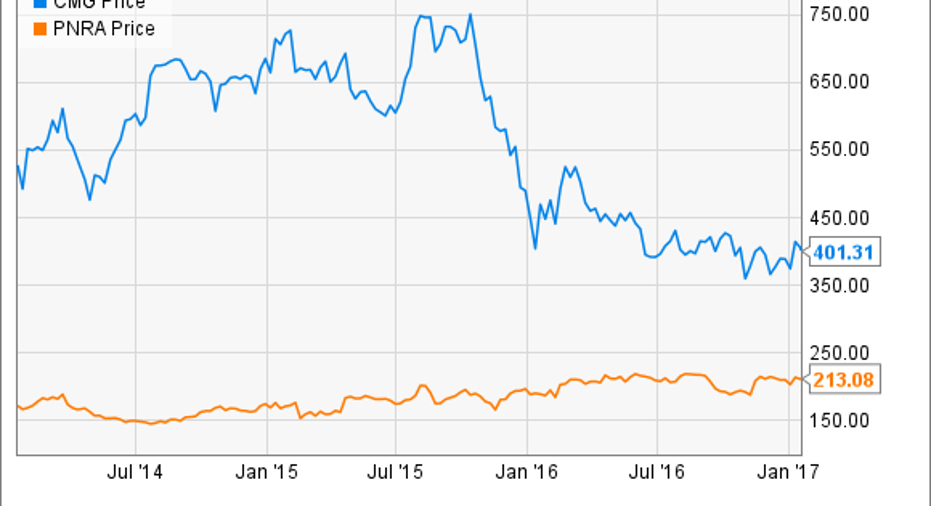

Panera's share price has inched up over the past three years, while Chipotle's fell off a cliff. Image source: YCharts.com.

The case for Chipotle?

Chipotle has been made to suffer for its food-safety issues even though it has gone more than a year without a recurrence. Despite that, the company continues to struggle to lure back customers. In Q3 it reported a 14.8% drop in revenue, as well as a decrease in comparable-restaurant sales of 21.9%.

Whether you should buy Chipotle shares depends on whether you believe that at some point people will begin forgiving the chain. That should eventually happen, though it won't be soon, because some lapsed customers have likely found other places where they prefer eating.

Still, time will heal this wound, and in the coming year the chain will face favorable comps. That should help it start to post increased sales and traffic, while its various promotions and new menu items slowly win people back.

Essentially, you can buy Chipotle shares at a discount from when the company was flying high. It may take a long time for the chain to hit its former heights, but the fundamentals of its brand have not changed. Chipotle does offer a quality meal at a decent price -- its food is better than that of fast-food chains -- and ultimately that should carry the day.

The case for Panera

In addition to being very focused on its clean-food efforts, Panera has also been very aggressively adding technology to its stores. The chain now offers mobile order and pay in most locations, while it's also vigorously rolling out delivery in appropriate markets.

Mobile order and pay could be a growth driver because it takes the waiting out of the restaurant experience for repeat customers. It also takes the regulars out of the line, which makes stores more inviting for casual users.

Those investments could help Panera improve its financial performance, which has been steady but unspectacular. In its most recent quarter, the chain reported that comparable sales in company-owned restaurants (bakery-cafes in company-speak) were up 3.4% year over yearand up 7.2% on a two-year basis. In addition, the company saw an 8% increase in GAAP net income for Q3 and a total revenue increase of 3%.

Panera has not been flashy and it's growing like a well-managed, mature business, not like the emerging brand some of its even-bigger rivals are seen as. That's a perception that likely drags on its stock price, and it's one the company will struggle to change even as it sits as a technology leader compared to most restaurants.

Is Chipotle or Panera a better buy?

Panera is a safe play. The company has a strong strategy and has stuck to it while investing in proven technology, which has worked well for its most-direct competitors (Starbucks and Dunkin' Donuts).

Chipotle, on the other hand, has more upside -- as long as you believe that at some point consumers will stop making E. coli jokes and remember that the chain offers really good food for the price. Its current price makes Chipotle the better buy. The company will eventually emerge from its troubles, and when it does, it should be able to start growing again, because at its core, the brand has a solid product.

10 stocks we like better than Chipotle Mexican Grill When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Chipotle Mexican Grill wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of January 4, 2017

Daniel Kline has no position in any stocks mentioned. He enjoyed the new Chipotle chorizo, which he tried for the first time this week. The Motley Fool owns shares of and recommends Chipotle Mexican Grill, Panera Bread, and Starbucks. The Motley Fool has a disclosure policy.