What Intel Corporation's Coffee Lake Means for Margins

Image source: Intel.

Thanks to leaks from both PC Watchand DIGITIMES, we now know that microprocessor giant Intel (NASDAQ: INTC) is planning to do something interesting with the products that it plans to launch for the personal computer market.

For thin and light notebooks, these reports suggest that the company intends to transition to products built with the company's new 10-nanometer chip manufacturing technology, known as Cannon Lake. However, for higher-performance products -- such as higher-performance notebooks and desktop personal computers -- the company plans to build a fourth generation of products, known as Coffee Lake, on its more mature 14-nanometer technology.

In this column, I'd like to explore the potential implications that this move could have on Intel's gross profit margins in the second half of 2017 to second half of 2018 time frame.

Some background on Intel, manufacturing tech, and margins

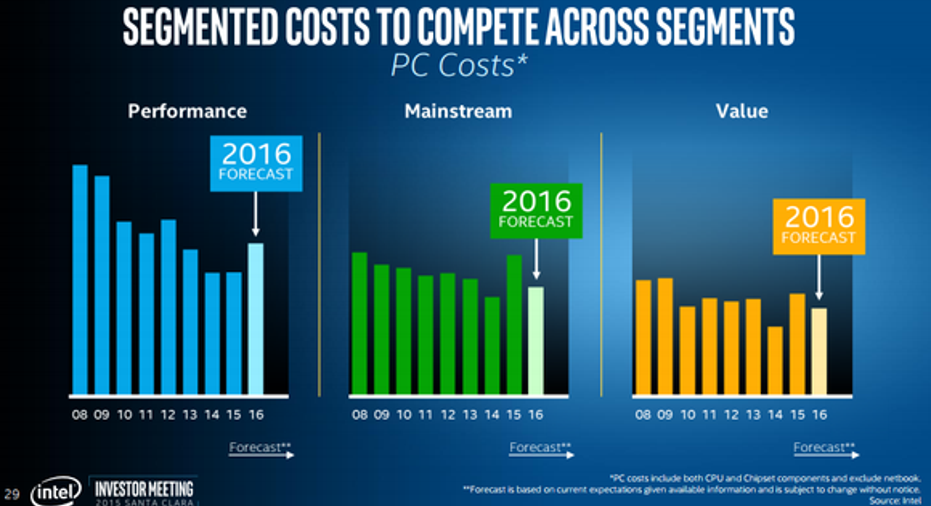

When Intel transitioned its personal computer product lines from its 22-nanometer technology to its 14-nanometer technology in 2015, the company's gross profit margins were negatively impacted. This was due to the fact that worse-than-expected manufacturing yields on its 14-nanometer manufacturing technology leading to increased product manufacturing costs generation over generation, as the following slide shows:

Image source: Intel.

Notice in the slide that in the "mainstream" and "value" segments of the personal computer chip market, Intel saw its costs rise significantly from the very low levels seen in 2014? This was due to the fact that Intel largely transitioned these product families from older 22-nanometer manufacturing technology to newer 14-nanometer technology.

The "performance" segment actually saw costs remain flattish because the company didn't introduce desktop processors on 14-nanometer until the end of 2015; the company predicted that costs in this segment would surge in 2016 as product costs went up as a result of the 22-nanometer to 14-nanometer transition kicking in.

With this background in mind, we can understand Intel's strategy vis-a-vis Coffee Lake and Cannon Lake.

Partially offsetting the hit to mainstream by keeping performance 14-nanometer

Beginning in late 2017 and extending through 2018 (so this discussion is centered around 2018 margins), Intel's mainstream product line will likely wholesale transition from 14-nanometer to 10-nanometer. I suspect that this will lead to an increase in product costs (I'm assuming that Intel's 10-nanometer yields won't be great out of the gate), diluting gross profit margins.

In terms of the slide above, I would expect 2018 mainstream product costs to tick up fairly significantly from where they will be in 2017.

However, for the performance segment, I could see costs staying roughly flattish to 2017 levels (assuming that Coffee Lake doesn't add so much additional die area that it winds up ballooning product costs anyway).

It's not clear what Intel's plan for the "value" segment is just yet. This segment is largely addressed by the company's Atom-based products sold under the Pentium and Celeron branding. In early 2015 these products transitioned to 14-nanometer and Intel recently released a new, second-generation Atom architecture.

It took Intel roughly a year and a half to transition from the 22-nanometer Atom (launched in the third quarter of 2013) to the first 14-nanometer Atom (first quarter of 2015). It was also another year and a half to go from the first 14-nanometer Atom to the second 14-nanometer Atom product.

Assuming that it takes Intel another year-and-a-half to transition Atom from 14-nanometer manufacturing to 10-nanometer manufacturing, we should expect the company to release 10-nanometer Atom-based processors for low-cost PCs in the first half of 2018.

In this case, I would expect a negative impact to Intel's margins from that particular transition.

All told 2018 might be a year in which Intel sees product costs increase (negatively impacting gross profit margins to some degree) as a result of the 10-nanometer transition, but by keeping a large portion of its shipments on 14-nanometer, it can soften that blow quite a bit.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Ashraf Eassa owns shares of Intel. The Motley Fool recommends Intel. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.