3 Dividend Stocks to Make Your Retirement Sweeter

Image source: Getty Images.

In America, death rates have been dropping for nearly all leading causes of death, according to a government report. That means you could easily have several decades to think of fun things to do during your retirement. Unfortunately, a longer life also means more opportunities for an ugly stock market downturn that could torpedo your portfolio.Your goal for retirement may be to join a punk rock band, climb Mount Everest, or just watch a lot more TV. But whatever your plans may be, you'll have a lot more fun if your investments provide steady, growing income.

So how can you protect yourself? One approach is to focus on less volatile stocks that will pay you a growing dividend.

In addition,the healthcare sectoris a terrific place to look for retirement stocks.Thesector tends to outperform the broader market: Asmeasured bythe Health Care Sector SPDR ETF(NYSEMKT: XLV), healthcare hasgained126%over the past 10 years, whereas the S&P 500 has gained 68%.

With the exception of biotechs, healthcarestocks also tend to hold upbetter in bear markets.During the 2007-2009 bear market, the S&P 500 lost 50% of its value, while the Health Care SPDR ETFtook only a 39% dip.Sweetening the potfurther, two major trends will likely keep this sector pumping for a long time. As people age, they need more healthcare, and the number of those aged 65 and over is forecast to nearly double to 83.7 million by 2050. In addition, the rise of the middle class around the world, particularly in Asia, means the demand for healthcare shouldgrow abroad as well.

While the healthcare sector is rife with opportunity, you might start your search with the following three stocks.

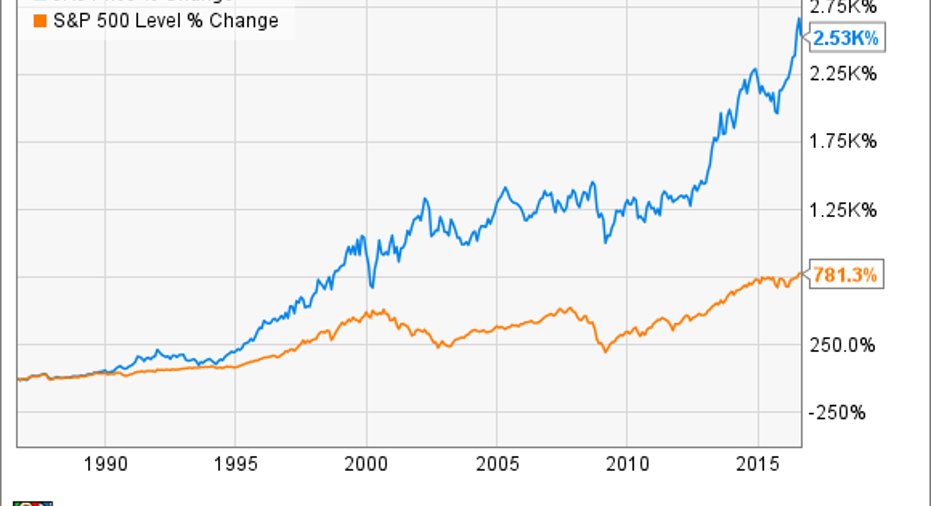

Johnson & Johnson: solid as they come

Few stocks can match global healthcare titanJohnson & Johnson's (NYSE: JNJ) epicperformance. It hasincreasedits dividend for 54 straight years, and it has been soundly beating the market for decades. Here's how it stacks up to theS&P 500over the past 30 years:

And that's not even including reinvested dividends, which would have doubled Johnson & Johnson's return over that period.

One of the greatest things going for J&J is its growth consistency. The company hasachievedsolid earnings increasesfor 32 straight years.Its earnings growth consistency owes largely to the fact that the company has over 250 subsidiaries coveringthree divisions: consumer health, medical devices, and pharmaceuticals. That kind ofdiversity meansthebusiness can put up great numbers overall, even if a particular subsidiary is lagging.

While J&J'sconsumer health and medical-device segmentsaregenerally lower-margin andtend to be slow or flat in growth,J&J'shigh-margin pharmaceutical sector has been lighting a fire under this stock.The company hasseengreat commercial success withdrugs such asImbruvica, which it's marketing in partnership with AbbVie. Imbruvica's first-half 2016 salesdoubled year over year to $556 million, and annual revenue is expected to peak at more than $5 billion before long.Invokana, anotherfast-growing drug,could potentially bring in more than $1 billion annually. J&J's pipeline should bear fruit as well: The company has announced plans for 10 new large-scale drugs to reach the market by 2019.

There is one caveat to all this: J&J currently trades at nearly 23 times its trailing-12-month earnings.That's a hefty ratio, even considering this company's history of commanding a premium. Further, it's yield of 2.7% is slightly below its five-year average yield of 3%. I've owned J&J a long time, and I consider it a "forever" stock. However, I think itmay bedue for a pause, or perhaps even a temporarypullback, which would allow investors to get in at a better price point.

Don't get me wrong -- J&J is stillone of the best names retireescan buy long-term.With a perfect "AAA" credit rating andplenty of cash on hand, this company epitomizesa safe long-term bet.

Pfizer: thrown off track but coming back

While J&J's stock has been on a tear, the second-largest drug manufacturer in the world, Pfizer, Inc.(NYSE: PFE), has been a laggard until recently.That's good news for investors, because it means the stock has some room to catch up.

Pfizer has been suffering from patent losses, but last quarter, overall revenue grew 11% from the second quarter of last year. That's amazing, considering what the drugmaker rakes in on a quarterly basis.Revenues totaled $13.1 billion in Q2,an increase of $1.3 billionfrom the year-ago quarter.While some of that bump was due to the consolidation of its Hospira acquisition, Pfizer has a key growth-driver going forward in the oncology segment, beginning with the newly approved breast cancer drug Ibrance.

Pfizer also has astrong free cash flow, which rang in at$13.8 billion over the last four quarters. That comfortablycovers the $7.1 billion the company paid out in dividends.The giant pharma hasalso been making somesmartacquisitions recently, includingAnacor Pharmaceuticals andMedivation. Both deals will add some neededzip to the pharma's pipeline. In addition,Medivation's already marketed prostate drug Xtandiis projected to be one of the top-selling oncology drugs by 2021.The drug could achieve $7 billion in sales, which would really bulk upPfizer'sbranded-drug portfolio.

What about the dividend? It was recentlyraised7.7% to $1.12, which lifts the yield to 3.4%,well above the S&P 500 average of 2.1%. Over time, that dividend looks set tokeepgrowing. Assuming Pfizer's shareprice also moves up, buying this pharmanow could lead to a sweet cost-basis yield in your retirement.

UnitedHealth Group: slow,but rarely misses a beat

The healthcare sector contains much more than drugmakers. Some of the most lucrative and defensive stocks available are healthcare insurance providers. Despite worries that Obamacare would spell disaster for this sector, the industry has posted growth since the bill passed. Among the companies raking it in, UnitedHealth Group, Inc.(NYSE: UNH)stands out as offering the best of both worlds: dividend income and earnings growth.

While United Health currently offers a modest dividend of 1.75%, that's higher than the current yield from competitors Humana, Cigna, and Aetna. In addition, United has a commitment to returning value to shareholders: It raised its dividend by 25% this year and by 33% in 2015.

Powered by its health-services arm, Optum, which showed revenue jumping 51% to $20.6 billion, the company posted a strong earnings beat last quarter and lifted the low end of its guidance for 2016. Better yet,to axe any losses related to Obamacare that could pull down overall earnings going forward, United has said it will exit a number of unprofitable exchanges.

All three of these stocks shouldkeep paying out growingdividends that willmake your retirement sweeter. That just leavesone big question unanswered: What willyou do with all that free time and all thatdividend income?

Well, howabout joining thatpunk rock band? Here's what Jodina, the lead vocalist for Arizona punk band One Foot in the Grave, had to say: "Just 'cause you're old doesn't mean you can't get up and do something different."

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Cheryl Swanson owns shares of Johnson & Johnson. The Motley Fool owns shares of and recommends Johnson & Johnson. The Motley Fool recommends UnitedHealth Group. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.