4 Huge Social Security Mistakes You Should Avoid

Image source: Getty Images.

So you've worked for decades and paid Social Security taxes the whole way through. The time has come for you to start collecting money from the program, instead of paying into it. You deserve it!

But if you commit one of the four errors described below, you'll be doing is shooting yourself in the foot. Don't let that happen. Before you claim Social Security, you should learn about these pitfalls so you can avoid them.

1. Failing to coordinate with your spouse

Married couples are a team, so their combined income is more important than their individual incomes. Both partners will benefit if they combine their Social Security resources. This means carefully considering when each spouse should file for benefits.

You can claim Social Security as early as age 62, but your benefit will increase for every year you delay, up until age 70. Statistically speaking, men tend to earn more than women, and they also tend to have shorter life spans. If you and your spouse are more or less average in those regards, then it makes sense for the husband to put off filing for benefits as long as possible, up to age 70.

That's because when one spouse passes away, the other gets to assume his or her full benefits. If a husband waits until age 70 to file for Social Security, then he is ensuring that when he passes away, his wife will get the maximum possible benefit. The wife can claim at an earlier date, and that money can help the couple make ends meet until the husband claims.

Also look into whether either spouse would come out ahead by claiming spousal benefits, rather than benefits based on his or her own work record.

2. Forgetting about the option of claiming based on your ex's history

Many people forget they can claim benefits based on a former spouse's working history. As long as you and your ex were married for at least 10 years, and you haven't remarried, then you are eligible to receive benefits. But there are important caveats to consider:

- If you had a higher earning record than your spouse, then having a qualifying ex can't raise your potential benefit.

- If you claim spousal Social Security benefits from an ex-partner, then you will be unable to claim benefits from your own work record. This means you can't collect "spousal" benefits based on your ex-spouse's record until age 70 and then collect your own maxed-out benefits.

3. Not realizing that benefits can be taxed if you're working

Some people, in an effort to make ends meet, will continue working after they file for Social Security benefits. Others will go back to work in retirement simply because they want to. In any case, working Social Security beneficiaries must know how their earned income may affect their benefits. If you earn above a certain amount on the job, then your benefits will be taxed.

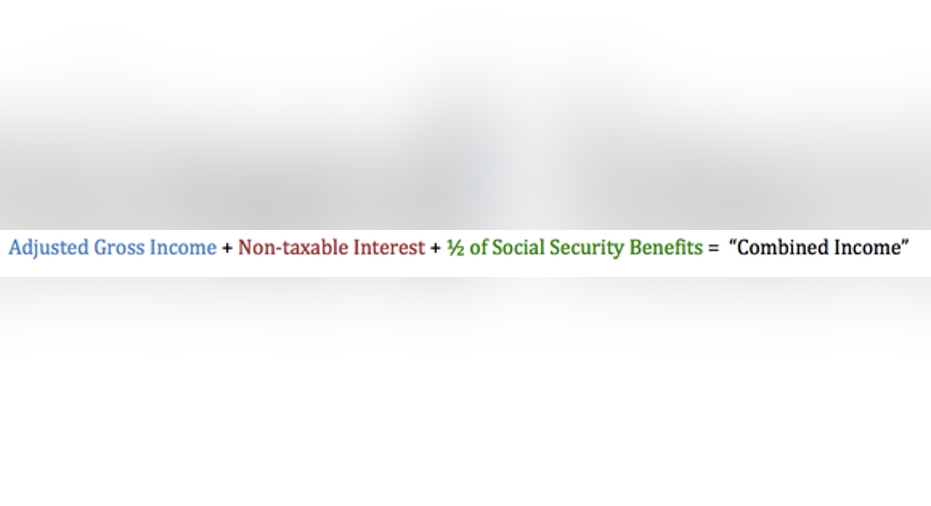

To figure out whether you'll have to pay taxes on Social Security benefits, you need to find out what your "combined" income is. The equation for that goes like this:

For couples filing jointly, if your combined household income is between $32,000 and $44,000 ($25,000 and $34,000 for individuals), then you may need to pay income tax on up to 50% of your Social Security benefits. If you're married filing jointly and your combined income exceeds $44,000 ($34,000 for individuals), then you may have to pay taxes on up to 85% of your Social Security benefits.

4. Not working for at least 35 years

The formula that calculates how large your monthly Social Security check will be depends largely on two factors: the age at which you file and the average earnings of your 35 highest-earning work years. If you retire before clocking in all 35 years, then your benefits could come in lower than you expected. For any "leftover" years short of 35, your earnings are counted as $0, which could substantially lower your average.

Let's put this in perspective: Say you earned an inflation-adjusted average of $50,000 per year, but you only worked for a total of 30 years. Your "average income" for Social Security's purposes would dip all the way to $42,900 -- and reduce your annual benefit at full retirement age by more than 10% from $21,965 to $19,680.

If you find yourself in a situation where any one of these mistakes might cost you in the future, then start taking steps today to avoid those pitfalls. Americans rely heavily on Social Security, and you deserve no less than your maximum benefit.

The $15,834 Social Security bonus most retirees completely overlook If you're like most Americans, you're a few years (or more) behind on your retirement savings. But a handful of little-known "Social Security secrets" could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $15,834 more... each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we're all after.Simply click here to discover how to learn more about these strategies.

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.