Forget American Express Company: Here Are 3 Better Dividend Stocks

Image source: Getty Images.

American Express (NYSE: AXP) is a great company. It's returns on equity are best in class, and its brand is ubiquitous around the world among the most-affluent and sought-after customers. However, when it comes to dividend investing, American Express stock leaves a lot to be desired.

For income investors, I think it may be time to forget American Express company. Here are three better options in the credit-card and payments business.

|

Company |

Stock Ticker |

Dividend Yield |

|---|---|---|

|

American Express Company |

AXP |

1.82% |

|

Discover Financial Services |

DFS |

2.15% |

|

JPMorgan Chase |

JPM |

3% |

|

First Republic Bank |

FRC |

0.89%* |

*Yes, this is a pretty low yield. Bear with me for just a moment, and I'll explain the rest of the story.

Data source: Google Finance.

Discover Financial Services has a similar business model, but with more dividends

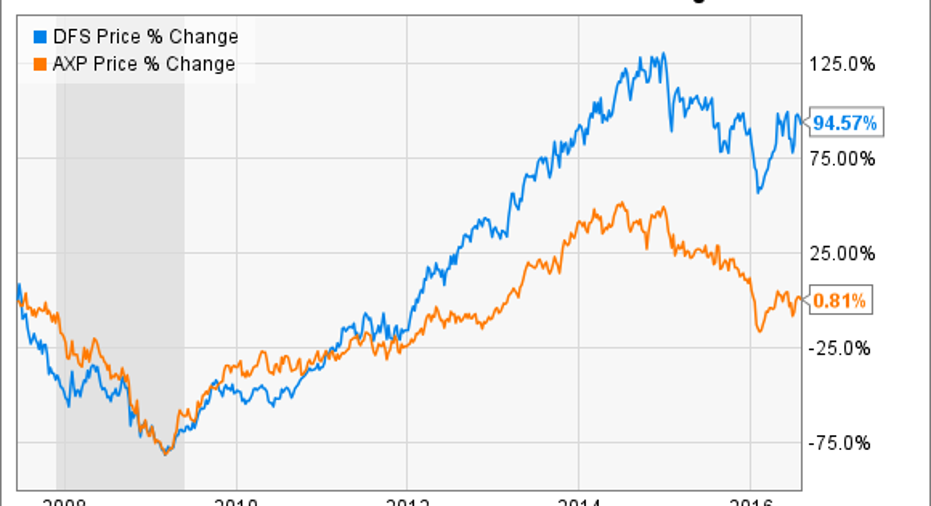

The first American Express alternative is a company with a very similar business model, Discover Financial Services (NYSE: DFS). Like AMEX, Discover is a payment processor, managing the digital transactions between consumers and businesses anytime a Discover-branded credit card is used at check out. Like American Express, Discover provides banking services to its clients, like deposit accounts and loans.

American Express has traditionally been the bigger fish in the pond compared to Discover. However, in recent years, Discover has outperformed its larger competitor in several meaningful ways. Discover's annual revenue has grown faster than American Express's over the past five- and 10-year periods, and its stock's performance has beaten AMEX's by a mile, for example.

American Express has better returns on equity than Discover, and that fact helps contribute to Discover's slightly lower price-to-earnings ratio. However, the lower valuation also helps to drive Discover's dividend yield higher, even though both companies have comparable dividend-payout ratios.

If it's the credit-card business you're after, try JPMorgan Chase

Credit cards and payment services are only a slice of JPMorgan Chase's (NYSE: JPM) massive operations, but income investors with an eye toward this niche should still consider the bank and its 3% dividend yield.As of the second quarter, JPMorgan was the largest bank in the U.S. by total assets and quarterly net income. It was also the largest credit-card issuer based on loans outstanding.

A credit-card issuer is the actual lender that holds the credit-card debt. That contrasts with payment processors like Visaor MasterCard, which manage the digital infrastructure that connects the credit issuers with the merchants and consumers in the transaction. Credit issuers primarily make money through interest income, while payment processors charge fees on each transaction. American Express is a hybrid of the two, acting as both payment processor and credit issuer when consumers use their AMEX cards.

This megabank trades at just less than 11 times its trailing 12-month earnings, a lower multiple than each of the other U.S. megabanks (except for the beleaguered Citigroup). To me, that valuation is a bargain. Its returns on equity are well above the industry average, its balance sheet is well-capitalized, and the bank has one of the strongest records of performance in all phases of the credit cycle. On the same trailing 12-month basis, its dividend yield is more than double that of Bank of America's, and nearly four times higher than Citi's.

In my view, JPMorgan is a diversified and stable financial services giant, still offers investment exposure to the credit-card and payments market, and is attractively valued at current prices. Plus, its dividend yield is significantly higher than American Express's.

First Republic Bank isn't a major credit-card player, but check it out, anyway

First Republic Bank (NYSE: FRC) is a niche bank, insofar as any institution with over $64 billion in total assets could be considered niche. First Republic's niche is providing financial products tailored to the needs of the nation's wealthiest individuals. The bank is based in California, but does business in a handful of select coastal cities on the East and West coasts, which are chosen because of the high concentration of wealthy and ultra-wealthy individuals who live there.

By focusing on the financial elite, First Republic is able to maintain exceptional credit quality. That protects both profits and capital throughout the economic cycle because the wealthiest individuals have the capacity to continue making their loan payments even when the economy hits a speed bump.

The bank's numbers show just how well the concept works. For example, the average mortgage borrower at First Republic between September of 2014 and June of 2016 had a credit score of 774, $618,000 in liquid assets, and put down an average down payment of 40%.

Maintaining such high credit standards has not slowed down the bank's financials, either. Second-quarter revenue was up 17% year over year, tangible book value per share increased 13.8%, and the bank originated an all-time record $6.5 billion in new loans during the quarter. Looking longer term, the bank's enterprise value has increased at a compounded annual growth rate of 23% since the bank was founded in 1986.

But the dividend only yields 0.89%. That's true of the bank's common stock. From time to time, though, First Republic will also issue preferred shares to fund its growth. There are currently seven issues of preferred shares outstanding, each with dividend yields above 5%.

Preferred stock investments come with their own set of risks distinct from common stock, but in this case, I think First Republic has the stability and the track record to justify a closer look at these big preferred dividends.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Jay Jenkins has no position in any stocks mentioned. The Motley Fool owns shares of and recommends MasterCard and Visa. The Motley Fool recommends American Express and Bank of America. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.