The 3 Best Ages to Start Taking Social Security

Image source: Getty Images

You can start receiving your Social Security retirement benefits as early as age 62, but the longer you wait beyond that, up to age 70, the higher your monthly checks will be. The trade-off, though, is that the longer you delay, the fewer checks you'll receive over your lifetime.

Due to that, it's only natural that every retiree would want to figure out what the best age will be for them to start taking benefits. Actuarially speaking, the total benefits you collect are expected to be about the same over the course of your retirement no matter when you start. Despite that fact, there are three key ages that stand out as the best ages to start taking benefits, depending on your personal circumstances. Those ages are 62, your full retirement age, or age 70.

When is 62 a great age to take Social Security?

The earliest you can start taking Social Security retirement benefits is when you turn 62, and it is by far the most common age for people to start claiming them. The obvious upside to taking the money early is the fact that you get the cash in your pocket at a younger age, and you'll be collecting it for the longest possible period of time. In addition, if you're living off your investments, those early Social Security checks can cover a decent chunk of your monthly expenses, which will let you keep more of your money in growth-oriented investments for longer.

There are two key downsides to taking your benefits early, though.

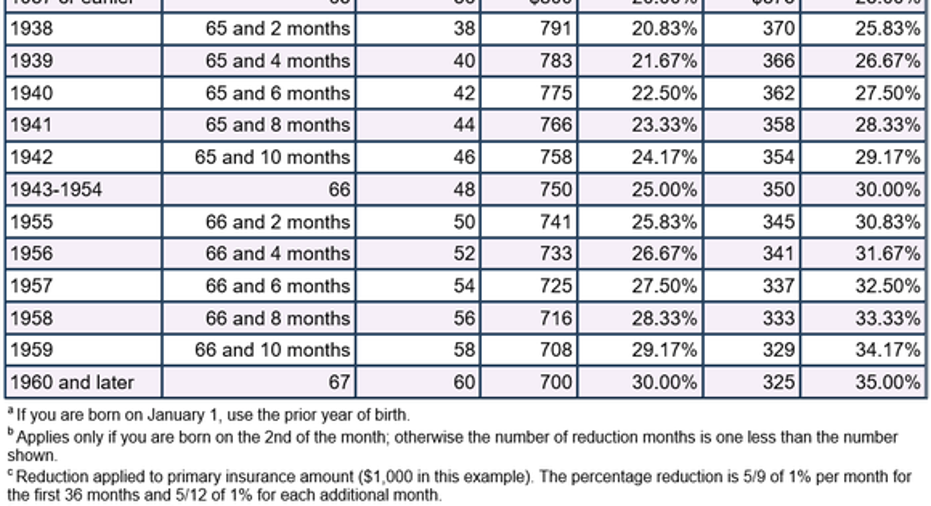

First, your monthly check will be permanently reduced compared to what it would have been if you waited until your full retirement age. The table below shows how much your checks will be reduced for taking benefits at 62, depending on your year of birth, and whether you're taking primary or spousal benefits.

Source: Social Security Administration

Second, if you're under your full retirement age and still working while collecting Social Security, there's a substantial penalty that reduces your benefits even further. In 2016, that penalty is $1 for every $2 you earn over $15,720. In the year you reach your full retirement age, for the months prior to reaching that full retirement age, the penalty drops to $1 for every $3 you earn over $41,880.

While you'll eventually get that money back after you reach your full retirement age, it makes little sense to take that permanent reduction in your benefit to get the money early -- and then not end up seeing that money early.

As a result, 62 can be a great age to start taking your Social Security, but only if you're no longer working and one of the following is true:

- You either really need the money to make ends meet, or

- By taking Social Security early, you can keep more of your money in growth-oriented investments for longer, giving you a chance to improve your total lifetime cash flow.

When is your full retirement age the right time to file?

Starting to take Social Security at your full retirement age gets you two key benefits over starting earlier. First, you'll get exactly the full benefit that Social Security calculates based on your earnings history. Second, you can keep working and earning money without penalty while receiving Social Security benefits. The same table shown above shows what your full retirement age is, based on the year you were born.

In addition, if you're still working past your full retirement age, taking Social Security anyway can give you the opportunity to top off your tax-advantaged retirement investment accounts. As long as your earned income allows, while you are in your 60s, you have the opportunity to make catch-up contributions to your 401(k) and IRA plans. In 2016, those catch-up contributions mean you can potentially invest a total of $6,500 per year in your IRA and $24,000 in your 401(k).

If the extra income from Social Security lets you sock away more of your paycheck toward your retirement, it can improve your financial position for when you do call it quits for good. On the flip side, if you're not confident in your ability to invest that additional money profitably, waiting to collect will get you about an 8% increase in benefits every year you wait past your full retirement age, up to age 70.

Note that depending on your total income level, up to 85% of your Social Security benefits can be subject to income taxes. So if you're still working and considering collecting Social Security at your full retirement age, be sure you've got a good use planned for that money. Otherwise, the 8% increase per year of waiting might be a better option than collecting the extra income and seeing a portion of it taxed away.

Image source: Getty Images.

When is 70 a great age to take Social Security?

Once you reach age 70, there is no benefit to continuing to wait to file for Social Security, which makes it the last great age to start collecting if you haven't already. Even if you have substantial income from other sources and don't need the money to support your lifestyle, there's no point in waiting anymore. You can always donate it to a worthwhile charity or use it to fund a gifting program to your children.

Note that while waiting until age 70 to collect will give you your largest possible monthly Social Security benefit, it's only a good idea to wait that long if you've got the ability to cover your expenses from other sources. It makes no sense to skimp painfully through your 60s in order to get a bigger payday in your 70s and beyond.

Whatever age you choose can be the right one for you

These key milestone ages are great points at which to start taking your benefits, but it's important to remember that unless you face special medical or lifestyle conditions, your lifetime benefit is likely to be about the same no matter what age you choose to start taking your payment.

With that in mind, any filing age that helps you meet yourretirement needs can be a great age for you to start taking your Social Security benefits. Just be sure to understand the way your age, your total income, and any taxes and penalties you might face will affect your finances, and make your choice with an eye toward your plans and needs throughout your retirement. That way, you can best use your benefit to make your golden years as comfortable as they can be.

The $15,834 Social Security bonus most retirees completely overlook If you're like most Americans, you're a few years (or more) behind on your retirement savings. But a handful of little-known "Social Security secrets" could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $15,834 more... each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we're all after.Simply click here to discover how to learn more about these strategies.

Chuck Saletta has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.