Billionaire Warren Buffett Hates This Investing Metric and You Should Too

Investing guru Warren Buffett thinks WACC is wack. Image Source: The Motley Fool

Investing is one of the few industries where complexity is favored over correctness. In this environment you'll find a tremendous number of performance metrics by which you can judge companies performance, many of which will directly conflict with one another. As an investor, it can be hard to separate superfluous valuation metrics from key, actionable data.

One such measure that's been bandied about is the weighted average cost of capital, or WACC. While it's considered a key metric among financial analysts and greater Wall Street, do not count Warren Buffett among its adherents. During Berkshire Hathaway's Annual Meeting in 2003, Buffett addressed WACC by responding:

WACC deconstructed

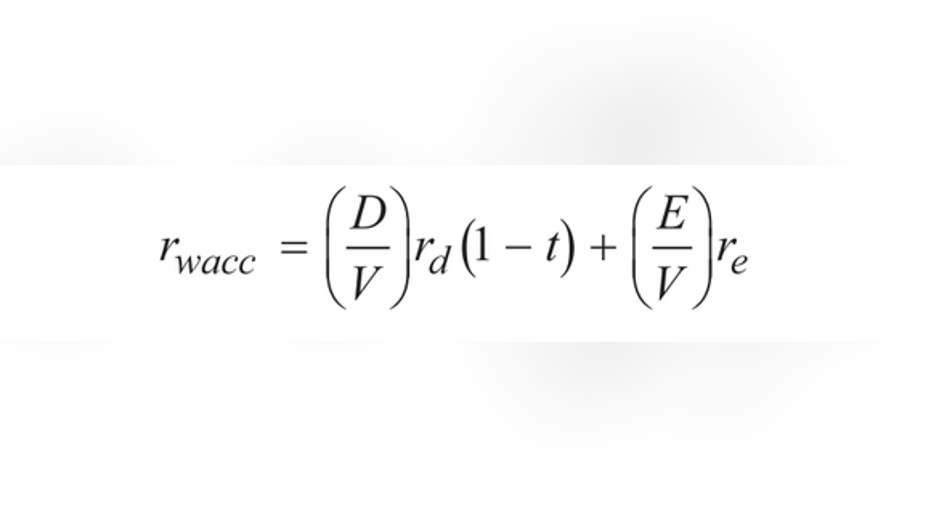

Weighted average cost of capital is a relatively easy concept to understand: It's the rate of return a company is expected to pay on its after-tax debt and equity, weighted by the percentage of firm value debt and equity represent. If you remember Accounting 101, assets equal liabilities plus equity, so WACC could also be defined as the cost of financing its assets.

Assuming a company has no preferred stock, here's the formula to calculate WACC:

Image Source: CFA Institute

Yet another way to think of WACC is as a "hurdle rate" for future projects. If the projected rate of a return of a new project -- an asset -- exceeds the weighted average cost of capital to finance said project, then capital finance dictates the firm should take the project to increase their value.

This is the underpinning of the Federal Reserve's rationale for lowering the fed funds rate: Lowering that key interest rate lowers rates across the board, making formerly unprofitable projects profitable, which boosts employment as firms require increased labor to complete them.

WACC is an important calculation for corporate and managerial finance, but it's certainly less useful for investors.

Problems with WACC

There are a few problems with WACC. The first is that the financing costs of equity are difficult to calculate. As the formula above shows, one needs to know the rate of return and the values the market puts on equity. Unfortunately, the method used to calculate these numbers can be as complex as discounting projected cash flows for decades, using an estimate of the equity risk premium in the capital asset pricing model, or simply using a heuristic "rule of thumb" estimate. All three of those estimation methods will produce different results, and are sensitive to even minor input variances.

The biggest problem with WACC, however, is that it doesn't accord with traditional stock valuation metrics. For an example, Guru Focus currently estimates Apple's WACC at 11.5%. Under WACC, then, Apple should undertake any investment in which they could produce a return greater than 11.5%.

However, if Tim Cook announced Apple was getting into appliances like microwaves, refrigerators, and ovens tomorrow, it's highly likely the investing community would react unfavorably, and the stock price would suffer. For a comparison, Apple's gross margin is heavily watched; the investment community excitedly starts to declare post-peak Apple anytime it drops below 39%. As of last quarter, Apple's net profit margin was 20.8% last quarter, nearly double its WACC.

Buffett is right

The differences between the WACCvaluation and the stock valuation are mostly due to valuation multiples. WACC essentially values a firm on an accounting basis, with no value assigned to future earnings or growth. In Apple's case, the market currently values the company at approximately 10 times its current earnings, due in large part to its growth potential. And that P/E is well below the P/E of the broad S&P 500 , which currently trades at a rate of about 24 times earnings.

In the aforementioned Apple scenario, it's highly likely investors would take Apple's move into kitchen appliances as an admission that its high-growth days in consumer electronics were over -- a signal that the company should trade at even lower valuation multiples, even if it was able to clear the hurdle rate of 10.5% with these products.

Finally, even changes in WACC can be misleading when used to value a stock. While an increase in WACC can certainly signify a company under duress -- reflective of investors asking for higher equity or debt rates of return -- it could equally be due to a Fed interest rate hike, or other macroeconomic effects. Additionally, an increase in a company's WACC isn't always a negative, especially if the increased costs are being taken on in order to take advantage of projects with above-average payoff potential.

Buffett is right here: WACC is an overrated concept as it relates to investing. There's no problem with occasionally monitoring this metric, but it shouldn't play a large role in your investing thesis.

The article Billionaire Warren Buffett Hates This Investing Metric and You Should Too originally appeared on Fool.com.

Jamal Carnette owns shares of Apple. The Motley Fool owns shares of and recommends Apple and Berkshire Hathaway (B shares). The Motley Fool has the following options: long January 2018 $90 calls on Apple and short January 2018 $95 calls on Apple. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.