5-Point Checklist for Investing in Big Oil

Image source: ExxonMobil investor presentation.

In the stormy seas of the energy market, Big Oil companies have been one of the few beacons of stability. As oil prices declined more than half over the past couple of years, companies with exposure to every facet of the oil and gas value chain saw declines ranging from 10% to 30%. To some, this stability and the traditionally generous dividends have made for a compelling investment thesis, but actually getting to know and understand the complex world of Big Oil companies is far from simple.

So to help you have a better understanding of these stocks, here's a five-point checklist when looking at the big five oil and gas companies -- ExxonMobil , Chevron , Total , Royal Dutch Shell , and BP -- and a few metrics of each that should help you in your investment decisions.

1. Does it have robust resources to grow production for years to come?

This question is pretty obvious, but there is more to it than just what the production outlook is over the next several years. Companies in the Big Oil business need to have a large quiver of assets that are about to come online, under construction, under evaluation, and under exploration to maintain and grow production over time.

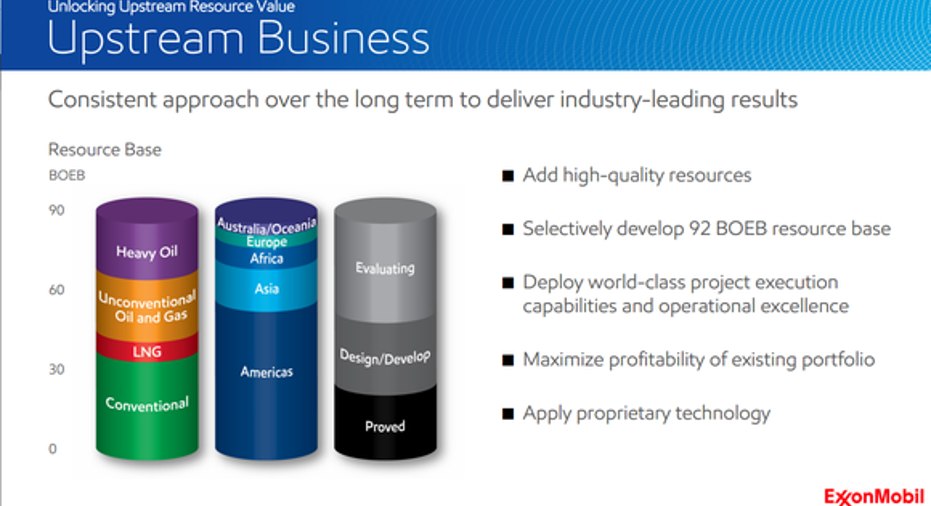

Let's use ExxonMobil as an example. The company produces about 4 million barrels of oil equivalent per day (BOE/D). It has about 450,000 BOE/D slated to come online this year and next to replace declining production and generate some modest growth, 25 billion BOE of proven reserves that are either producing assets or projects under construction, and more than 90 billion BOE of potential resources that are currently being explored or under evaluation.

Image source: ExxonMobil investor presentation.

Every Big Oil company has a portfolio like this, and each typically discloses it in its investor presentations. The most important thing to look for here are reserve replacement rates -- the amount of new resources being added to proven reserves divided by total production. With such large proven reserve bases, these companies don't necessarily need to replace their reserves every year -- although some view it as a point of pride to do so -- but over periods of a few years we want to see reserves being replaced faster than production takes them away.

2. Is that production from a low-cost source?

Having a lot of production growth waiting in the wings is nice, but it's worthless if that production is an expensive source that will provide marginal profitability at best. There is no real way for individual investors to know the profitability of each production source for a company. There are two reasons for this: One is that each company has widespread assets across the globe, and the other is that most of these companies won't disclose the profitability of individual assets.

Luckily, you don't necessarily have to go into that much detail. Instead, you can get a rough estimate by looking at the types of projects under development. The more expensive ones are typically those in very remote places that require building lots of infrastructure to get them completed. Projects like Arctic drilling or deepwater offshore reservoirs in places with little prior oil and gas development tend to be the more expensive ones.

You can also look at what the company is currently using as its oil price projection for its investment decisions. Each Big Oil company makes some budget estimates on what it believes is a reasonable price for oil in the future. Some companies are more ambitious with that projection, and others are more conservative. Here is a quick look at some of the recent low-price projections that Big Oil companies have featured in investor presentations.

| Company | Price Projection for Investment Decisions |

| BP | $50 |

| Chevron | $52 |

| ExxonMobil | $40 |

| Royal Dutch Shell | $45* |

| Total | $40 |

*Applies only to Shell's deepwater production assets; data on other production sources not given.Data source: Company investor presentations.

3. How big a role do its non-production assets play in profitability?

One thing to keep in mind with Big Oil companies is that they are more than just oil and gas producers. They also have large refining, transportation, chemical manufacturing, and retail sales footprints. These are the assets that help balance out a company's portfolio as oil and gas prices fluctuate, because refining and chemical manufacturing profits tend fluctuate in a direction opposite to that of production results.

You should keep two things in mind when looking at this part of the business: What is the company's balance between production and non-production assets? And are those non-production assets performing well enough to be a net positive for the company? Chevron, for example, is much more reliant on the success of the production side of its business than the other four companies, whereas Shell has some of the largest overall exposure to refining and chemical manufacturing -- although that could change as it sells off several assets after its recent BG Group merger.

4. Is it balancing its need to reinvest in the business and reward shareholders while living within its means?

This is probably the most challenging aspect for Big Oil's management teams. For the most part, investment decisions made today likely won't be cash-generating assets until several years down the road. So they all need to take a best educated guess about where there are gaps in the supply and demand of oil and gas, and how many investments should be made at the same time.

If commodity prices were constant and predicable, the job would be much easier. But we're talking about a commodity thatmoves up and down with an astonishing frequency. So at any given time in the future these companies have to model how much cash will be coming in the door based on certain price conditions, and how much they can spend while still rewarding shareholders with a stable dividend payment. Some companies are better at this than others, and a lot of it goes back to whether production comes from low-cost sources.

The best way to measure this is to look at the cash flow statement and compare the company's cash inflows from operations with outflows from capital expenditures and dividend payments.Of course, you shouldn't expect a company to do this perfectly year in, year out. The long development times of major projects and the volatility of the oil and gas markets mean that from time to time there will be cash shortfalls. However, a long-term trend where cash outflows outpace inflows and need to be helped with big asset sales or adding debt can be cause for concern.

5. Are shares reasonably priced?

To some, Big Oil stocks are like the old adage for IBMequipment: No one ever got fired for buying them. Big Oil companies are well-established companies that have long histories of generating returns for investors. At the same time, though, we have to acknowledge that these companies are in a cyclical industry, and buying them at the wrong time could lead to shares underperforming for a long time.That's why investors need to be a little price-cognizant when buying shares.

One of the better metrics for evaluating cyclical stocks that will see earnings fluctuate with commodity prices is the price-to-tangible-book-value ratio. This metric looks more at the value Wall Street is giving to the underlying assets of the company rather than the earnings those assets are generating at any given moment in time. Looking for shares with low price to tangible book values is a rough but pretty decent method of determining whether you are getting a deal on those stocks. Here is a breakdown of the Big Oil companies' price to tangible book value compared to their respective historical valuations.

| Company | 10-Year High | 10-Year Low | 10-Year Average | Current |

| BP | 3.92 | 1.04 | 2.20 | 1.61 |

| Chevron | 3.07 | 0.85 | 1.83 | 1.27 |

| ExxonMobil | 4.61 | 1.66 | 2.83 | 2.18 |

| Royal Dutch Shell | 2.77 | 0.76 | 1.56 | 1.05 |

| Total | 3.73 | 1.30 | 2.06 | 1.69 |

Price-to-book-value ratio for five big oil companies. Data source: S&P Capital IQ.

What a Fool believes

It's very easy to get lost in the weeds when trying to evaluate these companies. Their expansive footprints can make it hard to understand everything they do, and trying to factor what the price of oil will do to each of them will make your head spin. By focusing on these five aspects, though, you should be able to narrow your search down to the one or two stocks that are for you and figure out when would be a decent time to invest in them.

The article 5-Point Checklist for Investing in Big Oil originally appeared on Fool.com.

Tyler Crowe owns shares of ExxonMobil.You can follow him at Fool.comor on Twitter@TylerCroweFool. The Motley Fool owns shares of and recommends Chevron. The Motley Fool owns shares of ExxonMobil. The Motley Fool recommends Total. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.