2 Graphs Show Investors Won't Benefit From This "Black Swan" Again

U.S. stocks are lower on Friday on the back of a very disappointing jobs report for the month of May: The economy added just 38,000 jobs, far short of the 162,000 consensus estimate. TheS&P 500and theDow Jones Industrial Average (DJINDICES: $INDU)down 0.37% and 0.22%, respectively, at 12:30 p.m. EDT.

The next 10 years won't be as good as the last 40

No one ever accused Bill "the Bond King" Gross of not having an opinion. The PIMCO co-founder is always happy to share his thoughts, and he continues to publish his provocative monthly Investment Outlook from his new digs at Janus Capital.

In the latest installment, Gross argues that the high returns achieved over the last four decades on stocks and bonds amount to a rare event -- a " black swan" -- and are, therefore, extremely unlikely to be repeated over the next four decades (or the next 10 years). If that's true, it's not good news for the current generation of workers, who are saving for their retirement.

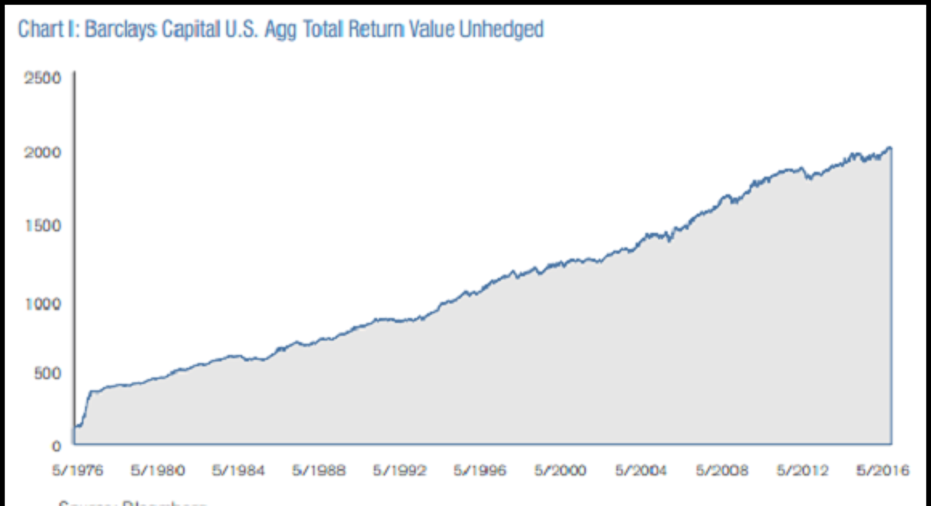

In support of his position, Gross produces two charts, the first one of which shows the total return of the Barclays Capital U.S. Aggregate Bond Index, the benchmark index for the U.S. bond market. The index includes investment-grade bonds across all segments (Treasury, agency, corporate, mortgage-backed, etc.) with at least a year to maturity:

Image source: Janus Capital Group.

The regularity of the upward trend managed to surprise even a bond market veteran like Gross:

Stocks are more complicated, of course. Returns over the same period have been excellent, but the ride was less comfortable:

Image source: Janus Capital Group.

"...a grey if not black swan that cannot be repeated."

Gross puts the two together and comes to an uncomfortable conclusion:

Is Bill correct? In the case of bonds, almost certainly. Unless you expect interest rates to go deep into negative territory (or that the U.S. will experience massive deflation), the long decline of yields over the past four decades is a tailwind that will be impossible to reproduce.

For stocks, the range of possible outcomes is much wider. Nevertheless, over the four decades to the end of May 2016, the S&P 500 produced an annualized total return (with dividends reinvested) of 11.1%, which is 1.1 percentage points over the annual average over the past 90 years -- not an insignificant difference.

Just as bonds benefited from the headwind of falling interest rates, stock returns were juiced by rising valuations. Between June 1976 and May 2016, the S&P 500's cyclically adjusted price-to-earnings multiple, which uses a 10-year trailing average of earnings, more than doubled, from 10.5 to 26.1. We are unlikely to see that happen over the next 10, 20 or 40 years (in its 135-year history, the cyclically adjusted P/E has only ever exceeded 40 in 1999 and 2000).

Here's how investors can prepare for lower returns

If Bill is right, and stock and bonds are likely to be appreciably lower over the next four decades, what should investors do about it? You have no control over the returns stocks or bonds will deliver, but there are some things within your control:

- If you have (good) reason to believe you can select fund managers that will outperform over extended periods, that's one means of earning an incremental return.

- Because most investors aren't able to select superior money managers, your best choice is likely to be minimizing your costs by investing regularly in the lowest-cost index funds (personally, I think Vanguard is first-rate).

- There's another variable over which you have some measure of control: Your saving rate. Increasing the amount of money you invest on a regular basis will go some way toward compensating for sub-par returns.

Finally, although this has nothing to do with investing per se, I would recommend to permanently be looking for ways to improve and expand your job skills, i.e., fortifying the competitive moat that protects and enriches the company that matters most: Me, Inc.

The article 2 Graphs Show Investors Won't Benefit From This "Black Swan" Again originally appeared on Fool.com.

Alex Dumortier, CFA, has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.