13-Point Checklist for Buying a Biotech Stock

Gaining an exclusive license to sell a life-changing -- sometimes lifesaving -- drug creates an opportunity even the greenest investor can understand. This is part of why thebiotechnology industry is rife with optimism, from both management and investors. Unfortunately, though, that optimism is often blind, and in the volatile world of biotech, one disappointing press release can lead to tremendous losses if you're not careful.

If you're looking for advice to make quick gains from trading around market catalysts, I'm afraid this is the wrong place. However, if you're considering buying biotech stocks as long-term investments, this checklist will help you identify encouraging signs, while avoiding common mistakes.

1. Check if the company is out of the clinical stage

A majority of the biotech industry's smaller members are in the clinical stage. In other words, they don't have a product to sell yet, but they're testing potential drugs in humans. They are extremely risky, and volatile. Less-than-positive results from an important clinical trial can result in heavy losses that might be temporary, but still present a great deal of risk.

For example,bluebird biomay have potential curesfor some devastating diseases, but its stock was beaten up after posting less-than-positive data from a very small clinical trial last year.Celldex Therapeutics shares were hammered when one of several promising candidates failed a clinical trial, even though its other candidates look very promising.

While I think these two stocks will turn around and provide fantastic gains in the long run, their future is uncertain. Human physiology can be surprisingly uncooperative and leave you with long-term losses. So, if you're interested in sleeping well at night, it may be best to stick to commercial-stage companies with proven products on the market.

2. Remember that commercial-stage companies are still risky

The vast majority of commercial-stage biotech companies (i.e. those with one or more approved products) are "growth" stocks. That's finance jargon for shoveling every penny of profit, sometimes more, back into their operations. This isn't necessarily bad, but a few wrong turns from management, and you could end up stuck with long-term losses.

For example, Vertex Pharmaceuticals recently announced a record-breaking first quarter, reporting $398.1 million in revenue. About $255.8 spent on R&D was its single largest expense, but the company still produced a net loss of over $41 million in the first quarter.

Vertex sells the only approved drugs that treat the root cause of cystic fibrosis, and this year's top line is expected to be over 70% higher than last year's.At a recent price of about 12 times this year's sales estimates, the slightest indication Vertex can't continue to expand sales, and eventually profits, at a phenomenal rate in the years ahead could lead to a stock market hammering.

PartnersAbbVie andGalapagosare hard at work to introduce some competition. The odds are long, but if this team, or any others, pressure Vertex's sales, the stock could remain depressed.

3. When buying biotech stocks, checkyour risk tolerance

An investor in his or her twenties without dependents can afford to take risks most fifty-somethings can't. Unfortunately appetites for risk often outweigh tolerances. I've seen too many investors lose more than they can afford to on biotech stocks; please don't become another.

The good news is that a handful of biotechs generate cash flows that outweigh their R&D reinvestment opportunities, which is a good indicator of a biotech's stability. Companies likeAmgenandGilead Sciencesare so well established that they're paying dividends and buying back shares. Even if your risk tolerance is practically zero -- a category I fit in -- evenJohnson & Johnsonprovidessomeexposure to the biotech industry.

Again, nothing is certain. However, your chances of suffering long-term losses with a company generating plenty of moneyandreturning profits to shareholders are much lower than with any of the previously mentioned stocks.

Now that you know the difference between clinical- and commercial-stage biotechs, and the inherent risks that come with them, let's dive into some less obvious hazards.

4. Check whether your biotech stock has all its eggs in one basket

Drug development expenses rise exponentially as clinical-stage drugs get closer to the FDA approval finish line. For this reason, it's not unusual for a clinical-stage company to devote a majority of its limited resources to the candidate with the best chance of crossing that line.

What you want to avoid are companies without any backup programs. For example,Puma Biotechnology is entirely devoted to development of neratinib for treatment of certain forms of breast cancer.

Over the past couple years the market has become less optimistic about that drug's future. When the FDA requested a change in the statistical analysis in March, the stock was subsequently hammered, again. Puma Biotechnology still plans to file an application for a limited breast cancer indication sometime this year. If it doesn't earn an approval, and impress oncologists, shareholders might never recover from the crushing losses.

5. Check for interest from bigger players

Unlike Puma Biotechnology,Ionis Pharmaceuticals discovers new drug candidates internally, and lots of them. Discovery is relatively easy, but moving drugs through clinical stages requires more resources than most biotechs have available.

Luckily, plenty of bigger companies are willing to fund development of Ionis' candidates for share of potential sales. Last the biotech racked up $283 million in total revenue without making any sales of its ownIthas so many collaborations with bigger drugmakers that I couldn't list them here without breaking the Internet.

In the years ahead, if its late-stage drugs begin earning sales, and the royalty checks start rolling in, Ionis will probably quit out-licensing the drugs it discovers and begin developing them with its own resources. This could lead to big gains for patient investors.

We've seen this story before: Over 20 years ago,Biogenlet Roche help it develop what eventually became Rituxan and Gazyva. Last year Biogen's share ofRituxan's and Gazyva's operating profits totaled $1.3 billion, and Biogen has effectively used those cash flows to develop its own drugs to great success.Biogen shareholders who held on since the beginning of that partnership have enjoyed astronomical gains, beating theS&P 500 by miles.

6. Avoid clinical-stage biotechs with big pipelines and no partners

Now that you've seen what can happen in the long run when biotechs which are discovering new drug candidates form partnerships, let's look at what happens when they don't.

Image source: Anavex Life Sciences.

Anavex Life Sciences has a burgeoning pre-clinical pipeline. It's also in preparation for a phase 2/3 trial with 2-73, its lead candidate for treatment of Alzheimer's disease. If 2-73 succeeds, it could become one of the best-selling drugs of all time, but Anavex investors have watched their share of any profits the company might generate dwindle: Without a partner, the company must fund its program with equity. Adjusting for the 4-for-1 share consolidation ahead of its uplisting to the Nasdaq exchange last October,the number of outstanding shares has risen 373% over the past two years, from 9.57 million at the end of March 2014 to 35.70 million at the end of this March.

Suppose you bought four shares of Anavex two years ago. Also imagine a partner swoops in today and funds development of its pipeline, and the company stops diluting shares from this point forward. If it produced a $9.57 million profit at some point in the future instead of reporting earnings of $1 per share, Anavex would report just $0.27 per share.

The company is authorized to sell a lot more stock, and investors who have been hanging on over the past several years will probably see their share of any potential profits dwindle much further.

7. Check the ratio of upfront cash to biobucks

The term "biobucks" is industry jargon forpotentialpayouts if drugs pass regulatory and commercial milestones. If you're thinking of buying a biotech stock because the company just announced a billion-dollar deal, look at how much the larger company offered upfront. The deal may entail delayed payments that are tied to developmental or commercial milestones in addition to an upfront payment. Generally a bigger initial payment signifies confidence, or even multiple bidders.

Not all partnership and licensing deals are the same, and the devil's in the details. For example, blue-chip biotechCelgene's 10% equity stake in Juno Therapeutics,combined with $150 million upfront, signifies a strong belief in Juno's potential.

A $10 million upfront payment to a new biotech with an interesting drug development platform to discover multiple new drug candidates, each worth potentially hundreds of millions in biobucks, is hardly worth a press release, but it usually results in one -- which brings us to the next point on our checklist.

8. Check the ratio ofpress releases to clinical trials

Touting minor developments isn't necessarily bad, but it should raise yellow flags when you think about buying biotech stocks. This could be the result of an over-caffeinated employee in the media relations office -- or it could be a sign the company is building a house of cards.

A quick way to decide if a biotech company is actually doing something worthwhile is to search the ClinicalTrials.gov database for the company's name. If it's sponsoring plenty of active trials, those press releases might indeed be worthwhile.

9. Check press releases against info in the ClinicalTrials.gov database

All trials have primary and secondary endpoints. Without a doubt, the primary endpoint is the most important one and the one that reflects the most important question being asked in a trial. Secondary endpoints are relevant, but to a much lesser extent. Sometimes a biotech will play up success related to a bunch of secondary endpoints, while burying the fact it didn't do so great at meeting the trial's main goal.

If the results you read in press releases don't jive with the official description of the trial, it could signify trouble.

10. Be encouraged by control groups in early stage trials

A control group is science-geek jargon for the people getting either the placebo or the current standard of care for their disease, rather than the experimental drug. Be extremely wary of biotechs touting positive efficacy results from trials without control groups.

Image source: Inotek Pharmaceuticals Corporation.

Phase 1 and phase 2 trials don't require control groups because they're testing for safety and determining an effective dosage, respectively. However, be encouraged when a biotech is willing to include a control group in early trials, because it's a big pain in the rear.

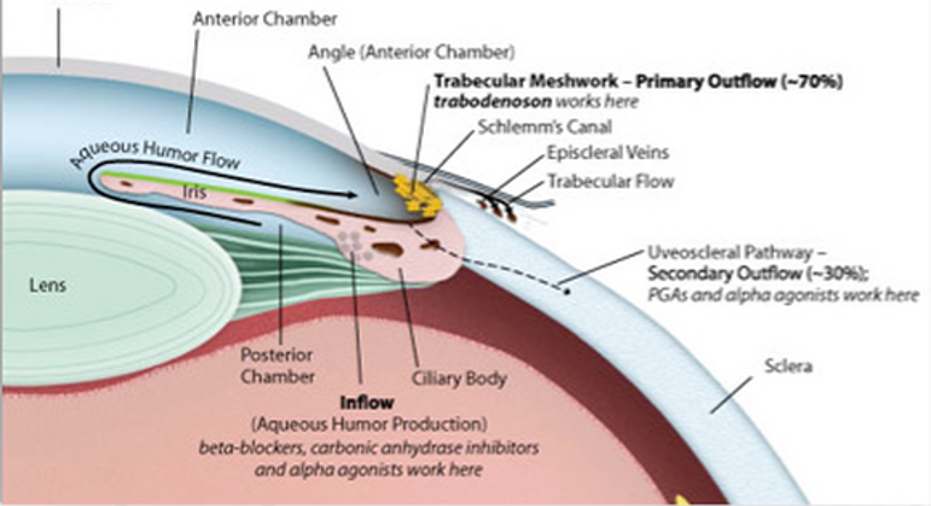

In the case ofInotek's recent phase 2 dose escalation trial with trabodenoson for treatment of glaucoma, it went through the trouble of hiring an outside group of professionals to create a placebo, and keep it a secret. If trabodenoson drops don't sting, or have any smell, or color, the placebo could simply be saline. More often than not, creating an acceptable placebo can delay trials for months, and at no small expense.

However, Inotek made the extra effort, and it paid off: One of the higher doses of trabodenoson was significantly more effective than placebo. Now the company can fund a bigger, far more expensive phase 3 trial with confidence, and its shareholders can rest easier.

Conversely, be wary if a company is willing to run a long trial, especially a phase 2, without a control group. It could signify management's lack of confidence in its candidate.

11. Check for statistical significance

Beginning biotech investors and a shocking number of scientists tend to forget that statistics are an attempt to predict what will happen in the real world, using a limited amount of available data. With respect to a drug's efficacy against a placebo, or the existing standard treatment, it's all about the p-value.

While a p-value of 0.05 is generally considered significant, it's important to understand this figure in the context of efficacy results. A p-value of exactly 0.05 means that the odds that chance accounted for the results are just 5 out of 100. Clearly, the lower the p-value, the better.

Recall our earlier definition of primary versus secondary endpoints. If you see a company touting a secondary efficacy outcome result with a p-value of 0.048, get nervous. When you see primary efficacy outcome-related p-values with several zeros on the right of the decimal point, get excited.

12. Remember FDA meetings and letters are not subject to full disclosure

The divisions of the FDA that deal with biotechs do not behave like any government agencies I'm familiar with. When consulting with companies in preparation for trials intended to support drug applications, the FDA is generally clear about what it wants to see. It's not uncommon for biotechs to ignore the Agency's recommendations in attempts to save time and money.

New drug applications are rarely rejected outright; instead, biotechs usually receive "complete response" letters, or CRL. They basically contain a list of things the FDA wanted, but didn't get. CRLs aren't necessarily a new drug's death sentence, but they usually are.

Most importantly, their contents are confidential. The biotech might disclose minor parts, such as: "There were concerns about the manufacturing process. We've already sorted it out and we'll resubmit in the first half of next year."

That could be the extent of the letter's contents. Generally, it's what biotechs don't disclose that leave you with long-term losses.

13. Check for pooled data analyses

After a trial fails to meet its primary endpoint, biotechs large and small are often unwilling to admit defeat. One of the most common last ditch efforts to save a program is to combine or "pool" data from separate trials and find a group that benefited. While this may be a reason to run another trial specific to the group that benefited, consider attempts to submit new drug applications based on pooled data analyses failures waiting to happen.

A stunning example of such behavior came from PTC Therapeutics. Last October the company announced its lead candidate, ataluren, for treatment of Duchenne muscular dystrophy, failed to meet its primary endpoint, improvement in distance patients were able to walk in six minutes after 48 weeks.

When PTC therapeutics announced the failure last October, it quickly pointed to promising data from a "pre-specified population" in the phase 3 study, pooled with patients from an earlier phase 2b trial. Although the clinical trial protocol screened specifically for patients able to walk 150 or more meters at the beginning of treatment,PTC Therapeutics noted that a pooled group of patients that began the phase 2b and phase 3 study able to walk between 300 meters and 400 meters in the six-minute test showed a statistically significant improvement after 48 weeks.

If the company had met with the FDA about running another registrational trial specific to this group of patients, that would have been a setback, but perhaps worth the effort. Instead PTC Therapeutics submitted an application for approval of the drug this January on the pooled data alone,and the FDA refused to file it in late February.

Anyone familiar with the FDA's stance on similar post hoc analyses would have known the application was doomed, but it took Wall Street by surprise:

This won't be the last time a company tries this tactic, but hopefully the next time something like this happens, you'll be ready.

If you've checked the biotech stocks you intend to buy against all these points, congratulations! You're no longer a rookie. In fact, you'll probably outperform most Wall Street biotech fund managers.

{%sfr}

The article 13-Point Checklist for Buying a Biotech Stock originally appeared on Fool.com.

Cory Renauer owns shares of Johnson & Johnson. You can follow Cory on Twitter@TMFang4applesor connect with him onLinkedInfor more healthcare industry insight.The Motley Fool owns shares of and recommends BioMarin Pharmaceutical, Celgene, Gilead Sciences, Ionis Pharmaceuticals, Johnson & Johnson, and Vertex Pharmaceuticals. The Motley Fool recommends Biogen, Bluebird Bio, Celldex Therapeutics, Juno Therapeutics, and Seattle Genetics. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.