3 Charts from Wells Fargo's 2016 Investor Day That Caught My Eye

At Wells Fargo's investor day this week, the bank's executives covered a lot of ground, though its CFO's presentation in particular caught my eye. Three charts in it go a long way toward explaining why Wells Fargo is known to be the best-run big bank in the country.

1. Revenue

Wells Fargo prides itself on its efficiency. Its 2015 efficiency ratio, which measures the percentage of the bank's net revenue consumed last year by operating expenses, was 58.7%. This is at the high end of its target range of 55% to 59%, but it's below the 60% threshold that most banks strive to achieve.

Even though most conversations about the efficiency ratio focus on expenses, one reason Wells Fargo's is so low is because the bank generates more revenue from its operations than most of its peers do. This matters because a bank's revenue is the numerator in the efficiency ratio calculation.

Data source: Wells Fargo. Chart by author.

Of the nation's six biggest banks, only Wells Fargo and U.S. Bancorpgrew their top lines over the past two years. Both increased by 5%. On the other end of the spectrum is Bank of America , which saw its revenue drop by 7% over the same stretch.

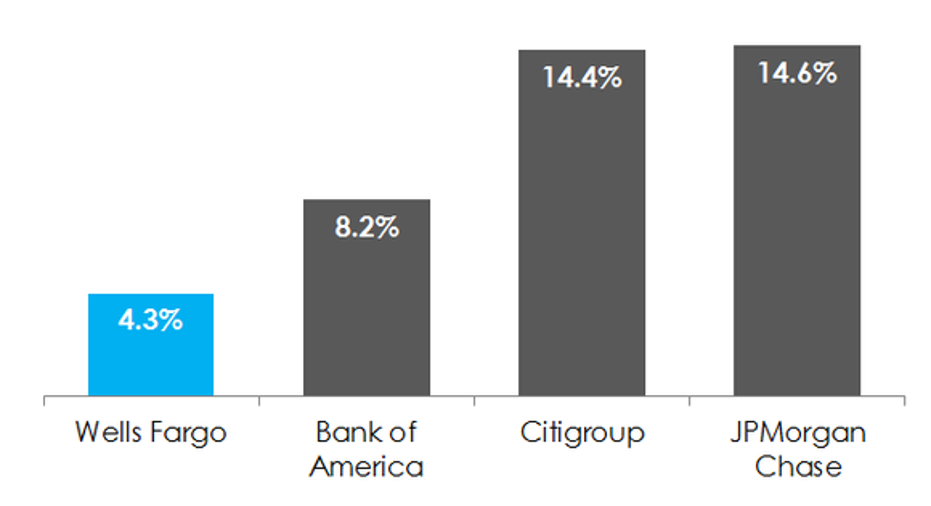

2. Trading assets

Wells Fargo's shares consistently trade at a higher multiple of book value than banks like JPMorgan Chase , Bank of America, and Citigroup . Why is this? Beside the fact that Wells Fargo is more profitable than its competitors, it's also a safer stock to own.

You can get a sense for this by comparing the size of these banks' trading operations, which are the riskiest and most volatile part of a bank's business. Wells Fargo's trading assets equate to only 4.3% of its total assets. That compares to 8.2% at Bank of America and more than 14% at both JPMorgan Chase and Citigroup.

Data source: Wells Fargo. Chart by author.

Wells Fargo's minimal exposure to the capital markets insulates it from the type of loss that JPMorgan Chase suffered in 2012. Thanks to a wrong way bet on derivatives tied to the price of corporate bonds, the nation's biggest bank by assets lost over $6 billion in one fell swoop.

3. Capital return

There are two main benefits that flow from Wells Fargo's ability to generate more revenue than its peers and to do so with less risk. First, its stock tends to perform better than other big banks. And second, Wells Fargo is able to distribute a larger share of its earnings each year to shareholders.

Since the financial crisis, banks with more than $50 billion in assets on their balance sheets must request approval from the Federal Reserve before raising their dividends. This is why Bank of America and Citigroup have only boosted their dividends once since the crisis, while JPMorgan Chase and Wells Fargo have been able to do so almost every year.

This comes through loud and clear in the following chart, which shows how much capital the nation's six biggest banks have returned to shareholders via dividends and buybacks over the past 24 months. Suffice it to say that Wells Fargo has handily outperformed its peers on this front.

Data source: Wells Fargo. Chart by author.

In short, it would take a much longer article to cover everything that allows Wells Fargo to separate itself from the pack. But these three points go a long way in this regard.

The article 3 Charts from Wells Fargo's 2016 Investor Day That Caught My Eye originally appeared on Fool.com.

John Maxfield owns shares of Bank of America, US Bancorp, and Wells Fargo. The Motley Fool owns shares of and recommends Wells Fargo. The Motley Fool recommends Bank of America. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.