It Would Be Dumb To Ignore These 5 Social Security Facts

Image source: Flickr user Garry Knight

Social Security is a critical source of retirement income for tens of millions of Americans, but Social Security's future could be at risk if Washington fails to take action. Social Security payments to recipients have been outstripping payroll tax revenue since 2010 and that means that every month that goes by puts the program one-step closer to running the Social Security Trust Fund dry. Given that risk, it's more important to learn as much about this valuable program than ever before. So, with that in mind, here are five facts about Social Security's solvency and its future.

Fact No. 1: Critical safety net

According to the Social Security Administration, a significant number of Social Security recipients count on Social Security checks to pay their monthly expenses.

Specifically, more than half of married couples and nearly three-quarters of unmarried Americans get more than 50% of their retirement income from the program. More worrisome is that almost half of unmarried recipients rely on Social Security for more than 90% of their retirement income.

With millions of seniors relying so heavily on Social Security to cover daily living expenses, it's not surprising that theCenter on Budget and Policy Prioritiesestimates 15 million elderly Americans would fall below the poverty line if Social Security were to disappear.

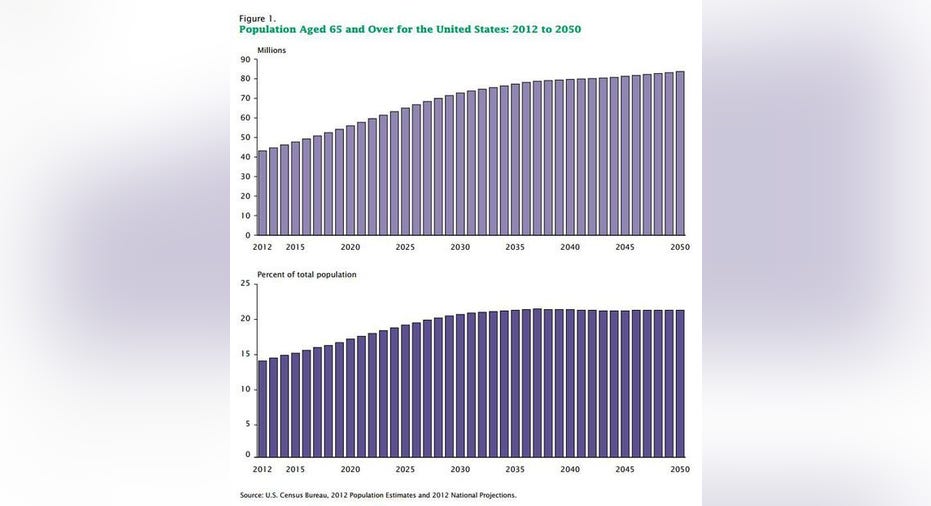

Fact No. 2: Social Security spending set to soar

76.4 million Americans were born between 1946 and 1964 and 10,000 of these baby boomers will turn 65 every day until 2029.

As a result, the number of people collecting Social Security is expected to skyrocket, sending Social Security outlays over the coming decade soaring.

Fact No. 3: Running out of money

The Social Security's Trustees predict that payments to recipients will exceed payroll taxes by about $76 billion annually through 2018, before rising steeply in the years after that.

Because the gap between tax revenue and Social Security payments will widen, more money will need to be withdrawn from the Social Security Trust Fund to make up the difference. According to a Congressional Budget Office report in December, making up for the shortfall will deplete the Trust Fund in 2029.

Fact No. 4: Benefit cuts on the horizon

The Congressional Budget Office projects that Social Security outlays will exceed tax revenue by "almost 30% in 2025 and by more than 40% in 2040." Obviously, that's untenable.

The depletion of the Social Security Trust Fund will require an across the board 29% cut to Social Security benefits beginning in 2029. That's because Social Security can't borrow money to make up the the difference. The only way that a benefit cut to Social Security can be avoided is if changes are made that either increase tax revenue or reduce Social Security's outlays. If Washington fails to make a proactive decision on this matter, then the mandated cuts will kick in.

Image Source: BernieSanders.com

Fact No. 5: Solutions are imperfect, but necessary

Cuts to benefits in 2030 could be avoided if Congress acts to protect Social Security, but proposals to sure-up Social Security are admittedly less than ideal. Among the most commonly proposed solutions are:

- Increasing the income cap on the payroll tax.

- Increasing the full retirement age.

- Changing how annual increases are calculated.

- And, instituting means testing to reduce payments to the wealthy.

Currently, the 12.4% payroll tax is split equally between employees and employers and assessed on income of up to $118,500. Both Hillary Clinton and Bernie Sanders recommend a tax holiday on income between $118,500 and $200,000 or $250,000, respectively. Any income above those levels, however, would be taxed at the 12.4% rate.

The full retirement age, or the age at which you qualify for 100% of your Social Security benefit, is currently 67 for people born after 1960. Increasing the age for people born more recently than that to 70, for example,could reduce the number of people receiving benefits and thus, lower outlays. Since American's average life expectancy is climbing, this option may make sense if it's phased in slowly. After all, as the following table illustrates, there's a precedent for increasing the full retirement age.

Annual increases to Social Security benefits are based on the consumer price index, or CPI. However, CPI isn't the only inflation measure that could be used. Chained-CPI takes into consideration the fact that buying patterns change as the cost of goods increases. As a result, chained-CPI has historically grown more slowly than traditional CPI and therefore, using it could slow Social Security spending.

Finally, means testing income has been floated as an option because it shifts Social Security payments to those who need it most from those who need it least. That could preserve the program longer, without requiring changes to the tax code, or adjusting retirement ages upward -- both of which could increase the financial pressure on low- and middle-income families. That being said, moving the goalposts on people who have already paid into the system and expect benefits is arguably unfair.

Taking control

These facts all point to a need for future retirees to focus more on creating other sources of retirement income than Social Security. However, too few Americans are taking the action necessary to stockpile money for their retirement, such as maxing out tax-advantaged retirement savings accounts, such as 401(k)s. If you're among them, now is a good time to start making the most of them. Even if you can't contribute the maximum to an employer sponsored plan (people can contribute $18,000 to their 401(k) plan in 2016, plus another $6,000 catch-up contribution if over age 50), consider bumping up the percentage contribution by 1% to 2% every year until you are maxed out. Making small changes now can really pay off in retirement thanks to compound interest, or the ability of returns to earn returns over time.

The article It Would Be Dumb To Ignore These 5 Social Security Facts originally appeared on Fool.com.

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.