Canadian National Railway (USA) Is Just Better at Moving Goods More Cheaply

Few railroads move goods more efficiently than CN. That's helped it grow profits, even as volumes have slipped.

During the past year-plus, investors have heard a near-constant refrain fromCanadian National Railway (USA): Weak energy and metals/minerals shipments have seen total volumes fall, though strong auto demand and housing construction in the U.S. have balanced that with increased shipments of vehicles and forest products. At the same time, however, CN has done an excellent job of managing its costs, and continues to report the best efficiency in the rail industry, helping it continue to grow profits, even as the issues above reduce volumes and revenues.

Let's take a closer look at Canadian National Railway's first-quarter financial results. (Note: All dollar amounts in this article reported in Canadian dollars.)

The numbers

| Metric | Q1 2016 | Q1 2015 | Change |

|---|---|---|---|

| Revenue | $2,964 | $3,098 | -4% |

| Net income | $792 | $704 | 13% |

| EPS | $1.00 | $0.86 | 16% |

| Operating ratio | 58.9% | 65.7% | 680 BPS improvement |

Revenue and net income in millions. Source: Canadian National Railway.

CN isn't the only railroad feeling the pinch of weak energy volumes. CSX Corporation reported earnings in mid-April, and its revenues declined 14% on a 5% decline in volume and lower fuel recovery. CSX reduced its expenses by 12% in the quarter, but the continued weakness -- particularly in shipping demand for coal, metals, and other commodity goods -- is expected to continue weighing on the company's volumes. CSX reported an 18% decline in earnings per share in the quarter.

CN, which recognizes its results in Canadian dollars, gets some benefit from a strong U.S. dollar, though much of this benefit is canceled out by operating expenses, which are also in U.S. dollars for all of its operations south of the Canadian border. At the same time, the company's ability to manage its costs, and consistently improve its already-excellent operating performance, has been a key and sustainable benefit to the bottom line.

Keys to the quarter

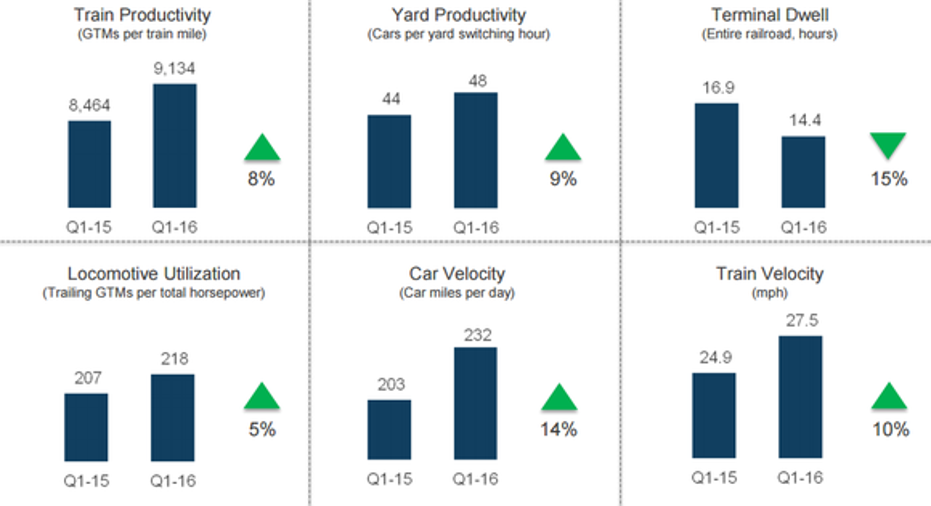

This slide from CN's earnings presentation sums up the operating-efficiency gains the company got last quarter:

Image source: Canadian National presentation.

In short, the railway moved goods more quickly, moved more cars through its yards in less time, and hauled more goods per horsepower utilized in the quarter. Add these all up, and that's more goods moved per dollar of cost, whether it's labor, fuel, or assets being utilized.

Another slide, which showed how the weaker Canadian dollar, as well as higher prices, helped drive a higher revenue per rail-ton-mile shipped, combined with the better ratios above to increase earnings:

Image source: Canadian National presentation.

The slide also shows, on the right, the volumes shipped by category. The importance here is that CN's relatively diverse mix of products that it ships allows the company to ride out weakness in one or more industries, while still maintaining highly efficient operations and solid profits.

Key comments from management

The weak Canadian dollar, as compared to the U.S. dollar, is helping CN in more than one way. Two statements from Chief Marketing Officer Jean-Jacques Ruest:

The company's relatively small exposure to coal is a big benefit, particularly as competitors such as CSX, with larger dependence on coal, will be challenged to find replacement volume:

CFO Luc Jobin pointed out that a weak Canadian dollar did help earnings, but it was far from the only source of earnings growth:

Back out that $0.07 per-share benefit, and EPS still increased 8% year over year. Factor out the 3% reduction in the share count from buybacks, and that's still a 5% boost in profits from improved operations, even on lower volume and revenue.

Looking ahead

When management gave guidance for 2016 on its fiscal 2015 earnings call, the expectation was for earnings per share to grow at a mid-single-digit rate. However, a number of factors, including a higher fuel price and foreign exchange assumptions, led the company to revise its guidance down, with the goal of delivering $4.44 per share in earnings in 2016. That would be the same as the railroad produced last year. In short, net income could decline as the year progresses, as share buybacks are likely to further reduce the share count.

At the same time, the board approved a 20% increase to the dividend earlier this year, to $1.50 per year, paid quarterly. At the projected $4.44 per share in earnings, that's roughly a 33% payout ratio, slightly below the target of 35%. In other words, if the company can exceed its earnings guidance in 2016, and if management can sustain that growth, further dividend increases that track with earnings growth each year are likely.

Image source: Canadian National Railway.

The article Canadian National Railway (USA) Is Just Better at Moving Goods More Cheaply originally appeared on Fool.com.

Jason Hall has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Canadian National Railway. The Motley Fool recommends CSX. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.