3 Things American Express Investors Should Worry About

American Express lost deals with Fidelityand Costco. It could soon face a challenge in keeping Starwood. But where all these headline-grabbing losses are important for American Express, it's important to recognize they're the symptom of much larger issues.

American Express is facing more competition from three major sources.

Banks are coming!By far the worst competitor for American Express is the traditional bank. The reason for it is simple: Banks are happy with low returns, and can achieve adequate (read: low) returns by working with Visa and MasterCard to bid on deals in an effort to attract credit card loan balances. American Express wants much higher returns, repeating time and time again that it has a 25% return on equity target for any deal.

It's not hard to see why, then, American Express is losing so many co-brand partnerships.

Take, for example, Citi, which recently partnered with Visa to take over the Costco partnership from American Express. Any deal that exceeds Citi's6-year average return on equity of less than 6% is essentially good enough to pursue. A single-digit ROE isn't ideal, but that's effectively Citi's hurdle -- anything more than what it is earning on its entire book right now is an improvement.

It's an unfortunately reality that AmEx's most capable and biggest competitors are earning single-digit returns in traditional banking. Lower interest rates push banks into high-net interest margin products like credit cards. Irrational competitors are a commodity business's worst nightmare.

Where's the upsell?Pressures go behind the obvious. Where American Express is a card business -- and pretty much only a card business -- the banks offer a full suite of products. Bank card customers can be theoretically upsold on bank accounts, car loans, mortgages, and asset management services. American Express can...well, issue you another credit card, and maybe sell you on a checking or savings account, but that's about it.

The customers and customer data generated from co-brand deals is fleeting. Card companies have to turn co-brand customers into their own customers, and do it quickly, or risk losing them entirely on the next contract renewal.

On the most recent conference call, American Express's CFO, Jeffrey Campbell, said that the company is pushing new cards to existing members "under a series of contractual restrictions about how we can market to Costco co-brand Card Members."

He added that "once the sale happens in mid-June, those Card Members will no longer be known to us, and they will be customers of one of our competitors. So that should produce a very different result." In my mind, banks with bigger product lines seem much more capable of extracting value from co-brand relationships.

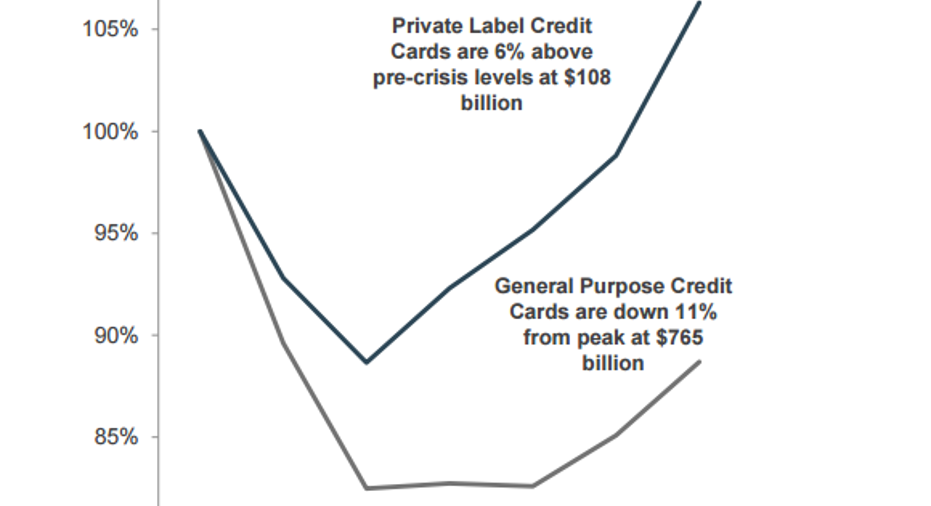

An industrywide shiftFinally, it's important to remember that the traditional general purpose or co-brand card are not the only card in the game. Increasingly, businesses are using private-label cards to reduce merchant fees, and improve on their ability to market to their customers.

Private-label issuer Synchrony Financial routinely touts the growth in private-label cards vs. so-called general purpose credit cards (traditional credit cards). Tellingly, private-label cards have been the primary driver of credit card balances since the financial crisis.

Private-label cards are store-specific cards that enable customers to run up a balance at just one store. But they're a highly competitive choice for retailers (who can avoid the fees on each swipe), and collect very valuable data about their customers.

A private-label card enables retailers to know exactly which pair of shoes you purchased, in which size, at what time, and whether you bought online or in store, for example. All that data allows a retailer to more effectively market to their most loyal customers. It's no surprise that these cares are becoming more popular.

Note, however, that private-label cards are the anti-thesis to a "spend-centric" model like American Express. There are no fees to collect on each swipe, and balances are typically much smaller due to single-store use and smaller credit limits.

Companies like Synchrony hope to make their money by charging interest on small balances that are carried over from month to month, in contrast to AmEx, which has built a business on the idea that the best income is made on swipes, not lending.

The article 3 Things American Express Investors Should Worry About originally appeared on Fool.com.

Jordan Wathen has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Costco Wholesale, MasterCard, and Visa. The Motley Fool recommends American Express. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.