Is Social Security Breakeven Analysis Fundamentally Flawed?

One of the most important decisions you'll make in your financial life is figuring out when to start taking Social Security benefits. A lot of people who examine the nuances of this decision use a technique known as breakeven analysis, in which they look at when a decision to wait to claim to get largely monthly payments will "catch up" with those who claim earlier and get smaller monthly payments for a longer period of time. Yet in doing this analysis, most policymakers pay little attention to the time value of money, and that can shift the argument toward the direction of claiming earlier rather than later.

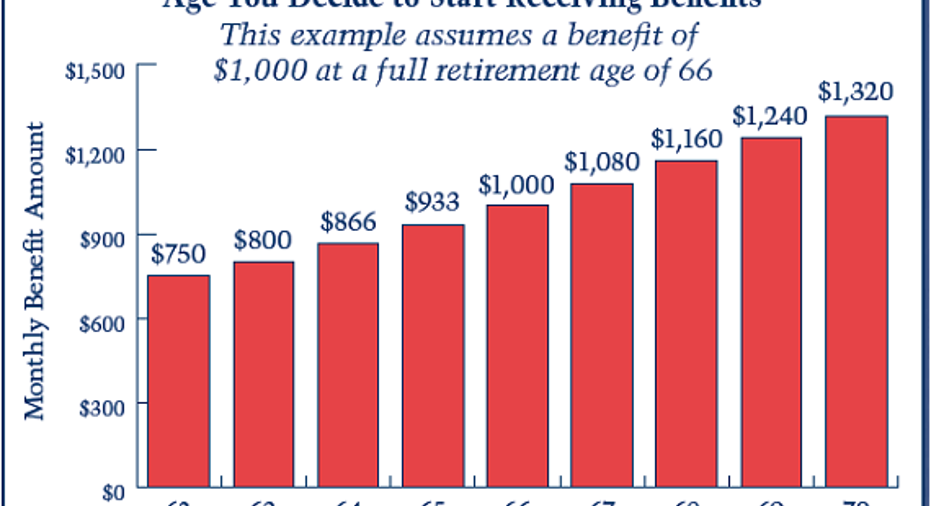

The basics of breakeven analysis To understand breakeven analysis, you first have to know the rules for Social Security payments. Currently, full retirement age is 66, and the calculations that the Social Security Administration does to figure your benefits start out by assuming that you'll start taking benefits then. If you decide to wait longer, then you can get delayed retirement credits that will add 8% to your monthly check for every year you decide to wait. If you take early benefits, you'll take a haircut of up to 25% on your benefits. The chart below gives you a sense of the resulting spread of potential monthly checks from your decision of when to claim benefits.

Image: SSA.

With this in hand, it's easy to figure out when the total dollar amounts for any two given Social Security claiming choices will be equal. For instance, in comparing claiming at 62 with claiming at 66 for someone with a base benefit of $1,000, the early claimer will get four extra years of monthly payments of $750. That adds up to $36,000. Once they hit age 66, the late claimer will get an extra $250 per month. Divide $36,000 by $250, and you get 144 months, or 12 years. That means the breakeven date is age 78 -- 12 years after the late claimer starts getting benefits.

You can see the general comparison of claiming at 62, 66, or 70 in the chart below. In general, though, standard breakeven analysis gives results that are in the late 70s or early 80s.

Image: Author.

Ignoring time valueHowever, the standard breakeven analysis makes a simple mistake: it ignores the time value of money. Specifically, the extra $250 that someone collects starting four years into the future is worth less than $250 would be worth today. Applying that discount to future payments shifts the balance toward taking smaller payments sooner.

For instance, the following chart assigns a 5% return to the money you receive from Social Security. If you have retirement assets that you've saved, then you can think of this rate as being your expected return on investing those assets.

Image: Author.

As you can see, adding even a modest return assumption dramatically increases the breakeven date. Comparing filing at 62 and filing at 66, the late filer doesn't catch up to the early filer until they reach their late 80s. Other strategies have breakeven dates into the 90s.

Should you not use breakeven analysis?It's tempting to conclude that breakeven analysis is fundamentally flawed, but the real answer is more complicated than that. Whenever you do a financial analysis, you have to make assumptions. The assumption underlying the traditional breakeven analysis is that you will immediately spend the money, and so time value is of minimal importance as long as you have enough to make ends meet. If you don't have the luxury of investing your Social Security money and don't have savings that you can draw down on while you wait to claim Social Security later, then building a return assumption into your Social Security decision-making analysis doesn't make sense.

However, for many people, earning a return through savings will be an option. For them, using time value as a component of a breakeven analysis makes sense, and it can lead to a more realistic picture of how things are likely to play out. It won't take everything into account, such as the impact that when you claim has on the survivor benefits your spouse will receive after your death. But the more authenticity you can build into a breakeven analysis, the more useful it will be in determining what truly is the best strategy you can follow in claiming Social Security.

The article Is Social Security Breakeven Analysis Fundamentally Flawed? originally appeared on Fool.com.

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.