Can Bank of America and Merrill Lynch Afford to Stay Together?

Image source: iStock/Thinkstock.

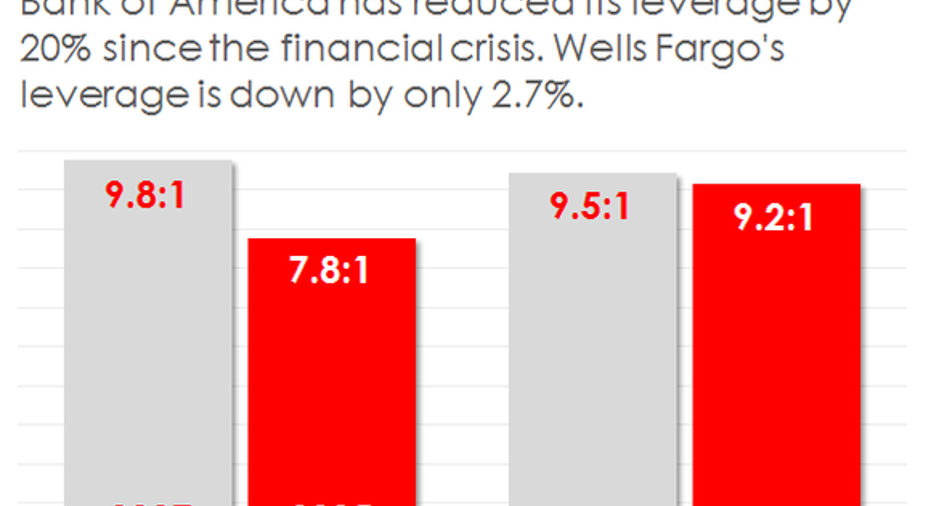

The more you dig into Bank of America's numbers, the more you come away thinking that its shotgun marriage eight years agoto Merrill Lynch can't last. This is particularly apparent when you consider how much Bank of America has had to deleverage since the financial crisis relative to Wells Fargo .

In 2007, Bank of America was leveraged by a factor of 9.8:1. For every $1 worth of common stockholders' equity, the North Carolina-based bank owned $9.80 worth of earning assets. Fast forward to today, and its leverage has fallen to 7.8:1. That's still a lot of leverage relative to a nonfinancial company, but it's nevertheless 20% less than Bank of America used before the crisis.

Compare that to Wells Fargo. In 2007, the California-based bank was leveraged by a factor of 9.5:1. Today, the figure is 9.2:1. Wells Fargo's leverage dropped, but only by 2.7%.

Data source: Bank of America and Wells Fargo. Chart by author.

The impact on Bank of America's profitability has been substantial. Holding all else equal, its return on common equity would have been 10.8% last year if it employed the same amount of leverage as it did in 2007. But because it didn't, its return on common equity was only 6.8%.

Under the former scenario, one could argue that Bank of America is creating value for shareholders because its hypothetical 10.8% return on equity is at least in the same ballpark as its cost of capital. But under the latter scenario, it's impossible to avoid the conclusion that the bank is eroding shareholder value when you factor in the risk of owning its stock, as well as the opportunity cost associated with forgoing the return from safer alternative investments.

What does Merrill Lynch have to do with any of this? In the first case, Bank of America's acquisition of Merrill Lynch increased its size, which subjects the bank to even greater regulatory scrutiny given that it's now considered a global systematically important bank, or GSIB. This alone may have had little impact, as Wells Fargo more than doubled in size as a result of its 2008 acquisition of Wachovia. But the devil is in the details.

The difference is that Wachovia, like Wells Fargo, was a commercial bank. It focused on collecting deposits and making loans. Merrill Lynch, on the other hand, is a major investment bank that plays a significant role in global capital markets. This exposes Bank of America to more risk, and increases its interconnectedness with the global financial system.

The net result is that, under the heightened regulatory and capital regime of the post-crisis period, Bank of America must hold more capital relative to its assets than Wells Fargo does. You can get a sense for this by looking at their respective GSIB buffers, which tie how much leverage a bank can use to its role in the global financial system. Bank of America's GSIB buffer is 3%, while Wells Fargo's is only 2%.

On top of this, Bank of America's capital-markets business seems to require it to maintain more liquidity than Wells Fargo. In 2014, regulators finalized two liquidity risk-related standards that tie the amount ofunencumbered high-quality liquid assets -- namely, cash and U.S. government-backed securities -- a bank must hold to the estimated net cash outflows the institution could encounter over a 30-day period of significant liquidity stress. The principal rule is known as the liquidity coverage ratio, or LCR.

There are two reasons to believe that the LCR takes an especially onerous toll on large universal banks such as Bank of America. First, as we saw with Bear Stearns during the last crisis, a bank's Wall Street operations, and particularly its prime brokerage, is often the first place that bleeds liquidity during a crisis. Second, as we saw this month with the results of the Federal Reserve's resolution plans, one of the main reasons whyJPMorgan Chase and Bank of America both failed to satisfy regulators is because of the way that they managed liquidity.

It's worth noting, moreover, that we may soon know exactly how much more stringent the liquidity requirements are for Bank of America than for Wells Fargo. This is because the Federal Reserverecently proposed a rule that would require large bank holding companies to publicly disclose, on a quarterly basis, certain quantitative and qualitative information regarding the LCR calculations.

Either way, it's clear that Bank of America operates with much more liquidity than Wells Fargo. Only 41% of its assets at the end of the first quarter consisted of loans, which are the most lucrative, but illiquid, type of asset a bank can hold. Wells Fargo, on the other hand, allocated 51% of its asset portfolio to loans last quarter. "Simplistically, the more loans to common equity [a bank holds] the higher the return on equity," observed Richard Bove of Rafferty Capital Markets in an email.

Data source: Bank of America and Wells Fargo. Chart by author.

You can see the impact of this on the amount of money the two banks generate from their income-earning assets. The annualized yield on Wells Fargo's portfolio of earning assets was 3.22% in the first quarter. Bank of America's was only 2.59%. That may seem like a negligible difference, but when you consider that Bank of America had $1.8 trillion worth of earning assets, the difference between the two figures amounts to $11 billion in annual interest income.

The point is that Bank of America's union to Merrill Lynch appears to require it to hold more capital than stand-alone commercial banks, as well as to increase the liquidity of its balance sheet. And while Merrill Lynch gives Bank of America the opportunity to cross-sell services to both consumer and commercial customers, there is little compelling evidence that the bank is particularly good at this, or that doing so will more than make up for the downside of being as big and globally interconnected as the combined institutions now are.

"Bank of America should be able to make up the return gap with contributions from Merrill's non-capital intensive operations, but it is not happening," says Bove.

None of this changes my thesis that Bank of America's shares are trading for an unconscionable discount to book value, which is why I'm bullish on its stock. But it does lead me to think differently about how the value from an investment in the $2.2 trillion bank may be unlocked in the years to come.

The article Can Bank of America and Merrill Lynch Afford to Stay Together? originally appeared on Fool.com.

John Maxfield owns shares of Bank of America and Wells Fargo. The Motley Fool owns shares of and recommends Wells Fargo. The Motley Fool has the following options: short May 2016 $52 puts on Wells Fargo. The Motley Fool recommends Bank of America. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.