What Is the Windfall Elimination Provision?

Image source: www.401kcalculator.org.

The Windfall Elimination Provision is in place to ensure the fairness of Social Security benefits to all retirees. Specifically, it provides for a different benefit calculation formula for certain retirees who also receive pensions based on work for which Social Security taxes were not withheld.

What it isThe Windfall Elimination Provision can affect your Social Security benefits if you earn a pension from an employer who didn't withhold Social Security taxes and you qualify for a Social Security benefit based on other work for which you did pay taxes. In general, this applies to certain federal, state, and local government workers, as well as employers of a nonprofit organization or people who worked in another country.

Why it's necessaryThe calculation of Social Security benefits favors lower-income workers. As of 2016, a worker's 35 highest-earning years are indexed to adjust for wage growth and are averaged. Then, the following formula is applied:

- 90% of the first $856 in monthly earnings

- 32% of monthly earnings between $856 and $5,157

- 15% of allowable earnings above this amount

So, lifetime low-income workers qualify for the highest Social Security benefits as a percentage of their earnings.

However, if a worker only paid Social Security tax on some of their earnings, they may appear to be a low-income worker when looking at their Social Security wages, when in reality that isn't the case.

How the benefit reduction worksWe mentioned that the benefit calculation formula above disproportionately favors low-income workers, and this is due to the 90% factor that applies to the first $856 of earnings. So, to compensate for the fact that certain pension recipients may not actually be low-income workers, the Windfall Elimination Provision can adjust this factor downward to as little as 40%.

The reduction amount (if any) depends on how many years of "substantial" earnings you had that were taxed for Social Security purposes. The threshold for "substantial earnings" is $22,050 for 2015 and 2016, and is indexed to compensate for inflation in previous years.

If you had 30 or more years of substantial earnings, the Windfall Elimination Provision does not apply to you, and your Social Security benefit is calculated normally using the formula listed earlier. However, if you had 29 years of substantial earnings or less, your 90% multiplier is reduced according to the following chart:

|

Years of Substantial Earnings |

Percentage |

|---|---|

|

30+ |

90% |

|

29 |

85% |

|

28 |

80% |

|

27 |

75% |

|

26 |

70% |

|

25 |

65% |

|

24 |

60% |

|

23 |

55% |

|

22 |

50% |

|

21 |

45% |

|

20 or fewer |

40% |

Data source: SSA.

The full list of annual substantial earnings thresholds can be found here(link opens PDF).Additionally, your Social Security benefit cannot be reduced by more than one-half of the amount of your pension for non-Social Security earnings, so if you have a small pension, the effect of the provision is limited.

And, the Windfall Elimination Provision does not apply if any of the following are true:

- You are a federal worker first hired after December 31, 1983.

- You were employed on December 31, 1983 by a nonprofit organization that did not withhold SS taxes from your pay at first, but then began doing so.

- Your only pension is for railroad employment.

- The non-taxed work you performed took place before 1957.

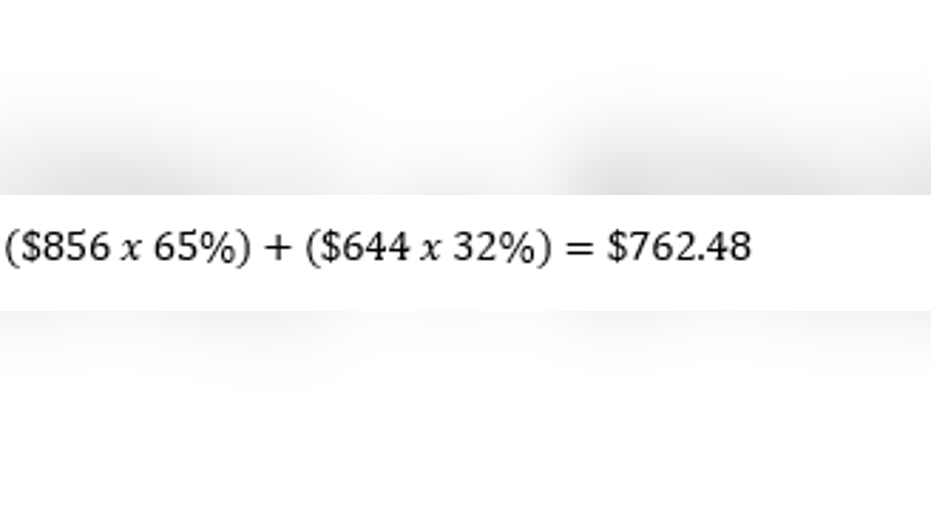

Example calculationLet's say that you reach full retirement age in 2016, and that your average Social Security wages for your career were $1,500 per month, and that you had 25 years of substantial earnings. We'll also assume that you have a $1,200 per month pension from a job where Social Security taxes were not taken.

According to the standard Social Security calculation, your benefit would be:

However, according to the Windfall Elimination Provision, your 90% multiplier is reduced to 65%, so your revised Social Security benefit is as follows:

So, your monthly Social Security benefit would be reduced by $214 per month to compensate for the fact that your pension income is based on earnings for which you didn't pay Social Security taxes.

The bottom line on the Windfall Elimination ProvisionThe Windfall Elimination Provision is designed to ensure that the payment of Social Security benefits is fair to all retirees, and does not result in disproportionately high retirement income for workers whose non-taxed earnings result in a pension. Essentially, the provision is in place to help level the Social Security playing field.

The article What Is the Windfall Elimination Provision? originally appeared on Fool.com.

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.