Berkshire Hathaway's Big Profit Center Prepares for Shrinkage

A shift in the top ranks at Berkshire Hathaway is a hint that its reinsurance businesses, historically one of its stars, is slated to shrink. The company recently announced the retirement of Tad Montross, who has led Berkshire's General Re subsidiary since 2008 after sharing the role for seven years prior. Montross's position will be filled with an unnamed executive, who will report to Ajit Jain, the head of Berkshire Hathaway Reinsurance.

Ajit Jain gets frequent praise from Buffett. It shouldn't be much more for Jain to handle, given General Re and BH Reinsurance operate in the same industry.

Last year, Buffett turned cold on the reinsurance industry. He told his investors that he expected lower returns from the industry during the next 10 years due to an influx of capital. Buffett also reduced the company's stake in Munich Re in 2015, further dialing back his exposure to the industry. In 2014, he warned about surging investor interest for catastrophe bonds, a special type of bond insurers often issue to pass on the risk of a major catastrophic event.

Highly competitive, the insurance industry ebbs and flows with its "surplus," or the amount of equity capital on insurance industry balance sheets. The greater the surplus, the more premiums that can be written.

When surplus grows too large, insurance companies that prioritize scale over underwriting profits compete aggressively on price. Insurers lose; insurance buyers win. It's an unfortunate reality that large losses, usually by catastrophe, are one of the most important factors for swinging the balance back into the favor of insurers.

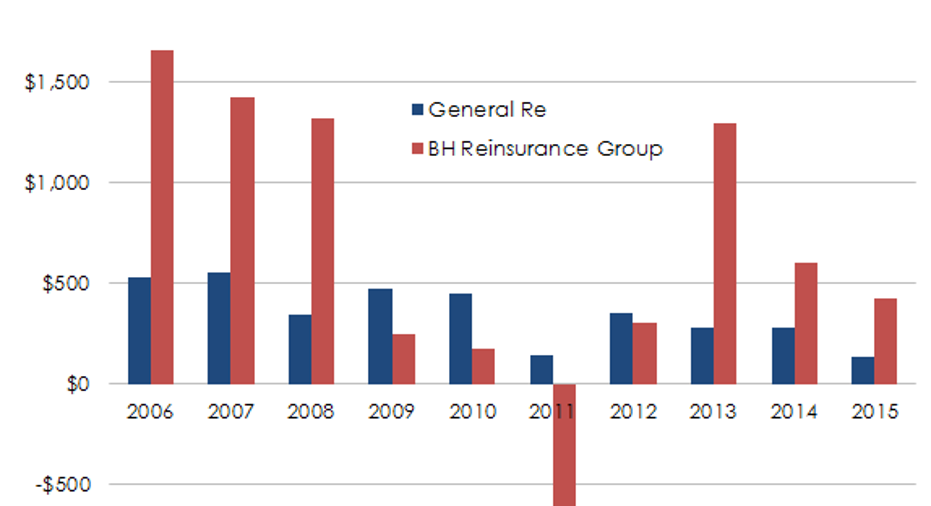

Reinsurance is a major contributor to Berkshire. In the past 10 years, General Re and BH Reinsurance have generated nearly $10.3 billion in pre-tax underwriting profits. The duo are the main drivers of Berkshire's insurance float, which generated $47.5 billion in pre-tax investment profits in the same 10-year period.

It wouldn't be the first time that Buffett has stepped off the gas pedal when the risk-reward turned unfavorable. Over a period spanning two decades, he watched as National Indemnity, another insurer Berkshire owns, shrank written premium volume 85%, while refusing to fire a single worker. Buffett views it as an important part of building a profitable culture -- he wants his insurers to do nothing when pricing is unfavorable.

Luckily, there are other fertile grounds to put cash to work. Buffett noted in his annual letter to shareholders that Berkshire's companies invested $16 billion in property, plant, and equipment in 2015, much of it in the company's energy units and its railroad, Burlington Northern Sante Fe.

Though regulated utilities aren't particularly profitable -- at least not by Berkshire's standards -- lower capital requirements for its shrinking insurance units somewhat validates the importance of having a go-to sponge for capital in the energy industry.

The article Berkshire Hathaway's Big Profit Center Prepares for Shrinkage originally appeared on Fool.com.

Jordan Wathen has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Berkshire Hathaway. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.