Why Kinder Morgan Serves As a Warning to Dividend Investors

Source: Kinder Morgan.

Dividend growth investing has been shown to be the best long-term strategy to grow wealth over time. However, thanks to the worst oil crash in over 50 years, many energy dividend stocks have ended up doing very poorly.

KMI Total Return Price data by YCharts

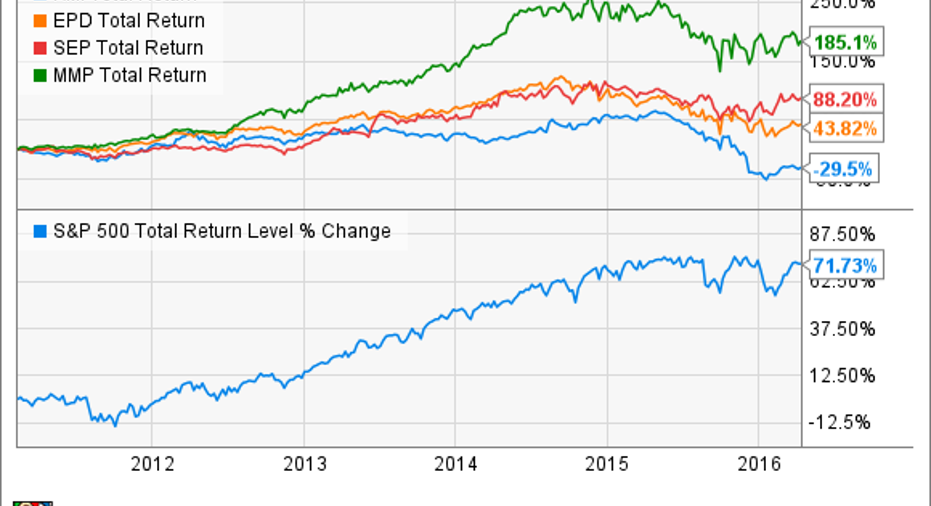

Kinder Morgan has not only underperformed the overall market over the past five years,but even when dividend reinvestment is factored in (total returns) it's actually lost investors money.Yet competitors such as Enterprise Products Partners , Spectra Energy Partners , and Magellan Midstream Partners have done much better.

The reason forKinder's poorperformance over the past half-decadecan teach investorsa vital lesson neededto avoid a similar fate. More importantly, it illustrates why Enterprise, Spectra, and Magellan will probably continue to be superior dividend growth investments over the coming years.

What went wrong at Kinder MorganThere's nothing inherently wrong with Kinder Morgan's assets. In fact,they generated $4.7 billion in distributable cash flow in 2015 andare expectedto generate $4.9 billion of DCF this year.

Kinder's problem was management's focus on excessive dividend growthat the expense of retaining enough cash flow to decrease reliance on external capital markets for growth.

While this worked fine when oil prices were high for years, as crude crashed and Wall Street abandoned all things oil- and gas-related, Kinder's share price plunged. This situation made equity capital increasingly expensive and raised capital costs high enough to make an increasing share of Kinder's expansion backlog less lucrative.

Until the end of 2015, Kinder was able to continue borrowing debt cheaply, but eventually its balance sheet became so overleveraged that rating agencies threatened to cut its rating to "junk." Doing so would've made future borrowing and refinancing costsfor $43.2 billion in debt skyrocket.

Kinder was then forced to finally do what Enterprise, Spectra, and Magellan had been doing all along; become more conservative with its approach to debt, and rely more on itsinternally generated cash flow to fund growth. For investors this meant a brutal 80% dividend cut, which the market had been anticipating for months and caused the share price to collapse.

The most important lesson dividend investors need to learn

| Company/MLP | Yield | 2015 Distribution CoverageRatio(Excluding Asset Sales) | Long-TermProjected Annual Payout Growth Rate |

|---|---|---|---|

| Kinder Morgan | 11.4% | 1.11 | NA |

| Enterprise Products Partners | 6.6% | 1.3 | 5.2% in 2016 |

| Spectra Energy Partners | 5.4% | 1.2 | 7.3% CAGR through 2018 |

| Magellan Midstream Partners | 4.8% | 1.2 | 10% in 2016 "at least" 8% in 2017 |

Sources: 10-Ks, Yahoo! Finance, management guidance, Fastgraphs.

For a little comparison here, this table shows Kinder's yield and 2015 coverage ratio had it maintained its dividend.

Kinder's maximum $0.51-per-share quarterly dividend was simply not sustainable, given the low coverage and lack of ongoing access to sufficiently cheap capital markets.Had management chosen to maintain this payout in 2016, even this year's projected 4.3% increase in cash flow would have resulted in a DCR of 1.08and probably a credit downgrade that could have permanently hurt future dividend growth.

While management made the right choice in terms of maximizing long-term investor value, Enterprise Products Partners', Spectra Energy Partners', and Magellan Midstream Partners' already were maintaining higher coverage ratios that allowed them to generate excess cash flow. This situation is expected to still allow payout growth even as oil prices remain at multi-year lows.

It was also a result of their more conservative managements, which, understanding the inherent cycle nature of energy prices, wisely chose to focus on two other vitally important metrics over the yearsthat make up the cornerstone of long-term distribution sustainability.

Strong balance sheet and project profitability

| Company/MLP | Debt/EBITDA (Leverage Ratio) | Weighted Average Cost of Capital (WACC) | Return on Invested Capital (ROIC) |

|---|---|---|---|

| Kinder Morgan | 5.6 | 3.03% | 1.87% |

| Enterprise Products Partners | 4.5 | 6.87% | 8.52% |

| Spectra Energy Partners | 3.6 | 5.85% | 7.36% |

| Magellan Midstream Partners | 2.9 | 7.12% | 18.64% |

Sources: Morningstar, GuruFocus.

Kinder Morgan's years of reliance onexternal capital not only resulted in a highly leveraged balance sheet that was the primary reason for the dividend cut, but it also hurt the company's long-term ability to grow shareholder value.

That's because it reduced the company's return on invested capital below its cost of capital, meaning that while new projects coming online will increase cash flow, they might not generate capital long term.

In an industry that's continually raising outside capital, it can be hard to know whether a company or MLPis really growing profitably or just using new capital to grow cash flows at any price.

That's why net ROIC is one metric you should keep a close eye on.Understand that netROIC isn't a perfect metric forjudging profitability because itrelies partly onshare volatility, which doesn't directly affect thereturns onprojects. In addition net income doesn'tshow an asset's cash flow generating potential, which is something investors should care about since it's what funds the quarterly payouts. However,as a rule of thumb it's a good way to ensure that management's using investor money wisely.

Bottom lineYield and dividend growth are often the first two things income investors focus on. Yetpayout sustainability is the most important factor.That's the reason all dividend investors need topay attentionto the three pillars of long-term dividend sustainability: coverage ratio, a strong balance sheet, and returns on capital in excess of its cost of capital.

While Kinder Morgan is likely toeventually recover, Enterprise Products Partners, Spectra Energy Partners, and Magellan Midstream Partnerscontinue offeringinvestors superior payout sustainability profiles, which should result in better long-term total returns.

The article Why Kinder Morgan Serves As a Warning to Dividend Investors originally appeared on Fool.com.

Adam Galas has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Kinder Morgan. The Motley Fool has the following options: short June 2016 $12 puts on Kinder Morgan. The Motley Fool recommends Enterprise Products Partners and Magellan Midstream Partners. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.