Shining a Light on SolarCity's Complex Fourth Quarter

Note: This article originally appeared in Motley Fool Rule Breakers on Feb.12, 2016. For a free trial to join Rule Breakers, click here.

Solar power system providerSolarCity looked a little less bright after reporting fourth-quarter results. The company's stock price fell as much as 30% in the trading session directly following their earnings release.

SolarCity installed a record 272 MW of new capacity, up 54% over last year. Regardless, this still fell short of guidance -- which was for 280 to 300 MW. CEO Lyndon Rive blamed the shortfall on delays of a few larger commercial projects, and on the company's recent decision to cease operations in the state of Nevada. He also guided for only 180 MW of new capacity additions for the coming first quarter.

The miss on the quarterly installs and the weak guidance appear to be the drivers behind Wednesday's exaggerated sell-off. But there's a bit more to the picture than just coming up short on guidance -- including a change in the company's strategy, and a shifting capital structure.

Let's look at each of those in greater detail, and dig into what they mean for investors.

An evolving strategyAs Imentioned last quarter, SolarCity's business strategy is in flux.

For most of the past decade, the company has focused primarily on the residential market, vertically integrating its operations, distribution, and sales force -- and leapfrogging smaller competitors in the highly fragmented market. Residential installations in the fourth quarter were up 49% over the same period last year, and SolarCity accounted for 35% of total U.S. residential solar installations during the full year of 2015. It is, by far, the largest player in the residential market.

But with uncertainty about whether the 30% federal investment tax credit for solar systems would be extended, SolarCity decided last quarter to leverage its warehouses and distribution to go after more-profitable commercial installations. These projects attract more competition, but are also larger jobs, with more attractive economics. As long as SolarCity can succeed in winning new bids, this strategy should have a positive effect on overall profitability.

We're certainly seeing the early signs of this paying off. Commercial installations increased 82% year over year, to 51 MW, in the fourth quarter. And because the projects are larger, the fixed costs are more widelyspread out. On a per-watt basis, sales expenses fell to $0.56 -- down 13% from just last quarter.

The company continues to relentlessly take costs out of its operations, driving "all-in" costs down to $2.71 per watt deployed. President Tanguy Serra thinks the company can get costs down to $2.25/W by 2017, which would be an additional 20% improvement by the end of next year.

Image source: SolarCity investor presentation.

However, the new focus on commercial isn't all sunshine. Commercial jobs are complex, and require more permitting and paperwork (which can sometimes take months to complete).

Forecasting and allocating working capital and manpower to this market can be tricky, and projects often get delayed. Three larger projects in the Northeast with 15 MW of combined capacity fell behind schedule in December. Had SolarCity finished just those three on time, it wouldn't have missed fourth-quarter guidance.

Overall, we think SolarCity's increasing attention to the commercial market will reward shareholders in the form of more-profitable installations. But there are still a few wrinkles the company needs to iron out as it learns how to serve its new customers most efficiently.

Capital structureIt costs SolarCity $2.71 per watt for each new panel it deploys. Let's shine some light on how the bill for that actually gets paid.

Traditionally, the company has issued long-term debt and equity to fund most of its expansion plans while mixing in a few other clever financing strategiesto cover the rest. A few of those strategies include using the solar panels themselves to generate cash up front -- such as aggregating their tax benefits (tax equity), or using them as collateral to issue asset-backed securities (securitizations). For each of these forms of asset financing, SolarCity recognizes an immediate benefit, which it can effectively use to cover the cost of its newly deployed panels.

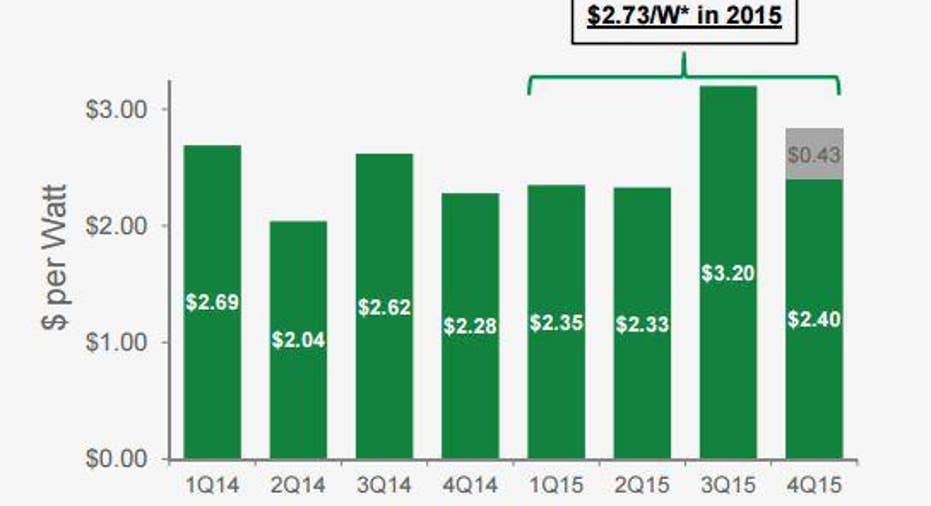

Now that SolarCity is getting bigger, it's becoming very efficient at monetizing those up-front benefits. It deployed 253 MW of new capacity in the fourth quarter, which included 218 MW of operating leases, 26 MW of MyPower loans, and 9 MW of straight-up system sales (note that MW deployed only counts projects that are up and running and are generating power, which is why it is less than the capacity of MW installed). From those deployments,tax-equity financing contributed an equivalent of $1.38 per watt deployed of the blended total, securitizations contributed $0.95/W, andstate rebates and prepayments brought in $0.07/W.

Altogether, SolarCity's average asset financing totaled $2.40/W for the quarter and $2.73/W for 2015.

Image source: SolarCity investor presentation.

Compare SolarCity's $2.73/W of full-year asset financing to its $2.71 of all-in costs, and you see that the company is reaching the point at which it can effectively fund the up-front costs of deploying new panels with the panels themselves. There's less of a need to take on the burden of higher-interest rate debt, or to dilute shareholders to fund expansion.

Here's a quote from Rive during the conference call (emphasis mine):

Of course, not everything is immediately monetized upfront. The solar systems also churn out electricity that generates monthly cash flows for 20-plus years. Each new watt deployed is estimated to generate $3.64 of gross value (calculated by discounting the unlevered cash flows of the projects to the present). That means SolarCity is monetizing and capturing roughly two-thirds of its new projects' value up front; the other third is held on to during the remainder of its lifespan.

Image source: SolarCity Investor Presentation.

Um, what did he just say?All right, Simon, enough with the financial mumbo-jumbo. What does all of this mean for me as an investor?

The bottom line is that SolarCity needs to borrow a lot of money to fund its expansion, so financing costs matter. Just as a bank relentlessly tracks the net interest margin between its deposits and loans, SolarCity keeps close tabs on how it's raising money, the value it's creating from the end markets it's selling to, and the profitability spread between the two of those.

The markets for tax equity and solar securitizations are maturing, giving SolarCity additional options to monetize more longer-term financing up front. The company is increasingly tapping these markets to use asset-based securities and aggregation facilities to borrow at more attractive rates. Of course, we also recognizethat if the credit markets were to dry up, SolarCity's access to financing could also fall -- which could significantly slow expansion plans.

We've seen financing play an increasing role in SolarCity's strategy. Rather than reporting the total number of customers, total number of contracts, and net retained value, the company is focusing today on value per MW deployed, and the effect to the bottom line that each new project pulls in. For shareholders -- who have a claim to that profit stream that the business generates -- this is a move that will be bumpy in the short term, but is worth it in the long run.

Policy and expansionI recently chatted on a Rule Breakers podcast about the effect that political headlines have had on SolarCity's stock price. Here are a few of the volatility-inducing things that have taken place in the political arena:

- The solar investment tax credit wasextended for five more years.

- California approved a new net metering policy, which includes time-of-use rates.

- Nevada is preliminarily (but also retroactively) raising the monthly fees, and lowering net metering rates for solar customers. This action has caused SolarCity to cease operations in the state, and relocate its employees.

Energy policy decisions are largely made state by state -- though they can have a measurable effect on SolarCity's business -- and it's very difficult to predict which way the votes will go. We do believe SolarCity's policy team is making progress on shaping future policy. But this is, and will always be, a risk of investing in companies that operate in political industries such as energy.

The company also updated investors that international operations are ramping up. Thanks to the company's recent acquisition of Mexican solar developer ILIOSS, SolarCity is planning to launch a product in Mexico within two quarters. Rive also briefly mentioned that other international opportunities are on the table, and that SolarCity is considering entering a third country by year-end. We'll stay tuned.

TheFoolish bottom lineThis past year was a wild one for SolarCity shareholders, with the stock popping or dropping 30% or more on multiple occasions. From our Foolish perspective, the monthly fluctuations are less important than the company's shift in business strategy and its focus on profitability.

I'll wrap this up with an excerpt from the final section of Rive's letter to shareholders:

We love that SolarCity is strategically thinking in the longer term, and tactically building a battle plan for the short term on how to get there. The energy industry is huge and full of challenges, but we like the steps SolarCity is taking to retain its top-dog position in solar.

The article Shining a Light on SolarCity's Complex Fourth Quarter originally appeared on Fool.com.

Simon Erickson owns shares of SolarCity andhas the following options: long January 2017 $50 calls on SolarCity, short January 2017 $50 puts on SolarCity, and short January 2017 $40 puts on SolarCity. The Motley Fool owns shares of and recommends SolarCity. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.